You might also like

- Tales of Peasants, Traders, and Officials: Contracting in Rural Andhra Pradesh, 1980-82From EverandTales of Peasants, Traders, and Officials: Contracting in Rural Andhra Pradesh, 1980-82No ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Akuntansi Account ReceivableDocument8 pagesAkuntansi Account Receivablem habiburrahman55No ratings yet

- Muhammad Alfarizi - 142200278 - Ea-J - Tugas 2 Ap2Document4 pagesMuhammad Alfarizi - 142200278 - Ea-J - Tugas 2 Ap2Muhammad AlfariziNo ratings yet

- Salsse Roofing Services Was Formed On December 01, 2016. The Following Transactions TookDocument7 pagesSalsse Roofing Services Was Formed On December 01, 2016. The Following Transactions TookDipika tasfannum salamNo ratings yet

- EZ Problem Set 8Document3 pagesEZ Problem Set 8Teyang67% (3)

- Solution: P7-3 (L03) Bad-Debt Reporting-Aging: InstructionsDocument8 pagesSolution: P7-3 (L03) Bad-Debt Reporting-Aging: InstructionsHerry SugiantoNo ratings yet

- Chapter 8: Accounting For Receivables: Exercise 1Document45 pagesChapter 8: Accounting For Receivables: Exercise 1jokerightwegmail.com joke1233No ratings yet

- Worksheet ProblemDocument4 pagesWorksheet Problemusernames358No ratings yet

- P9-3A Journalize Entries To Record Transactions Related To Bad DebtsDocument1 pageP9-3A Journalize Entries To Record Transactions Related To Bad DebtsDrenyar ScoutNo ratings yet

- Chapter 9Document7 pagesChapter 9Saharin Islam ShakibNo ratings yet

- Exa Final ACCO500 5 6 8 10 13 Jun 2020Document9 pagesExa Final ACCO500 5 6 8 10 13 Jun 2020Omar PerezNo ratings yet

- Review CH 08Document7 pagesReview CH 08Martin Putra100% (1)

- Review CH 08Document7 pagesReview CH 08Lalala100% (1)

- HW Chap 8Document5 pagesHW Chap 8uong huonglyNo ratings yet

- Auditing Answers To ProblemDocument6 pagesAuditing Answers To ProblemAngela CondeNo ratings yet

- 4 Solution Exam Auditing 2Document5 pages4 Solution Exam Auditing 2Kristina KittyNo ratings yet

- Mock 1 Mid-Term Exam (Answers and Explanations)Document8 pagesMock 1 Mid-Term Exam (Answers and Explanations)100519554No ratings yet

- CH 7 ExcelDocument29 pagesCH 7 ExcelGAANo ratings yet

- Assigment 14Document8 pagesAssigment 14cecilia angelNo ratings yet

- Review Quiz Inter1Document9 pagesReview Quiz Inter1Vanessa vnssNo ratings yet

- ACCT 213 ExerciseDocument5 pagesACCT 213 ExerciseMohammedNo ratings yet

- 1712 Acct6174 Tmba TK4-W10-S15-R2 Team2Document7 pages1712 Acct6174 Tmba TK4-W10-S15-R2 Team2Adzinta Syamsa100% (1)

- 87549654Document3 pages87549654Joel Christian Mascariña100% (1)

- Assignment 1 Acounting 2011 (Repaired)Document13 pagesAssignment 1 Acounting 2011 (Repaired)Vishal PatelNo ratings yet

- Acctg 115 - CH 7 SolutionsDocument9 pagesAcctg 115 - CH 7 SolutionsShehryaar MunirNo ratings yet

- 16 UNIT III LiquidationDocument20 pages16 UNIT III LiquidationLeslie Mae Vargas ZafeNo ratings yet

- Madelyn Rialubin Travel Agency Adjusting Entries AdjustedDocument5 pagesMadelyn Rialubin Travel Agency Adjusting Entries AdjustedJustine Almodiel100% (1)

- CH 2Document40 pagesCH 2danaNo ratings yet

- ACCT 315 AssignmentDocument11 pagesACCT 315 AssignmenthumaNo ratings yet

- Exam PapersDocument8 pagesExam PapersTASH TASHNANo ratings yet

- Financial Accounting 7th Edition Harrison Solutions ManualDocument32 pagesFinancial Accounting 7th Edition Harrison Solutions Manualmelioraque2bd0v100% (23)

