You might also like

- Economics and Other Related LawsDocument29 pagesEconomics and Other Related LawsMhary Antonette OrdinNo ratings yet

- Economic DevelopmentDocument17 pagesEconomic DevelopmentVher Christopher Ducay100% (1)

- TCW Economics Intro ExpandedDocument27 pagesTCW Economics Intro ExpandedMarck Niño Abe CoronelNo ratings yet

- Chapter 1 ECONDocument9 pagesChapter 1 ECONMelody ViernesNo ratings yet

- EconomicsDocument5 pagesEconomicsFarah FatimaNo ratings yet

- Political Economy Framework of The PhilippinesDocument7 pagesPolitical Economy Framework of The PhilippinesAyza Unay MontejosNo ratings yet

- IB ECON Chapter 1 Notes (Basics of Econ)Document6 pagesIB ECON Chapter 1 Notes (Basics of Econ)H15T0RYK1NGNo ratings yet

- Economics AssignmentDocument6 pagesEconomics Assignmentsolo_sudhanNo ratings yet

- Lecture Key Int EconomyDocument26 pagesLecture Key Int Economyf nNo ratings yet

- What Is Economics.s02Document75 pagesWhat Is Economics.s02GenNo ratings yet

- Eco - NotesDocument4 pagesEco - NotesMukunth KLNo ratings yet

- Economic Challenges Facing Contemporary BusinessDocument24 pagesEconomic Challenges Facing Contemporary Businessmonel_24671No ratings yet

- Handout Applied EconDocument6 pagesHandout Applied EconShaina MancolNo ratings yet

- Econ Note For A LevelDocument43 pagesEcon Note For A LevelteeheeteeheehahahaNo ratings yet

- Int'l Trade 4Document2 pagesInt'l Trade 4Zarina ChanNo ratings yet

- Economics Notes HYDocument21 pagesEconomics Notes HYilu_3No ratings yet

- Summary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESFrom EverandSummary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESNo ratings yet

- Introduction To EconomicsDocument23 pagesIntroduction To EconomicsSampath HewageNo ratings yet

- (Chapter 2) Understanding Economics and How It Affects BusinessDocument6 pages(Chapter 2) Understanding Economics and How It Affects BusinessTommyArnzenNo ratings yet

- (Half-Yearly) Introduction To EconomicsDocument8 pages(Half-Yearly) Introduction To EconomicsEllia ChenNo ratings yet

- Applied Economics (Prelims)Document12 pagesApplied Economics (Prelims)Amor A. Fuentecilla Jr.No ratings yet

- Health Economics PrelimDocument15 pagesHealth Economics PrelimMelchor Felipe SalvosaNo ratings yet

- Economics Notes - Introduction To EconomicsDocument16 pagesEconomics Notes - Introduction To Economicskkesarwani727No ratings yet

- Econ 1-Lesson 1 ModuleDocument9 pagesEcon 1-Lesson 1 ModuleArnie Jovinille Sablay RemullaNo ratings yet

- Economic ThinkingDocument3 pagesEconomic ThinkingTrixia Dela CruzNo ratings yet

- Economics Cheat SheetDocument3 pagesEconomics Cheat SheetMushfiq Jahan KhanNo ratings yet

- Economic Planning and StrategyDocument6 pagesEconomic Planning and Strategyolivasjonas6No ratings yet

- Introduction To EconomicsDocument12 pagesIntroduction To EconomicsBaro LeeNo ratings yet

- McGraw Business Summary Unit1Document6 pagesMcGraw Business Summary Unit1Jimmy gogoNo ratings yet

- Chapter-1: EconomisDocument7 pagesChapter-1: EconomisAsya YıldırımNo ratings yet

- Summary Of "The Economic System" By Armando Fastman: UNIVERSITY SUMMARIESFrom EverandSummary Of "The Economic System" By Armando Fastman: UNIVERSITY SUMMARIESNo ratings yet

- Nat Review PPT Session1Document54 pagesNat Review PPT Session1Dorie MinaNo ratings yet

- Eco NotesDocument10 pagesEco NotesNicoleUmaliNo ratings yet

- 'A State of Complete Physical, Mental and Social Well-Being And. Not MerelyDocument7 pages'A State of Complete Physical, Mental and Social Well-Being And. Not MerelyAdam JerusalemNo ratings yet

- Classification of The Economies, Demand, Demand CurveDocument45 pagesClassification of The Economies, Demand, Demand CurvesambaNo ratings yet

