You might also like

- AC201 Notes PART 1Document25 pagesAC201 Notes PART 1mollymgonigle1No ratings yet

- Summary Notes - Conceptual Framework - Objective of Financial ReportingDocument5 pagesSummary Notes - Conceptual Framework - Objective of Financial ReportingEDMARK LUSPENo ratings yet

- FA1-01 - Accounting Framework - 2013 Edition - PortraitDocument5 pagesFA1-01 - Accounting Framework - 2013 Edition - PortraitFloyd Alexis RafananNo ratings yet

- Chapter 3 SummaryDocument3 pagesChapter 3 SummaryXiaoyu KensameNo ratings yet

- Module 2 Conceptual Framework For Financial ReportingDocument9 pagesModule 2 Conceptual Framework For Financial ReportingVivo V27No ratings yet

- Who Are The Users of Accounting Information and How Do They Benefit From This Information?Document4 pagesWho Are The Users of Accounting Information and How Do They Benefit From This Information?Marco PaulNo ratings yet

- Conceptual Framework Underlying Financial Reporting: Thursday, January 9, 2020 9:45 PMDocument10 pagesConceptual Framework Underlying Financial Reporting: Thursday, January 9, 2020 9:45 PMClyde Ian Brett PeñaNo ratings yet

- Rev. CH2Document3 pagesRev. CH2Mark RanekNo ratings yet

- Lecture 1 NoteDocument5 pagesLecture 1 NoteKanokporn TangthamvanichNo ratings yet

- 11Document27 pages11James Gliponio CamanteNo ratings yet

- Framework For The Preparation and Presentation of The Financial StatementsDocument28 pagesFramework For The Preparation and Presentation of The Financial StatementsTin ManaogNo ratings yet

- Why Are Financial Statements Important?Document23 pagesWhy Are Financial Statements Important?Dylan AdrianNo ratings yet

- Chapter 01: Conceptual FrameworkDocument14 pagesChapter 01: Conceptual FrameworkCorin Ahmed CorinNo ratings yet

- Conceptual Framework and Financial Statements SummaryDocument5 pagesConceptual Framework and Financial Statements SummaryAndrea Mae ManuelNo ratings yet

- Ch1-Fundamental of Financial AccountingDocument40 pagesCh1-Fundamental of Financial AccountingEYENNo ratings yet

- Fundamentals of Financial AccountingDocument40 pagesFundamentals of Financial AccountingEYENNo ratings yet

- Financial StatementsDocument68 pagesFinancial StatementsEdmon Lopez100% (1)

- Conceptual Framework: Far 3 Esrl & JPRFDocument11 pagesConceptual Framework: Far 3 Esrl & JPRFAnne NavarroNo ratings yet

- Conceptual FrameworkDocument45 pagesConceptual FrameworkKendall JennerNo ratings yet

- CFAS Summarized NotesDocument6 pagesCFAS Summarized Noteslyleisaac.illaga.23No ratings yet

- Financial ReportingDocument133 pagesFinancial ReportingJOHN KAMANDANo ratings yet

- Conceptual FrameworkDocument8 pagesConceptual FrameworkHashi OrloNo ratings yet

- Reviewer Acca 102Document12 pagesReviewer Acca 102Nicole FidelsonNo ratings yet

- Financial ReportingDocument133 pagesFinancial ReportingClerry SamuelNo ratings yet

- Conceptual FrameworkDocument57 pagesConceptual FrameworkmolemothekaNo ratings yet

- Status and Purpose and Status of The FrameworkDocument7 pagesStatus and Purpose and Status of The FrameworkMercado GlendaNo ratings yet

- Basic Financial Statements: Conceptual FrameworkDocument11 pagesBasic Financial Statements: Conceptual FrameworkNhel AlvaroNo ratings yet

- CFAS Chap2-7Document40 pagesCFAS Chap2-7Patrick Jayson VillademosaNo ratings yet

- CFM02 FAR2 2018 Conceptual FrameworkDocument7 pagesCFM02 FAR2 2018 Conceptual FrameworkAnime LoverNo ratings yet

- Summary of Accounting Standards From Cfas Book CompressDocument34 pagesSummary of Accounting Standards From Cfas Book Compressofficial.kwentoniagimatNo ratings yet

- Financial Reporting PDFDocument67 pagesFinancial Reporting PDFlukamasia93% (15)

