You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Dictionary of Home Loan FinancingDocument16 pagesDictionary of Home Loan FinancingnetworkcapitalNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 1519 Loza, JesusDocument17 pages1519 Loza, JesusIsabella Kings100% (1)

- Efficient Capital MarketsDocument25 pagesEfficient Capital MarketsAshik Ahmed NahidNo ratings yet

- Debt Recovery Management of SBIDocument128 pagesDebt Recovery Management of SBIpranjalamishra100% (6)

- Exercise #1: Transactions of Bud's Computer Are As FollowsDocument19 pagesExercise #1: Transactions of Bud's Computer Are As FollowsMejias, Janrey80% (10)

- The General Relationship Between Bank and Its CustomerDocument9 pagesThe General Relationship Between Bank and Its CustomerAnkit AgarwalNo ratings yet

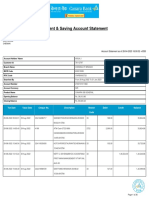

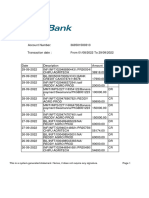

- Current & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiDocument26 pagesCurrent & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiArun Jayaprakash NarayananNo ratings yet

- SKYPE PresentationDocument6 pagesSKYPE PresentationKeshvi AggarwalNo ratings yet

- Mba ProjectDocument100 pagesMba ProjectRajat Aneja67% (3)

- FunctionsDocument2 pagesFunctionsKeshvi AggarwalNo ratings yet

- Article 82189Document7 pagesArticle 82189Keshvi AggarwalNo ratings yet

- Holiday HomeworkDocument22 pagesHoliday HomeworkKeshvi AggarwalNo ratings yet

- MS SQP B.studies 12, Set-1, 2022-23Document5 pagesMS SQP B.studies 12, Set-1, 2022-23Keshvi AggarwalNo ratings yet

- G D Goenka Public School, Jammu: "Liberalisation, Privatisation & Globalisation: An Appraisal"Document4 pagesG D Goenka Public School, Jammu: "Liberalisation, Privatisation & Globalisation: An Appraisal"Keshvi AggarwalNo ratings yet

- Important Terms Ncert (Data) : G D Goenka Public School, JammuDocument3 pagesImportant Terms Ncert (Data) : G D Goenka Public School, JammuKeshvi AggarwalNo ratings yet

- Accounts ProjectDocument20 pagesAccounts ProjectKeshvi Aggarwal0% (1)

- G. D Goenka Public School, Jammu: Class: Xii Subject: Mathematics Name: Roll NoDocument2 pagesG. D Goenka Public School, Jammu: Class: Xii Subject: Mathematics Name: Roll NoKeshvi AggarwalNo ratings yet

- G D Goenka Public School, Jammu: Subject: EconomicsDocument4 pagesG D Goenka Public School, Jammu: Subject: EconomicsKeshvi AggarwalNo ratings yet

- Topics For Als ProjectDocument8 pagesTopics For Als ProjectKeshvi AggarwalNo ratings yet

- G D Goenka Public School, Jammu: "INDIAN ECONOMY 1950-1990"Document3 pagesG D Goenka Public School, Jammu: "INDIAN ECONOMY 1950-1990"Keshvi AggarwalNo ratings yet

- Packing 1Document3 pagesPacking 1Keshvi AggarwalNo ratings yet

- Brief Notes National Income and Related AggregatesDocument1 pageBrief Notes National Income and Related AggregatesKeshvi AggarwalNo ratings yet

- Ipm in Iim JammuDocument16 pagesIpm in Iim JammuKeshvi AggarwalNo ratings yet

- Science Activity The Sun - The Brightest StarDocument6 pagesScience Activity The Sun - The Brightest StarKeshvi AggarwalNo ratings yet

- Biology Holidays HomeworkDocument13 pagesBiology Holidays HomeworkKeshvi AggarwalNo ratings yet

- Bond ValuationDocument3 pagesBond ValuationGauravNo ratings yet

- Partnership FinalDocument4 pagesPartnership FinalJessa Mae Caballero JagnaNo ratings yet

- Death Questions 2022Document2 pagesDeath Questions 2022Tûshar ThakúrNo ratings yet

- PM (Partial Presentation)Document110 pagesPM (Partial Presentation)sampadaNo ratings yet

- Commercial Review DigestDocument180 pagesCommercial Review DigestCassyNo ratings yet

- Answers To End-Of-Chapter Questions 5Document3 pagesAnswers To End-Of-Chapter Questions 5Tommy Jing Jie NgNo ratings yet

- Statement 1664456345829Document7 pagesStatement 16644563458295003743ypunithreddy8No ratings yet

- Financial Reporting 1St Edition Loftus Test Bank Full Chapter PDFDocument31 pagesFinancial Reporting 1St Edition Loftus Test Bank Full Chapter PDFalicebellamyq3yj100% (12)

- Chapter 7 - 18may 2022Document51 pagesChapter 7 - 18may 2022Hazlina HusseinNo ratings yet

- Assignment On Financial ManagementDocument22 pagesAssignment On Financial ManagementSimran VirmaniNo ratings yet

- Banking Assignment 2Document4 pagesBanking Assignment 2Anjali PaneruNo ratings yet

- International Finance 6Document33 pagesInternational Finance 6Hu Jia QuenNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToRichardNoelFernandesNo ratings yet

- M4 Sales & Consumer Protection INCDocument11 pagesM4 Sales & Consumer Protection INCCher NaNo ratings yet

- S&P Debt Rating DefinitionsDocument6 pagesS&P Debt Rating DefinitionsilyakostNo ratings yet

- Time Value of MoneyDocument7 pagesTime Value of Money老坑No ratings yet

- Ross Corporate 13e PPT CH21 AccessibleDocument37 pagesRoss Corporate 13e PPT CH21 AccessibleVy Dang PhuongNo ratings yet

- Mohamed Assem Financial Managment AssignmentDocument10 pagesMohamed Assem Financial Managment AssignmenthananNo ratings yet

- Himali Akarawita Invoice PDFDocument12 pagesHimali Akarawita Invoice PDFAnura PiyatissaNo ratings yet

- New Microsoft Office Word DocumentDocument4 pagesNew Microsoft Office Word DocumentMilan KakkadNo ratings yet

- In Re Rajesh Kumar Gupta of Mahveer Prasad MohanlalDocument20 pagesIn Re Rajesh Kumar Gupta of Mahveer Prasad MohanlalAshish AgarwalNo ratings yet

- Ukk 2023 P2-Kunci Jawaban RevDocument47 pagesUkk 2023 P2-Kunci Jawaban RevSaepul RohmanNo ratings yet