- Macroeconomics Definitions ReviewerDocument6 pagesMacroeconomics Definitions ReviewerArizza NocumNo ratings yet

- Principles of EconomicsDocument27 pagesPrinciples of EconomicsChristopher Villegas33% (3)

- Mod 1 MicroecoDocument23 pagesMod 1 MicroecoHeina LyllanNo ratings yet

- What Is Economics About: Relative ScarcityDocument28 pagesWhat Is Economics About: Relative Scarcitykevin9797No ratings yet

- IntrotoBusiness 02 EconEnvironmentDocument22 pagesIntrotoBusiness 02 EconEnvironmentchaudhary samavaNo ratings yet

- Entrepreneurs in A Market EconomyDocument46 pagesEntrepreneurs in A Market EconomyRahul KumarNo ratings yet

- At The End of This Chapter/module, You Will Be Able ToDocument8 pagesAt The End of This Chapter/module, You Will Be Able ToSamantha LeexyNo ratings yet

- Economics and ScarcityDocument23 pagesEconomics and ScarcityMarsha Benito AmorinNo ratings yet

- MacroeconomicsDocument9 pagesMacroeconomicsWynnie Pouh100% (1)

- Principles of Economics and Bangladesh EconomyDocument6 pagesPrinciples of Economics and Bangladesh EconomyZonal office ChapainawbagnajNo ratings yet

- Applied Economics. ReviewerDocument9 pagesApplied Economics. ReviewerKISS VALERY CAMACHONo ratings yet

- Toaz - Info CXC Economics Study Guide PRDocument31 pagesToaz - Info CXC Economics Study Guide PRRickoy Playz100% (1)

- Chapter 2-2Document25 pagesChapter 2-2Tanner MelleNo ratings yet

- 1 Introduction To EconomicsDocument24 pages1 Introduction To Economicsrommel legaspiNo ratings yet

- FOGEDocument8 pagesFOGEssssaaatraNo ratings yet

- Economic Challenges Facing Contemoprary BusinessesDocument24 pagesEconomic Challenges Facing Contemoprary BusinessesMHPNo ratings yet

- The Economic Problem: Industrial RevolutionDocument16 pagesThe Economic Problem: Industrial RevolutionhenniekNo ratings yet

- Economics As A Social Science and Applied Science in Terms of Nature and ScopeDocument45 pagesEconomics As A Social Science and Applied Science in Terms of Nature and ScopeRenz Errol SaavedraNo ratings yet

- Ec1 SystemsDocument27 pagesEc1 Systemsapi-251258644No ratings yet

- Macro Economics Cycle Contribute To The Growth BetweenDocument5 pagesMacro Economics Cycle Contribute To The Growth BetweenQNo ratings yet

- Midterm LecDocument5 pagesMidterm Lecmary joyNo ratings yet

- Econ NoteDocument9 pagesEcon NoteKigari AtasaNo ratings yet

- Definition of EconomicsDocument14 pagesDefinition of EconomicsChristian Jack CordovaNo ratings yet

- Chap 3Document26 pagesChap 3Jawad ArkoNo ratings yet

- Applied Econ. Lesson 1Document21 pagesApplied Econ. Lesson 1Shiela Jean H. RescoNo ratings yet

- Finals MarketingDocument7 pagesFinals MarketingDanica DimaculanganNo ratings yet

- Geological Processes On Earth's SurfaceDocument34 pagesGeological Processes On Earth's Surfacedanica dimaculanganNo ratings yet

- ENTREPRENEURSHIPDocument8 pagesENTREPRENEURSHIPDanica DimaculanganNo ratings yet

- Business EthicsDocument14 pagesBusiness EthicsDanica DimaculanganNo ratings yet

- Business EnterpriseDocument15 pagesBusiness EnterpriseDanica DimaculanganNo ratings yet

- Business Finance: Weeks 3-4Document25 pagesBusiness Finance: Weeks 3-4Danica DimaculanganNo ratings yet

- Working Capital Management: Week 6Document45 pagesWorking Capital Management: Week 6Danica DimaculanganNo ratings yet

- Business Finance: Continuation W1Document19 pagesBusiness Finance: Continuation W1Danica DimaculanganNo ratings yet

- Business Finance W1Document17 pagesBusiness Finance W1Danica DimaculanganNo ratings yet

- The Catholic MassDocument24 pagesThe Catholic MassDanica DimaculanganNo ratings yet

