You might also like

- Firstprogress Cardholder AgreementDocument12 pagesFirstprogress Cardholder Agreementdeskmaster90No ratings yet

- Diners Club Cardmember Agreement SummaryDocument10 pagesDiners Club Cardmember Agreement SummaryEric WeiNo ratings yet

- Barcalys AgreementDocument12 pagesBarcalys AgreementChristopher PierceNo ratings yet

- Merrick Bank Unsecured AgreementDocument2 pagesMerrick Bank Unsecured AgreementNneka Ojimba100% (1)

- Cardmember Agreement - Diners Club Charge CardDocument16 pagesCardmember Agreement - Diners Club Charge CardEric WeiNo ratings yet

- Secured Variable UpDocument16 pagesSecured Variable UpEarl SalyerNo ratings yet

- Orchard Bank 288451024 - AgreementNPI2701ADocument15 pagesOrchard Bank 288451024 - AgreementNPI2701AKestrel1940No ratings yet

- Personal Card Agreement 011221 033122 enDocument9 pagesPersonal Card Agreement 011221 033122 enfukuiu505No ratings yet

- Credit Card Agreement and Disclosure Statement 104Document4 pagesCredit Card Agreement and Disclosure Statement 104Jane OfendaNo ratings yet

- GoldChargeCard FullTnCDocument16 pagesGoldChargeCard FullTnCDgusta2No ratings yet

- Destiny 200Document11 pagesDestiny 200Jeanine WallaceNo ratings yet

- AMA PenFed Platinum Cash Rewards-Pricing List InfoDocument4 pagesAMA PenFed Platinum Cash Rewards-Pricing List InfomattermarkusNo ratings yet

- Kikoff Credit Account Agreement PricingDocument9 pagesKikoff Credit Account Agreement PricingH.I.M Dr. Lawiy ZodokNo ratings yet

- Opensky Secured Visa Credit Cardholder Agreement: Interest Rates and Interest ChargesDocument14 pagesOpensky Secured Visa Credit Cardholder Agreement: Interest Rates and Interest ChargesChris brownNo ratings yet

- Cred Account AgreementDocument24 pagesCred Account AgreementJermaine ReynoldsNo ratings yet

- 2146749Document14 pages2146749Frank CasaleNo ratings yet

- Card Savings Account TermsDocument5 pagesCard Savings Account TermsborgosdNo ratings yet

- Noc Ip Payroll CH AgreementDocument7 pagesNoc Ip Payroll CH AgreementAlejuanchis Kamacho GarciaNo ratings yet

- Secured Personal Terms EnDocument8 pagesSecured Personal Terms Enluiscelis01No ratings yet

- Business Debit DisclosureDocument5 pagesBusiness Debit DisclosureashleyNo ratings yet

- Wamu Arbitration AgreementDocument12 pagesWamu Arbitration AgreementLUENo ratings yet

- Scotiabank Revolving Credit AgreementDocument4 pagesScotiabank Revolving Credit AgreementKendra MangioneNo ratings yet

- Build Card Military Lending Act Cardholder AgreementDocument8 pagesBuild Card Military Lending Act Cardholder Agreementprateekmehta92No ratings yet

- 2023-07-17T10 22 47 LoanAgreement 691671Document9 pages2023-07-17T10 22 47 LoanAgreement 691671juantirado0777No ratings yet

- Bbva Clearspend Card Terms and ConditionsDocument15 pagesBbva Clearspend Card Terms and ConditionsKahtanNo ratings yet

- Consumer Account AgreementDocument20 pagesConsumer Account AgreementjeevankombanNo ratings yet

- World_Mastercard_Insurance_enDocument28 pagesWorld_Mastercard_Insurance_enbrinksbabyclothingNo ratings yet

- CC Purchase Assurance enDocument24 pagesCC Purchase Assurance enReeman432No ratings yet

- Goldman Sachs Apple Card Customer AgreementDocument15 pagesGoldman Sachs Apple Card Customer AgreementJack PurcherNo ratings yet

- Credit Card Statement DisclosureDocument1 pageCredit Card Statement DisclosureShahnaz NawazNo ratings yet

- Apple Card Customer AgreementDocument16 pagesApple Card Customer AgreementAppleNo ratings yet

- Revolut Sutton Bank TermsDocument17 pagesRevolut Sutton Bank TermsKevin Parker100% (1)

- Visa AgreementDocument6 pagesVisa AgreementRaheem ParnellNo ratings yet

- OnlineuseragreementDocument10 pagesOnlineuseragreementLaGrosseTruite DeCombatNo ratings yet

- Consent to Electronic CommunicationsDocument9 pagesConsent to Electronic CommunicationsLiliana MendozaNo ratings yet

- Indigo 602Document15 pagesIndigo 602OneNationNo ratings yet

- Deposit Account EssentialsDocument30 pagesDeposit Account EssentialsmattloyaltyNo ratings yet