- Financial Accounting 7Th Edition Harrison Solutions Manual Full Chapter PDFDocument53 pagesFinancial Accounting 7Th Edition Harrison Solutions Manual Full Chapter PDFMichaelMurrayewrsd100% (11)

- Accounting For Trade Receivables (Accounts Receivable) - Continuation 11Document5 pagesAccounting For Trade Receivables (Accounts Receivable) - Continuation 11rufamaegarcia07No ratings yet

- Chapter 4, Accounting CycleDocument13 pagesChapter 4, Accounting CyclekhanNo ratings yet

- Sample Worksheet K204050266 P3.5Document16 pagesSample Worksheet K204050266 P3.5Trâm Mai Thị ThùyNo ratings yet

- Government Technical Institute Business Department Accounts Revision Worksheet ONEDocument4 pagesGovernment Technical Institute Business Department Accounts Revision Worksheet ONEKen GulliverNo ratings yet

- Problems Chapter 7 PDFDocument9 pagesProblems Chapter 7 PDFCa AdaNo ratings yet

- Name: Lecturer: Course Name: Course CodeDocument6 pagesName: Lecturer: Course Name: Course CodeJaredNo ratings yet

- Class Exercise Sheet FourDocument9 pagesClass Exercise Sheet Fourcarol mohasebNo ratings yet

- Accounting 50 IMP QUESDocument94 pagesAccounting 50 IMP QUESVijayasri KumaravelNo ratings yet

- UTS Ak 1 Genap 2029-2020Document3 pagesUTS Ak 1 Genap 2029-2020Dominica ViolitaNo ratings yet

- 2013 Dse Bafs 2a MS 1Document8 pages2013 Dse Bafs 2a MS 1ryanNo ratings yet

- Chapter 9 ProblemsDocument1 pageChapter 9 ProblemsQasim KhanNo ratings yet

- HW 7Document2 pagesHW 7Mishalm96No ratings yet

- Tugas Bab 6 Jawaban P 6-3Document2 pagesTugas Bab 6 Jawaban P 6-3Syahirul AlimNo ratings yet

- Solution Problem 8-3aDocument2 pagesSolution Problem 8-3aPlok TingNo ratings yet

- Samia Begum - AccountingDocument36 pagesSamia Begum - AccountingsamiaNo ratings yet

- Drill-Receivables CompressDocument7 pagesDrill-Receivables CompressHannahbea LindoNo ratings yet

- Drill - ReceivablesDocument7 pagesDrill - ReceivablesMark Domingo MendozaNo ratings yet

- HUM 121assignment 1Document6 pagesHUM 121assignment 1Nayeem HossainNo ratings yet

- Financial Analysis - Ratio IllustrationsDocument10 pagesFinancial Analysis - Ratio IllustrationsDarshana RNo ratings yet

- Chapter 7 Correction of Errors (II) TestDocument6 pagesChapter 7 Correction of Errors (II) Test陳韋佳No ratings yet

- Handout 7.studentDocument6 pagesHandout 7.studentVikrant KapoorNo ratings yet

- Answers To Extra QuestionsDocument8 pagesAnswers To Extra QuestionsHashani KumarasingheNo ratings yet

- 5 FINANCIAL ACCOUNTING I PaperDocument5 pages5 FINANCIAL ACCOUNTING I PaperRhys SinclairNo ratings yet

- Tugas Akm 3Document1 pageTugas Akm 3cindyegaa27No ratings yet

- Ans: A) Journal Entry On Date of Issue Date Account DR CRDocument4 pagesAns: A) Journal Entry On Date of Issue Date Account DR CRHumera AkbarNo ratings yet

- Tugas III Irensyah PayungbuaDocument4 pagesTugas III Irensyah PayungbuaWilliam MangumbanNo ratings yet

- BUS 142 - Exercises CH 8Document22 pagesBUS 142 - Exercises CH 8Jess IcaNo ratings yet