- Affiliated To University of Mumbai Program: COMMERCE Program Code: RJCUCOM (CBCS 2018-19)Document20 pagesAffiliated To University of Mumbai Program: COMMERCE Program Code: RJCUCOM (CBCS 2018-19)Endubai SuryawanshiNo ratings yet

- Customer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedDocument25 pagesCustomer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedOmor FarukNo ratings yet

- Model LLP AgreementDocument20 pagesModel LLP AgreementSoumitra Chawathe71% (21)

- TATA 1MG Healthcare Solutions Private Limited: Wadi On Jalamb Road Khamgaon,, Buldhana, 444303, IndiaDocument1 pageTATA 1MG Healthcare Solutions Private Limited: Wadi On Jalamb Road Khamgaon,, Buldhana, 444303, IndiaTejas Talole0% (1)

- Faktor Resiko TBDocument15 pagesFaktor Resiko TBdrnurmayasarisihombingNo ratings yet

- MQ1 1Document1 pageMQ1 1shaira alliah de castroNo ratings yet

- Agricultural InsuranceDocument21 pagesAgricultural InsuranceSamer SahuNo ratings yet

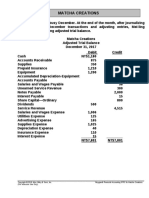

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Other SourceDocument43 pagesOther SourceJai RajNo ratings yet

- Assignment of Contract (Correct Version)Document2 pagesAssignment of Contract (Correct Version)Heru Atiba El - BeyNo ratings yet

- Tribune 17th June 2023Document30 pagesTribune 17th June 2023adam shingeNo ratings yet

- State of Afghan Cities 2015 Volume - 1Document156 pagesState of Afghan Cities 2015 Volume - 1United Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- Working Capital Management (Bhavani)Document86 pagesWorking Capital Management (Bhavani)gangatulasiNo ratings yet

- RTI ManualDocument79 pagesRTI Manualtnpsc2busarNo ratings yet

- Research Methods For Architecture Ebook - Lucas, Ray - Kindle StoreDocument1 pageResearch Methods For Architecture Ebook - Lucas, Ray - Kindle StoreMohammed ShriamNo ratings yet

- ECO Ebook by CA Mayank KothariDocument404 pagesECO Ebook by CA Mayank KothariHemanthNo ratings yet

- Project Cycle Management Report (AEPAM Pub.288)Document64 pagesProject Cycle Management Report (AEPAM Pub.288)Waqar AhmadNo ratings yet

- Labor Costs in Manufacturing IndustriesDocument18 pagesLabor Costs in Manufacturing Industriesminhduc2010No ratings yet

- GX Cloud Banking 2030 FsiDocument12 pagesGX Cloud Banking 2030 FsiMoidin AfsanNo ratings yet

- Fee ReceiptDocument1 pageFee ReceiptFinch HeroldNo ratings yet

- Unit-5&6 Inst. Support To Ent. in Nepal-2Document65 pagesUnit-5&6 Inst. Support To Ent. in Nepal-2notes.mcpu0% (2)

- The Star SydneyDocument12 pagesThe Star SydneyKLIOMARIE ANNE CURUGANNo ratings yet

- What Is Enterprise Agility and Why Is It ImportantDocument4 pagesWhat Is Enterprise Agility and Why Is It ImportantJaveed A. KhanNo ratings yet

- Review of Related Literature OutlineDocument4 pagesReview of Related Literature OutlineSiote ChuaNo ratings yet

- Principles of Taxation Law 2022 Chapter4Document30 pagesPrinciples of Taxation Law 2022 Chapter4Kaylah NewcombeNo ratings yet

- Reflection Paper 2 (MM)Document1 pageReflection Paper 2 (MM)Paul Irineo MontanoNo ratings yet

- Income Under The Head Capital Gains: LTCG Arising From The Transfer of RHP and Is Reinvested in New RHP (Exemption U/s 54)Document14 pagesIncome Under The Head Capital Gains: LTCG Arising From The Transfer of RHP and Is Reinvested in New RHP (Exemption U/s 54)dosadNo ratings yet

- 84 UCin LRev 327Document23 pages84 UCin LRev 327Shashwat BaranwalNo ratings yet

- CPAR 92 AUD-1st PB SolDocument3 pagesCPAR 92 AUD-1st PB SolEmmanuel TeoNo ratings yet

- HDFC Bank Notice For SettlementDocument1 pageHDFC Bank Notice For Settlementtomarankit44No ratings yet