- b9048099-e72b-4e8a-8671-7e754a10a30bDocument30 pagesb9048099-e72b-4e8a-8671-7e754a10a30bjoshuaharaldNo ratings yet

- Example of Credit Card Agreement For Bank of America® Visa Signature® AccountsDocument13 pagesExample of Credit Card Agreement For Bank of America® Visa Signature® AccountsDEShifNo ratings yet

- Cardmember Agreement - Diners Club Card EliteDocument16 pagesCardmember Agreement - Diners Club Card EliteEric WeiNo ratings yet

- 2005 HSBC Agreement With JAMSDocument4 pages2005 HSBC Agreement With JAMSrdowninNo ratings yet

- 2020 Dec Credit Cards Terms and ConditionsDocument9 pages2020 Dec Credit Cards Terms and Conditionsやま ひかりNo ratings yet

- Ca en Rca CCDDocument7 pagesCa en Rca CCDChris CutraraNo ratings yet

- Including The Long Form Fee Disclosure ("List of All Fees.")Document9 pagesIncluding The Long Form Fee Disclosure ("List of All Fees.")Shamara LoganNo ratings yet

- "Registering Your Card" and "Personal Identification Number"Document11 pages"Registering Your Card" and "Personal Identification Number"Ivan MilosavljevicNo ratings yet

- 2020 July Credit Cards Terms and ConditionsDocument8 pages2020 July Credit Cards Terms and ConditionsPJFilm-ElijahNo ratings yet

- BMO AIR MILES®† World Elite®* MasterCard®* card Information GuideDocument56 pagesBMO AIR MILES®† World Elite®* MasterCard®* card Information Guidemahmoud jalloulNo ratings yet

- Loan Agreement PDFDocument9 pagesLoan Agreement PDFHengki YonoNo ratings yet

- FreeBlue DAAD MO 1291Document16 pagesFreeBlue DAAD MO 1291zolalaw4No ratings yet

- Wells Fargo Cash Back College Card TermsDocument5 pagesWells Fargo Cash Back College Card TermsataraNo ratings yet

- Chase AgreementDocument30 pagesChase AgreementDijana MitrovicNo ratings yet

- BD Silver Gold Credit Card Terms Conditions BrochureDocument8 pagesBD Silver Gold Credit Card Terms Conditions Brochurehasan raisNo ratings yet

- Certificate of Deposit Account Agreement 2023may31Document12 pagesCertificate of Deposit Account Agreement 2023may31acescamerNo ratings yet

- AchieveCard Prepaid MasterCard Cardholder AgreementDocument18 pagesAchieveCard Prepaid MasterCard Cardholder AgreementAchieve CardNo ratings yet

- Apple Card Customer AgreementDocument19 pagesApple Card Customer AgreementMarian PahNo ratings yet

- Personal Client Agreement: ConfidentialDocument8 pagesPersonal Client Agreement: ConfidentialKobus WilkenNo ratings yet

- Choice - Mercury Commercial Debit Card AgreementDocument7 pagesChoice - Mercury Commercial Debit Card Agreementfulbert.nguessanNo ratings yet

- Signed by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMDocument6 pagesSigned by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMTymon SwaqqCity ScottNo ratings yet

- cardholder-agreement-edv01odcashDocument54 pagescardholder-agreement-edv01odcashTruLuv FaithNo ratings yet

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- Voucher Hotel For Amanda Sasmitha RoroDocument2 pagesVoucher Hotel For Amanda Sasmitha RoroCloud FarisNo ratings yet

- OAA Certificate of ServiceDocument1 pageOAA Certificate of ServiceCloud FarisNo ratings yet

- Formulir Hotel RedemptionDocument1 pageFormulir Hotel RedemptionCloud FarisNo ratings yet

- Voucher Hotel For Sabrina Yura MikhaelDocument2 pagesVoucher Hotel For Sabrina Yura MikhaelCloud FarisNo ratings yet

- Gift Redeem For Blanche Chloé ClementineDocument1 pageGift Redeem For Blanche Chloé ClementineCloud FarisNo ratings yet

- Employee of The Month Sabrina Yura MikhaelDocument1 pageEmployee of The Month Sabrina Yura MikhaelCloud FarisNo ratings yet

- Gift Redeem For Amanda Sasmitha RoroDocument1 pageGift Redeem For Amanda Sasmitha RoroCloud FarisNo ratings yet

- EMPLOYEE OF THE MONTH Amanda Sasmitha RoroDocument1 pageEMPLOYEE OF THE MONTH Amanda Sasmitha RoroCloud FarisNo ratings yet

- Employee of The Month Blanche Chloe ClementineDocument1 pageEmployee of The Month Blanche Chloe ClementineCloud FarisNo ratings yet

- Code of Conduct 2021Document94 pagesCode of Conduct 2021Rian Rizki YantamaNo ratings yet