- Chapter 4 Accounting Concepts and PrinciplesDocument14 pagesChapter 4 Accounting Concepts and PrinciplesAngellouiza MatampacNo ratings yet

- Cfas and Pas 1 AnswersDocument10 pagesCfas and Pas 1 AnswersFrancene Shalanda SapilanNo ratings yet

- Notes CfasDocument7 pagesNotes CfasCorin Ahmed CorinNo ratings yet

- Intermediate Accounting 3 The Conceptual Framework For Financial Reporting Purpose and Status of The FrameworkDocument5 pagesIntermediate Accounting 3 The Conceptual Framework For Financial Reporting Purpose and Status of The FrameworkFe VhieNo ratings yet

- Conceptual FrameworkDocument5 pagesConceptual Frameworkchaleen23No ratings yet

- Handout 2 Concepts and Principles of AccountingDocument5 pagesHandout 2 Concepts and Principles of AccountingRyzha JoyNo ratings yet

- #02 Conceptual FrameworkDocument5 pages#02 Conceptual FrameworkZaaavnn VannnnnNo ratings yet

- CHAPTER 2-Accounting Framework RevisedDocument7 pagesCHAPTER 2-Accounting Framework RevisedMuchakunda GooraNo ratings yet

- Chap 2 NotesDocument3 pagesChap 2 Notes乙คckคrψ YTNo ratings yet

- Fa (Mubs) Mba 2018-19Document185 pagesFa (Mubs) Mba 2018-19henrywasulaNo ratings yet

- B291 TheoryDocument9 pagesB291 TheoryNajwa Al-khateebNo ratings yet

- Conceptual Framework (Part 1)Document3 pagesConceptual Framework (Part 1)Eui KimNo ratings yet

- Conceptual FrameworkDocument5 pagesConceptual FrameworkSherlyn AnacionNo ratings yet

- Basic Accounting ConceptsDocument3 pagesBasic Accounting ConceptsVanSendrel Parate100% (1)

- AFM 291 Chapter 2 NotesDocument6 pagesAFM 291 Chapter 2 NoteszoeyNo ratings yet

- SBR Pocket NotesDocument32 pagesSBR Pocket Notesfab home100% (1)

- Conceptual Framework - Chapter 1Document2 pagesConceptual Framework - Chapter 1Miko Louis ManligoyNo ratings yet

- M1 Handout 4 Conceptual Framework of AccountingDocument9 pagesM1 Handout 4 Conceptual Framework of AccountingAmelia TaylorNo ratings yet

- AUDITINGDocument13 pagesAUDITINGGrace AlolorNo ratings yet

- L3Document4 pagesL3Emilrose SadiasaNo ratings yet

- Financial Accounting and Reporting 2 Accounting 007: Mr. Dennis V. Dupitas, CPADocument11 pagesFinancial Accounting and Reporting 2 Accounting 007: Mr. Dennis V. Dupitas, CPAShaira Mangon RamirezNo ratings yet

- Toa Iasb Conceptual FrameworkDocument11 pagesToa Iasb Conceptual FrameworkreinaNo ratings yet

- Lesson 2 - Accounting Concepts and PrinciplesDocument5 pagesLesson 2 - Accounting Concepts and PrinciplesJeyem AscueNo ratings yet

- Intermediate Accounting: Eleventh Canadian EditionDocument41 pagesIntermediate Accounting: Eleventh Canadian EditionthisisfakedNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Table of Specifications: University of Santo TomasDocument3 pagesTable of Specifications: University of Santo TomasAINAH SALEHA MIMBALAWAGNo ratings yet

- CFAS Part 5Document10 pagesCFAS Part 5AINAH SALEHA MIMBALAWAGNo ratings yet

- CFAS Part 4Document11 pagesCFAS Part 4AINAH SALEHA MIMBALAWAGNo ratings yet

- CFAS Part 1Document3 pagesCFAS Part 1AINAH SALEHA MIMBALAWAGNo ratings yet

- CFAS Part 2Document5 pagesCFAS Part 2AINAH SALEHA MIMBALAWAGNo ratings yet

- Financial Reporting Mcom 3 Semester: AssetsDocument2 pagesFinancial Reporting Mcom 3 Semester: AssetsYasir AminNo ratings yet

- Departmental Accounts PDFDocument41 pagesDepartmental Accounts PDFAryan ChoudharyNo ratings yet

- Banking On The Belt and Road Insights From A New Global Dataset of 13427 Chinese Development ProjectsDocument166 pagesBanking On The Belt and Road Insights From A New Global Dataset of 13427 Chinese Development ProjectsJose Luis PerelloNo ratings yet

