You might also like

- Contoh Soal Analisa Keputusan Keadaan Variabel Random Dan Decision Under UncertainlyDocument8 pagesContoh Soal Analisa Keputusan Keadaan Variabel Random Dan Decision Under UncertainlyEssy DoankNo ratings yet

- MGT 115 Removal Exam 1S AY 2017 2018 25 Sept 2018Document6 pagesMGT 115 Removal Exam 1S AY 2017 2018 25 Sept 2018Kadita MageNo ratings yet

- Advanced Corporate Finance Case 1Document2 pagesAdvanced Corporate Finance Case 1Adrien PortemontNo ratings yet

- Mulcher Cash Flow EstimationDocument8 pagesMulcher Cash Flow EstimationvarunjajooNo ratings yet

- Assignment 1 20 F-0023Document7 pagesAssignment 1 20 F-0023maheen iqbalNo ratings yet

- GFW Investment Calculator: Total 206,700Document4 pagesGFW Investment Calculator: Total 206,700Tvyan RaajNo ratings yet

- Regression StatisticsDocument10 pagesRegression StatisticsNovia SukmawatiNo ratings yet

- 25 Days Trading ProfitDocument1 page25 Days Trading Profitmubbigamer2No ratings yet

- Auro Chit New Payment ChartDocument1 pageAuro Chit New Payment Chartbest southNo ratings yet

- Balanta de Verificare CompletataDocument1 pageBalanta de Verificare CompletataAndreea AntonNo ratings yet

- AssignmentDocument120 pagesAssignmentPrashant MakwanaNo ratings yet

- NPVDocument1 pageNPVfreakcricket80No ratings yet

- Analysis: Calculation of Total Sales of The ProjectDocument7 pagesAnalysis: Calculation of Total Sales of The ProjectShailesh Kumar BaldodiaNo ratings yet

- Capital Investment Decisions Answers To End of Chapter ExercisesDocument3 pagesCapital Investment Decisions Answers To End of Chapter ExercisesJay BrockNo ratings yet

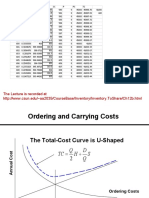

- The Lecture Is Recorded atDocument37 pagesThe Lecture Is Recorded atLuisa Maria CarabaliNo ratings yet

- Generated Through CPM (New Then Crashing)Document14 pagesGenerated Through CPM (New Then Crashing)Aiman BaigNo ratings yet

- Financier ADocument9 pagesFinancier Aesneiderdej.villeraNo ratings yet

- Tanishka Jain 210765Document48 pagesTanishka Jain 210765tanishkajain129No ratings yet

- Capital Budgeting BSNLDocument10 pagesCapital Budgeting BSNLAşhwįnį GawasNo ratings yet

- Ficl Lab 3Document3 pagesFicl Lab 3JoséMoralesRamírezNo ratings yet

- ABC Product ListingDocument128 pagesABC Product Listingerwin abiansyahNo ratings yet

- Book Method (Matrix) : Calculating IRRDocument9 pagesBook Method (Matrix) : Calculating IRRAli SaeedNo ratings yet

- Annual Report 2075 76 EnglishDocument200 pagesAnnual Report 2075 76 Englishram krishnaNo ratings yet

- Ingreso Anuales de Amzon 2Document2 pagesIngreso Anuales de Amzon 2Leonel ColqueNo ratings yet

- Business Simulation Team-HDocument12 pagesBusiness Simulation Team-Hpawan vermaNo ratings yet

- Muhammad Usman 2077 Cert 4 AccountingDocument10 pagesMuhammad Usman 2077 Cert 4 AccountinggazanNo ratings yet

- McReath Original SolutionDocument2 pagesMcReath Original SolutionSuchi0% (1)

- Revised-Installment-of-all-Scheme - 14-05-2020Document3 pagesRevised-Installment-of-all-Scheme - 14-05-2020Toufiqur Rahman SiamNo ratings yet

- Alee Bookkeeping Alleee Letter Asad Anayat-Luzia Anayat - OT Najeeb Naeem Saqib Return Event Return Waseem Retyrn Classic ReturnDocument6 pagesAlee Bookkeeping Alleee Letter Asad Anayat-Luzia Anayat - OT Najeeb Naeem Saqib Return Event Return Waseem Retyrn Classic ReturnIkramNo ratings yet

- FM pracDocument15 pagesFM pracanushkas0701No ratings yet

- M4 1Document3 pagesM4 1KakifejNo ratings yet

- TrialDocument43 pagesTrialArun PuniaNo ratings yet

- Case 1Document4 pagesCase 1imi.imtenanNo ratings yet

- Quiz 2 TableDocument5 pagesQuiz 2 TableSathish BNo ratings yet

- Mat Foundation Design CalculationsDocument12 pagesMat Foundation Design CalculationsjoanNo ratings yet