- Posting of BondDocument3 pagesPosting of BondZian felixNo ratings yet

- Assignment 2 CanadaDocument12 pagesAssignment 2 Canadaabdulrahman mohamedNo ratings yet

- Growth and Development of Retail Banking in India: Drivers of Retail BankingDocument17 pagesGrowth and Development of Retail Banking in India: Drivers of Retail BankingDR.B.REVATHYNo ratings yet

- Break Even Answer KeyDocument8 pagesBreak Even Answer Keyyea okayNo ratings yet

- The Following Unadjusted Trial Balance Is For Power Demolition CompanyDocument1 pageThe Following Unadjusted Trial Balance Is For Power Demolition Companytrilocksp SinghNo ratings yet

- Capital Budgeting: Payback PeriodDocument4 pagesCapital Budgeting: Payback PeriodPooja SunkiNo ratings yet

- SAPMDocument26 pagesSAPMJawed KhanNo ratings yet

- International Journal of Bank Marketing: Article InformationDocument27 pagesInternational Journal of Bank Marketing: Article InformationRukmal KalderaNo ratings yet

- Session 23-25 Permissible Deduction From Gross Total IncomeDocument14 pagesSession 23-25 Permissible Deduction From Gross Total Incomeomar zohorianNo ratings yet

- Bid Document PDFDocument107 pagesBid Document PDFMainali IshuNo ratings yet

- Chapter 4Document34 pagesChapter 4Hameed GulNo ratings yet

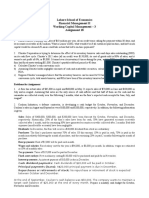

- Lahore School of Economics Financial Management II Working Capital Management - 3 Assignment 18Document2 pagesLahore School of Economics Financial Management II Working Capital Management - 3 Assignment 18SinpaoNo ratings yet

- 010221-SBT (Fy 2011-2012)Document552 pages010221-SBT (Fy 2011-2012)JamesNo ratings yet

- Avocado Set To Become EthiopiaDocument3 pagesAvocado Set To Become Ethiopiasamuel teferiNo ratings yet

- BELTRAN-EAC Company - Balance Sheet and Income StatementDocument2 pagesBELTRAN-EAC Company - Balance Sheet and Income StatementYasmin Pheebie BeltranNo ratings yet

- 1 Can Islamic Banking Ever Become IslamicDocument20 pages1 Can Islamic Banking Ever Become IslamicPT DNo ratings yet

- Asian Paints 22-23 - Statutory ReportsDocument59 pagesAsian Paints 22-23 - Statutory Reportsryarpit0No ratings yet

- FORA Listener Registration FormDocument1 pageFORA Listener Registration FormRaiya MallickNo ratings yet

- FOportal 20220802Document1,476 pagesFOportal 20220802Abhishek0% (1)

- ICAI SEP 2023 - Complete JournalDocument132 pagesICAI SEP 2023 - Complete JournalS M SHEKARNo ratings yet

- Eastboro Machine Tools CorporationDocument19 pagesEastboro Machine Tools CorporationrifkiNo ratings yet

- Payslip - Feb 2023Document1 pagePayslip - Feb 2023Kavin ShanmugamNo ratings yet

- Sample Case DigestDocument2 pagesSample Case DigestAnn Orlina100% (1)

- This Study Resource Was: PAS 2 InventoriesDocument3 pagesThis Study Resource Was: PAS 2 Inventorieshsjhs100% (2)

- The Corporation and The Financial Manager: Fundamentals of Corporate FinanceDocument16 pagesThe Corporation and The Financial Manager: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- GEN ED3 ReviewerDocument3 pagesGEN ED3 ReviewerRishel AlamaNo ratings yet

- Quote U0347886G0Document6 pagesQuote U0347886G0Owen DalyNo ratings yet

- CITN STUDY Pack - International TaxationDocument166 pagesCITN STUDY Pack - International TaxationOguntimehin AdebisolaNo ratings yet

- Assignment 1 SCM - 19BBA10015Document3 pagesAssignment 1 SCM - 19BBA10015KartikNo ratings yet

- Pilipinas Shell Petroleum Corpo RationDocument12 pagesPilipinas Shell Petroleum Corpo RationCario Mary Cris DaanoyNo ratings yet