- Satyam ScientificDocument1 pageSatyam ScientificHussain ShaikhNo ratings yet

- DGFT FAQs - Status Holder Certificate v1.0Document6 pagesDGFT FAQs - Status Holder Certificate v1.0pratyush1200No ratings yet

- Snapshot Q1 2023Document3 pagesSnapshot Q1 2023JIA WEI SIEWNo ratings yet

- Manias, Panics, and Crashes: A History of Financial Crises: Book SummaryDocument3 pagesManias, Panics, and Crashes: A History of Financial Crises: Book Summarydabster7000No ratings yet

- Business Partner C1 WorkbookDocument51 pagesBusiness Partner C1 WorkbookVeronika Chekan86% (7)

- Is The World Witnessing Reverse GlobalizationDocument7 pagesIs The World Witnessing Reverse GlobalizationDinesh VelliangiriNo ratings yet

- GRS Scope Certificate 2022 CG700072Document5 pagesGRS Scope Certificate 2022 CG700072Asa RudiNo ratings yet

- Basics of Stock Market Trading GuideDocument10 pagesBasics of Stock Market Trading Guidegokul kNo ratings yet

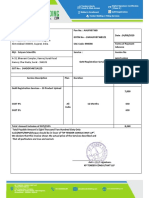

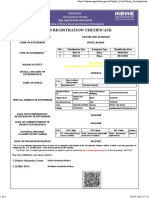

- Raju N Print Udyam Registration CertificateDocument3 pagesRaju N Print Udyam Registration CertificateOmkar kaleNo ratings yet

- A Owns Majority of The Outstanding Ordinary SharesDocument2 pagesA Owns Majority of The Outstanding Ordinary Sharesasdfghjkl zxcvbnmNo ratings yet

- IFRS 15 SolutionsDocument12 pagesIFRS 15 SolutionsshakilNo ratings yet

- Husky Brochure EnglishDocument26 pagesHusky Brochure EnglishPandega DewantoNo ratings yet

- SUMMER INTERNSHIP PROJECT REPORT KavyaDocument76 pagesSUMMER INTERNSHIP PROJECT REPORT Kavyakavya srivastavaNo ratings yet

- International Economics: The Standard Theory of International TradeDocument35 pagesInternational Economics: The Standard Theory of International TradeZ pristinNo ratings yet

- VJQ.23 04496 2Document3 pagesVJQ.23 04496 2tdm_101No ratings yet

- Summary Acctg 320Document3 pagesSummary Acctg 320Cj ReyesNo ratings yet

- Gpbs 2024 BrochureDocument8 pagesGpbs 2024 BrochurejayeshmananiNo ratings yet

- Activity Based CostingDocument52 pagesActivity Based CostingAfrina AfsarNo ratings yet

- Brand PerceptionDocument1 pageBrand PerceptionsantoshkumarvarmaNo ratings yet

- Final ECO2Document84 pagesFinal ECO2Phan Ngọc Như BìnhNo ratings yet

- Mahesh MumbaiDocument3 pagesMahesh MumbaiANISH SHAIKHNo ratings yet

- Financial Management 1 CatDocument9 pagesFinancial Management 1 CatcyrusNo ratings yet

- Aon - 2021 Global Risk Management Survey FindingsDocument142 pagesAon - 2021 Global Risk Management Survey FindingsIgnacio Alfredo A.F.No ratings yet

- "Navodaya Vidyalaya Samiti" PRE-BOARD Exam 2020-21 Class: Xii Subject: Accountancy (055) TIME: 3 Hours Max Marks: 80Document12 pages"Navodaya Vidyalaya Samiti" PRE-BOARD Exam 2020-21 Class: Xii Subject: Accountancy (055) TIME: 3 Hours Max Marks: 80hardikNo ratings yet

- Ms09 Standard Costing Variance AnalysisDocument7 pagesMs09 Standard Costing Variance AnalysisAshley BrevaNo ratings yet

- Sartorius Stedim India: Bioprocess Solutions 5S JourneyDocument53 pagesSartorius Stedim India: Bioprocess Solutions 5S JourneyChethan Nagaraju KumbarNo ratings yet

- Undergraduate Internship Report: AcknowledgementsDocument62 pagesUndergraduate Internship Report: AcknowledgementsDawit WorkuNo ratings yet