- Time schedule and cost analysis of building construction projectDocument24 pagesTime schedule and cost analysis of building construction projectAgie Ramdiansyah NurrahmanNo ratings yet

- SDM - Assignment 2Document5 pagesSDM - Assignment 2AryanNo ratings yet

- Tarea RedesDocument7 pagesTarea RedesDaniel MantillaNo ratings yet

- Bajaj Finserv ReportDocument6 pagesBajaj Finserv ReportAdarsh ChavelNo ratings yet

- AFDM - W9S - Seminar PB, ARR, NPV, IRRDocument1 pageAFDM - W9S - Seminar PB, ARR, NPV, IRRsamNo ratings yet

- Bolt Clamping Load ChartsDocument1 pageBolt Clamping Load ChartssourajpatelNo ratings yet

- Alano Julius N. TM 205 - Financial and Cost Analysis For Technology Managers 2018-20700 S (9:00AM-12:00PM)Document1 pageAlano Julius N. TM 205 - Financial and Cost Analysis For Technology Managers 2018-20700 S (9:00AM-12:00PM)Julius AlanoNo ratings yet

- Rata Rata PBV 2.55 Rata Rata Roe 19 Harga Wajar Bbri Dengan PBV Rata Rata 5 Tahun 3,790 Harga Future Dengan Roe Rata Rata 5 Tahun Tahun Target HargaDocument4 pagesRata Rata PBV 2.55 Rata Rata Roe 19 Harga Wajar Bbri Dengan PBV Rata Rata 5 Tahun 3,790 Harga Future Dengan Roe Rata Rata 5 Tahun Tahun Target HargaAdnanNo ratings yet

- P P K H H S X NX N: IN6331 Assignment 6 Part 2 SolutionDocument4 pagesP P K H H S X NX N: IN6331 Assignment 6 Part 2 SolutionManohar MjmNo ratings yet

- Financial Plan of Chemical Industry: Amardeep PigmentDocument17 pagesFinancial Plan of Chemical Industry: Amardeep Pigmentsant1306No ratings yet

- Chit SheetDocument3 pagesChit SheetvcpavithraNo ratings yet

- PPF CalculatorDocument2 pagesPPF CalculatorshashanamouliNo ratings yet

- Year Project 1-Low Risk Project 2-High Risk Project 3 - Medium RiskDocument3 pagesYear Project 1-Low Risk Project 2-High Risk Project 3 - Medium RiskAkshaya LakshminarasimhanNo ratings yet

- 29 Days Trading PlanDocument1 page29 Days Trading Planmubbigamer2No ratings yet

- Q3 Yearly financial projections and cash flow analysisDocument3 pagesQ3 Yearly financial projections and cash flow analysissumera dervishNo ratings yet

- Exam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCADocument1 pageExam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCAAbdoNo ratings yet

- Laporan Setio 09'21Document144 pagesLaporan Setio 09'21SetiohomedecorNo ratings yet

- Operation Expenses and Sales Analysis for Stationery Business Over 5 YearsDocument31 pagesOperation Expenses and Sales Analysis for Stationery Business Over 5 YearsJanine PadillaNo ratings yet

- September 2013 NPVDocument6 pagesSeptember 2013 NPVShahriar KabirNo ratings yet

- Bulan Praoperasi 1 2 3 4Document11 pagesBulan Praoperasi 1 2 3 4Aqilah SufianNo ratings yet

- Preference Shares - November 6 2019Document1 pagePreference Shares - November 6 2019Tiso Blackstar GroupNo ratings yet

- ENPV - REVISION LECTURE Solution ACTIVITYDocument4 pagesENPV - REVISION LECTURE Solution ACTIVITYRafael StoicanNo ratings yet

- 223-NIdhi RathodDocument33 pages223-NIdhi RathodNidhi RathodNo ratings yet

- Student Support - Module 1-TVMDocument16 pagesStudent Support - Module 1-TVMZeusNo ratings yet

- Cost Slope Crashing CalculationDocument3 pagesCost Slope Crashing Calculationmadam iqraNo ratings yet

- Finding Patterns Through Analysis of Financial RatiosDocument4 pagesFinding Patterns Through Analysis of Financial Ratiosmadam iqraNo ratings yet

- Major Assignment 2 GuidelinesDocument4 pagesMajor Assignment 2 Guidelinesmadam iqraNo ratings yet

- FinanceDocument9 pagesFinancemadam iqraNo ratings yet

- Mobile PhoneDocument2 pagesMobile Phonemadam iqraNo ratings yet

- Topic Debenhams SWOT AnalysisDocument5 pagesTopic Debenhams SWOT Analysismadam iqraNo ratings yet

- Case Study DebenhamsDocument4 pagesCase Study Debenhamsmadam iqraNo ratings yet

- BOOM FINAL PR - EditedDocument10 pagesBOOM FINAL PR - Editedmadam iqraNo ratings yet

- Types of Financial Swaps ExplainedDocument3 pagesTypes of Financial Swaps Explainedmadam iqraNo ratings yet