- CFPB Electronicb Filing ProceduresDocument4 pagesCFPB Electronicb Filing ProceduresCloud FarisNo ratings yet

- Pedoman Tata Kelola Perusahaan Yang BaikDocument132 pagesPedoman Tata Kelola Perusahaan Yang BaikCloud FarisNo ratings yet

- Accountancy 17Document12 pagesAccountancy 17Manav GargNo ratings yet

- Tugas 4 Dasar AkuntansiDocument20 pagesTugas 4 Dasar AkuntansiAji Surya Wijaya75% (4)

- DemoDocument3 pagesDemoEngr Muhammad Khaliq UtroriNo ratings yet

- Tutorial 2 Business Entities #1Document3 pagesTutorial 2 Business Entities #1Shannan RichardsNo ratings yet

- Journal, Ledger TB - Problems SolutionsDocument14 pagesJournal, Ledger TB - Problems Solutionssri lekhaNo ratings yet

- Chapter 19: Audit of Owners' Equity: Review QuestionsDocument18 pagesChapter 19: Audit of Owners' Equity: Review QuestionsReznakNo ratings yet

- Preliminary Examination: Multiple ChoiceDocument4 pagesPreliminary Examination: Multiple ChoiceNita Costillas De MattaNo ratings yet

- Name: Year & Course: SubjectDocument15 pagesName: Year & Course: Subjectshella mae pormento100% (1)

- W2 Module 2 - Financial Statement AnalysisDocument6 pagesW2 Module 2 - Financial Statement AnalysisDanica Vetuz100% (1)

- SWORN STATEMENT OF ASSETS AND LIABILITIESDocument2 pagesSWORN STATEMENT OF ASSETS AND LIABILITIES아오아오No ratings yet

- Chapter 1-5 Book 1Document42 pagesChapter 1-5 Book 1Krizel Dixie ParraNo ratings yet

- Pre Fi NotesDocument35 pagesPre Fi NotesMikMik UyNo ratings yet

- Chapter 4 - Financial Statements of CompaniesDocument198 pagesChapter 4 - Financial Statements of CompaniesVaidehee MishraNo ratings yet

- 13 Comm 308 Final Exam (Summer 1, 2012) SolutionsDocument17 pages13 Comm 308 Final Exam (Summer 1, 2012) SolutionsAfafe ElNo ratings yet

- BPI v. RoxasDocument2 pagesBPI v. RoxasYvette MoralesNo ratings yet

- Chapter 21 Dispositions of Partnership Interests and Partnership Distributions 2Document9 pagesChapter 21 Dispositions of Partnership Interests and Partnership Distributions 2Doreen0% (1)

- Hire Purchase AgreementDocument7 pagesHire Purchase AgreementNNENNA NWAHIRI100% (4)

- ACCY121 - REPORT - TND SquadDocument17 pagesACCY121 - REPORT - TND SquadToànNo ratings yet

- Credit, Collection and Compliance Application 1 - Introduction To CreditDocument5 pagesCredit, Collection and Compliance Application 1 - Introduction To CreditGabriel Matthew Lanzarfel GabudNo ratings yet

- Business Law MCQ 2020 MCQDocument17 pagesBusiness Law MCQ 2020 MCQAnseeta SajeevanNo ratings yet

- Shell Pilipinas Corporation Audited Financial StatementsDocument112 pagesShell Pilipinas Corporation Audited Financial StatementsKYLA RENZ DE LEONNo ratings yet

- Dubois Bank Protected as Holder in Due CourseDocument2 pagesDubois Bank Protected as Holder in Due CourseClaudine Allyson DungoNo ratings yet

- With a Period (1193): Key ConceptsDocument39 pagesWith a Period (1193): Key ConceptsTanya KimNo ratings yet

- Format of Financial StatementsDocument2 pagesFormat of Financial StatementsAmeerul HarithNo ratings yet

- Lesson 3 - AccountsDocument13 pagesLesson 3 - AccountsJeyem AscueNo ratings yet

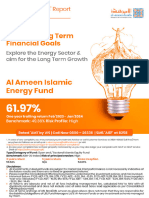

- Al Ameen Funds-Fund Manager Report-Jan-2024Document21 pagesAl Ameen Funds-Fund Manager Report-Jan-2024aniqa.asgharNo ratings yet

- Accounting in Tally PrimeDocument5 pagesAccounting in Tally PrimeNiladri SenNo ratings yet

- Chapter 1Document18 pagesChapter 1clarizaNo ratings yet

- AICO - Unbundling November 2013Document3 pagesAICO - Unbundling November 2013addyNo ratings yet

- Solved MR Carlsen Was Sued by Financial Collection Services For OutstandingDocument1 pageSolved MR Carlsen Was Sued by Financial Collection Services For OutstandingAnbu jaromiaNo ratings yet