You might also like

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- Amendment Booklet GST CA CMA CS Inter MAY 2023 ExamsDocument57 pagesAmendment Booklet GST CA CMA CS Inter MAY 2023 ExamsPRATHAM AGGARWALNo ratings yet

- Solvents and Their Nomenclauture PDFDocument10 pagesSolvents and Their Nomenclauture PDFAashish GauravNo ratings yet

- 11608-Driving Women Fiction and PDFDocument240 pages11608-Driving Women Fiction and PDFAleksi KnuutilaNo ratings yet

- 6.case Study On Input Tax Credit Under GSTDocument17 pages6.case Study On Input Tax Credit Under GSTSUNIL PUJARINo ratings yet

- Vic Mamalateo (Tax Remedies) PDFDocument51 pagesVic Mamalateo (Tax Remedies) PDFMV FadsNo ratings yet

- Ryanair Strategic AnalysisDocument36 pagesRyanair Strategic AnalysisAlmas Uddin100% (1)

- Capital Expenditure Decision Making ToolsDocument19 pagesCapital Expenditure Decision Making ToolsRoshan PoudelNo ratings yet

- Australia vs. France ReportDocument5 pagesAustralia vs. France ReportammeNo ratings yet

- EIA For Maize & Wheat Milling Plant DEI PDFDocument110 pagesEIA For Maize & Wheat Milling Plant DEI PDFSasira Fionah100% (2)

- 2018 Albano Doctrine On INCOME Taxation For The 2018 Bar ExamDocument14 pages2018 Albano Doctrine On INCOME Taxation For The 2018 Bar ExamNissi JonnaNo ratings yet

- Supreme Court Rules Japanese Firm Exempt from Taxes Under Exchange of NotesDocument17 pagesSupreme Court Rules Japanese Firm Exempt from Taxes Under Exchange of NotesAnonymous VtsflLix1No ratings yet

- Atok Finance Corporation vs. Court of AppealsDocument3 pagesAtok Finance Corporation vs. Court of AppealsAngelica Abalos100% (1)

- Arellano LMT TaxDocument32 pagesArellano LMT TaxGretchen Alunday SuarezNo ratings yet

- GST - CGST - Circulars - 178-10-2022 Dated - 03 August 2022Document9 pagesGST - CGST - Circulars - 178-10-2022 Dated - 03 August 2022Bhavya JindalNo ratings yet

- Circular - 178.22 PART 1Document2 pagesCircular - 178.22 PART 1welcome dearNo ratings yet

- Bos 59824Document99 pagesBos 59824student 100d0917No ratings yet

- GST on liquidated damagesDocument10 pagesGST on liquidated damageswelcome dearNo ratings yet

- Article - GST On Washout Charges or Liquidated DamagesDocument6 pagesArticle - GST On Washout Charges or Liquidated DamagessupdtconflNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- Project Explores Indirect Tax Concept of Supply Under GSTDocument17 pagesProject Explores Indirect Tax Concept of Supply Under GSTShivani Singh ChandelNo ratings yet

- GST on liquidated damagesDocument8 pagesGST on liquidated damagesVenkataramana NippaniNo ratings yet

- Chapter-2 What Is Taxable and Exempted Unde GSTDocument47 pagesChapter-2 What Is Taxable and Exempted Unde GSTDR. PREETI JINDALNo ratings yet

- GST Amendment For May 23Document29 pagesGST Amendment For May 23Tushar MittalNo ratings yet

- Taxguru - In-Gujarat High Court Decision On The Demerger Scheme Between Vodafone Essar Group CompaniesDocument31 pagesTaxguru - In-Gujarat High Court Decision On The Demerger Scheme Between Vodafone Essar Group CompaniesMudit KediaNo ratings yet

- Decoding Recent Judgements of Supreme Court in Taxes - Part 2Document3 pagesDecoding Recent Judgements of Supreme Court in Taxes - Part 2prithish mNo ratings yet

- Cir 188 20 2022 CGSTDocument4 pagesCir 188 20 2022 CGSTAtanu Kumar SenNo ratings yet

- ELP Indirect Tax Newsletter November 2022Document6 pagesELP Indirect Tax Newsletter November 2022ELP LawNo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- 484b6 Impact Wrong Type of Tax Paid and Wrong Claim of ItcDocument5 pages484b6 Impact Wrong Type of Tax Paid and Wrong Claim of Itc15211 alok AnandNo ratings yet

- IDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFDocument69 pagesIDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFfarhana shaikNo ratings yet

- MSME Has No Limitation Bar For RecoveryDocument5 pagesMSME Has No Limitation Bar For Recoveryseshadrimn seshadrimnNo ratings yet

- Direct Taxes Circular - SecDocument26 pagesDirect Taxes Circular - SecnalluriimpNo ratings yet

- Taxsutra All Rights ReservedDocument7 pagesTaxsutra All Rights ReservedAlpa Shah DesaiNo ratings yet

- Circular No 12 2022Document7 pagesCircular No 12 2022shantXNo ratings yet

- Tax Deduction Guidelines Issued for Section 194RDocument7 pagesTax Deduction Guidelines Issued for Section 194RDEVA1985No ratings yet

- Advantages and Disadvantages of The FloatingDocument22 pagesAdvantages and Disadvantages of The FloatingFarhana KhanNo ratings yet

- Write Back Amount Vs GSTDocument8 pagesWrite Back Amount Vs GSTashim1No ratings yet

- Circular No 18 2022Document6 pagesCircular No 18 2022Manish KumarNo ratings yet

- TOPIC 8 Provisions For Non Unionised Employees As Stipulated in The Employment Act, 1955Document74 pagesTOPIC 8 Provisions For Non Unionised Employees As Stipulated in The Employment Act, 1955LunaNo ratings yet

- 1999 BIR - Ruling - DA 087 99 - 20210505 13 16oil1yDocument2 pages1999 BIR - Ruling - DA 087 99 - 20210505 13 16oil1yJM CBNo ratings yet

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationDocument3 pagesJustice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationNicco AcaylarNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- Paper 19 Dec2023 Syllabus2022Document40 pagesPaper 19 Dec2023 Syllabus2022Abhijith ViratNo ratings yet

- Indirect TaxDocument14 pagesIndirect TaxAzulfa Sultan.No ratings yet

- 194C Detailed AnalysisDocument18 pages194C Detailed AnalysisPuneet kumarNo ratings yet

- UNIT 2 (1) Taxable Event - Printed NotesDocument8 pagesUNIT 2 (1) Taxable Event - Printed NotesSania KhanNo ratings yet

- CIR vs. SMARTDocument14 pagesCIR vs. SMARTRhona MarasiganNo ratings yet

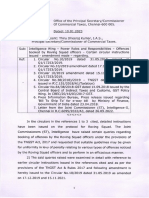

- Power Roles and Responsibilities - Offences Booked by Roving Squad OfficersDocument16 pagesPower Roles and Responsibilities - Offences Booked by Roving Squad OfficersAnandd BabunathNo ratings yet

- Bir Ruling (Da - (C-005) 023-08)Document4 pagesBir Ruling (Da - (C-005) 023-08)Marlene TongsonNo ratings yet

- GST implications of lending transactionsDocument5 pagesGST implications of lending transactionsSakshi DamwaniNo ratings yet

- Analysis of Clause 10CC of Contract AgreementDocument25 pagesAnalysis of Clause 10CC of Contract AgreementMafaka Maxx100% (1)

- GST Applicability On Inter Corporate Guarantees - Taxguru - In-1Document3 pagesGST Applicability On Inter Corporate Guarantees - Taxguru - In-1rkalangiNo ratings yet

- Ap Aar 02 2020 17.02.2020 DecipplDocument7 pagesAp Aar 02 2020 17.02.2020 Decipplshubhamt25No ratings yet

- Vehicle Company MergerDocument9 pagesVehicle Company Mergerhc271105No ratings yet

- Supply-By CA Arpit HaldiaDocument75 pagesSupply-By CA Arpit HaldiaCA Aravind100% (1)

- Titan 544 SCRA 466Document23 pagesTitan 544 SCRA 466Rodolfo TobiasNo ratings yet

- Grp7 Cardillo Sales Zapanta 2nd Exam CasedigestsDocument11 pagesGrp7 Cardillo Sales Zapanta 2nd Exam CasedigestshiltonbraiseNo ratings yet

- Contentious Issues in GST 11.10.2018Document24 pagesContentious Issues in GST 11.10.2018Bathina Srinivasa RaoNo ratings yet