- MGBBTOOSE: Orientation For Success in Higher Education in Business and Tourism ManagementDocument6 pagesMGBBTOOSE: Orientation For Success in Higher Education in Business and Tourism Managementmadam iqraNo ratings yet

- Finance Interview QuestionsDocument15 pagesFinance Interview QuestionsJitendra BhandariNo ratings yet

- Stryker Corp: In-Sourcing PCB Manufacturing Saves $10MDocument5 pagesStryker Corp: In-Sourcing PCB Manufacturing Saves $10MYulfaizah Mohd Yusoff100% (6)

- BEC 3 Outline - 2015 Becker CPA ReviewDocument4 pagesBEC 3 Outline - 2015 Becker CPA ReviewGabrielNo ratings yet

- Group 3 Aia ReportDocument26 pagesGroup 3 Aia ReportNAVAS E VNo ratings yet

- Phuket Beach Resort Case Analysis: Planet Karaoke Pub vs Beach Karaoke PubDocument23 pagesPhuket Beach Resort Case Analysis: Planet Karaoke Pub vs Beach Karaoke PubTosheef Allen Kropenski100% (1)

- Sinclair Company Group Case StudyDocument20 pagesSinclair Company Group Case StudyNida AmriNo ratings yet

- Knights International Facility Investment AnalysisDocument16 pagesKnights International Facility Investment AnalysisMuhammad SaadNo ratings yet

- Sensitivity Analysis: 1. Revenue Sensitivity: Major Inputs To The Revenue Estimation AreDocument3 pagesSensitivity Analysis: 1. Revenue Sensitivity: Major Inputs To The Revenue Estimation AreVn RaghuveerNo ratings yet

- Hasil Diskusi 8 Manajemen KeuanganDocument4 pagesHasil Diskusi 8 Manajemen KeuanganTtsani TsaniNo ratings yet

- 23ATT033RFPDocument14 pages23ATT033RFPResearch GatewayNo ratings yet

- Corporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFDocument35 pagesCorporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFvernon.amundson153100% (10)

- Investment Evaluation MethodDocument13 pagesInvestment Evaluation MethodBAo TrAmNo ratings yet

- Informe - 468 - 18-11-2022bDocument44 pagesInforme - 468 - 18-11-2022bMadahi Katherine Garcia MedranoNo ratings yet

- $845.07 Thus, The Price of The Bond Is $845.07Document16 pages$845.07 Thus, The Price of The Bond Is $845.07Vani Prince TyagiNo ratings yet

- Corporate Valuation of Saas Companies: A Case Study Of: ISM International School of Management, Paris, FranceDocument15 pagesCorporate Valuation of Saas Companies: A Case Study Of: ISM International School of Management, Paris, FranceМаксим ЧернышевNo ratings yet

- Summary - Strategic Database Marketing - Arthur M. HughesDocument51 pagesSummary - Strategic Database Marketing - Arthur M. Hughesjkivit100% (1)

- 01 Capital BudgetingDocument25 pages01 Capital Budgetingkimngantong103No ratings yet

- Chapter 13 Equity ValuationDocument33 pagesChapter 13 Equity Valuationsharktale2828No ratings yet

- Principles of Corporate Finance 12th Edition Brealey Test Bank Chapter 02Document18 pagesPrinciples of Corporate Finance 12th Edition Brealey Test Bank Chapter 02Hassane AmadouNo ratings yet

- Libyan InvestmentsDocument20 pagesLibyan InvestmentsAyam ZebossNo ratings yet

- Net Present Value and Other Investment Rules: Multiple Choice QuestionsDocument22 pagesNet Present Value and Other Investment Rules: Multiple Choice QuestionsraymondNo ratings yet

- Accounting 9th Edition Horngren Solution ManualDocument19 pagesAccounting 9th Edition Horngren Solution ManualAsa100% (1)

- Practical Examples of Operations Research: Example 1 (Giapetto' S Woodcarving)Document12 pagesPractical Examples of Operations Research: Example 1 (Giapetto' S Woodcarving)Karlus TomasNo ratings yet

- Capital BudgetingDocument4 pagesCapital BudgetingNirav TibraNo ratings yet

- Haramaya University Sheep and Goat FatteDocument23 pagesHaramaya University Sheep and Goat FatteAbelNo ratings yet

- Case StudyDocument136 pagesCase StudyNadeem AhmadNo ratings yet

- Financial Management & International Finance QuestionsDocument15 pagesFinancial Management & International Finance QuestionsTarunSainiNo ratings yet

- Capital BudgetingDocument50 pagesCapital Budgetinghimanshujoshi7789No ratings yet

- Excel'S NPV FunctionDocument41 pagesExcel'S NPV FunctionSyed Ameer Ali ShahNo ratings yet

- Session 7 - Make or Buy StrategyDocument33 pagesSession 7 - Make or Buy StrategyChung HeiNo ratings yet