- CTA CasesDocument177 pagesCTA CasesJade Palace TribezNo ratings yet

- Creating - Charges - Under The Companies Act, 2013 - Corporate - Commercial Law - IndiaDocument3 pagesCreating - Charges - Under The Companies Act, 2013 - Corporate - Commercial Law - IndiakaranNo ratings yet

- Input Tax Credit: Cma Bibhudatta SarangiDocument3 pagesInput Tax Credit: Cma Bibhudatta SarangihanumanthaiahgowdaNo ratings yet

- 3 The ICC Uniform Rules For Demand GuaranteesDocument6 pages3 The ICC Uniform Rules For Demand GuaranteesShyamal DuttaNo ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- Charges - Company LawDocument39 pagesCharges - Company LawParag Jain DugarNo ratings yet

- Ethernet Networking EssentialsDocument5 pagesEthernet Networking Essentialsjmiguel000No ratings yet

- Edmonton Report On Flood MitigationDocument6 pagesEdmonton Report On Flood MitigationAnonymous TdomnV9OD4No ratings yet

- Ensure Data Quality in Oracle TCA with DQMDocument17 pagesEnsure Data Quality in Oracle TCA with DQManand.g7720No ratings yet

- How To Write A Evaluation EssayDocument2 pagesHow To Write A Evaluation EssayurdpzinbfNo ratings yet

- Mitchell Board of Education June 26 Meeting AgendaDocument33 pagesMitchell Board of Education June 26 Meeting AgendainforumdocsNo ratings yet

- Study of Altman's Z ScoreDocument8 pagesStudy of Altman's Z ScoreKatarina JovanovićNo ratings yet

- Department of Civil Engineering, Semester 7th: Different Types of BridgesDocument39 pagesDepartment of Civil Engineering, Semester 7th: Different Types of BridgesSiddhartha SahaNo ratings yet

- Walmart Drug ListDocument6 pagesWalmart Drug ListShirley Pigott MDNo ratings yet

- Coal PDFDocument36 pagesCoal PDFurjanagarNo ratings yet

- Unit 1Document176 pagesUnit 1kassahun meseleNo ratings yet

- Chapter 3 - Excel SolutionsDocument8 pagesChapter 3 - Excel SolutionsHalt DougNo ratings yet

- Modified Variable Neighborhood Search Algorithm For Maximum Power Point Tracking in PV Systems Under Partial Shading ConditionsDocument8 pagesModified Variable Neighborhood Search Algorithm For Maximum Power Point Tracking in PV Systems Under Partial Shading ConditionsTELKOMNIKANo ratings yet

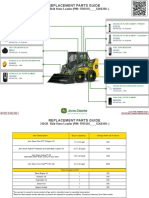

- 312GR Skid Steer Loader PIN 1T0312G G366358 Replacement Parts GuideDocument3 pages312GR Skid Steer Loader PIN 1T0312G G366358 Replacement Parts GuideNelson Andrade VelasquezNo ratings yet

- Altair Flow Simulator 2021.2 Release Notes HighlightsDocument4 pagesAltair Flow Simulator 2021.2 Release Notes HighlightsOliver RailaNo ratings yet

- Databases 2 Exercise Sheet 4Document2 pagesDatabases 2 Exercise Sheet 4Shivam ShuklaNo ratings yet

- Q12 KeyDocument3 pagesQ12 KeyMuhammad AbdullahNo ratings yet

- Media Palnning ProcessDocument3 pagesMedia Palnning ProcessSrinivas KumarNo ratings yet

- 121-Ugong Issue 5.2 - FINAL - Doc - With Corrections-2nd RevisionDocument16 pages121-Ugong Issue 5.2 - FINAL - Doc - With Corrections-2nd RevisionMarq QoNo ratings yet

- Web Browsing and Communication NotesDocument19 pagesWeb Browsing and Communication NotesRahul PandeyNo ratings yet

- Tesco AnalysisDocument12 pagesTesco Analysisdanny_wch7990No ratings yet

- Hello World in FortranDocument43 pagesHello World in Fortranhussein alsaedeNo ratings yet

- Science 10 - Q1 - W5 - D2Document1 pageScience 10 - Q1 - W5 - D2zenaida a academiaNo ratings yet

- Mapua IT LED Display "Boot SequenceDocument10 pagesMapua IT LED Display "Boot SequenceKristine ToledoNo ratings yet

- 200 NsDocument63 pages200 NsSam SamiNo ratings yet