You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- CVP Relevant CostDocument15 pagesCVP Relevant CostSoumya Ranjan PandaNo ratings yet

- Costing Problem and Solution For PracticeDocument8 pagesCosting Problem and Solution For Practicesaradindu123No ratings yet

- JW SPORT SuppliesDocument5 pagesJW SPORT SuppliesVishvesh Soni100% (4)

- Cma Budget ExcelDocument6 pagesCma Budget ExcelDristi SinghNo ratings yet

- Budgetary ControlDocument14 pagesBudgetary ControlCool BuddyNo ratings yet

- 5 Job CostingDocument22 pages5 Job CostingAbimanyu Shenil0% (1)

- Calculate manufacturing costs and operating income given inventory levelsDocument9 pagesCalculate manufacturing costs and operating income given inventory levelsVivek SharanNo ratings yet

- Submitted by Nisar Ahmed Registration# 44150: Visic Corporation Cost of Goods Manufactured StatementDocument4 pagesSubmitted by Nisar Ahmed Registration# 44150: Visic Corporation Cost of Goods Manufactured StatementHaris KhanNo ratings yet

- Variable CostingDocument10 pagesVariable CostingShoaib HyderNo ratings yet

- Problem 2-14 Product Cost Sunk Cost Direct LaborDocument8 pagesProblem 2-14 Product Cost Sunk Cost Direct LaborarijitmajeeNo ratings yet

- Assignment: Table of ContentDocument9 pagesAssignment: Table of ContentAhsanur HossainNo ratings yet

- MANAC Pre MidDocument9 pagesMANAC Pre MidAbhay KaseraNo ratings yet

- Budgeting and Budgetary ControlDocument2 pagesBudgeting and Budgetary ControlpalkeeNo ratings yet

- Illustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesDocument4 pagesIllustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesGabriel BelmonteNo ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- CostingDocument46 pagesCostingRaghav KhakholiaNo ratings yet

- UTS AkutansiDocument24 pagesUTS AkutansiAbraham KristiyonoNo ratings yet

- Alpha, Beta, Gamma divisions budget and variance analysisDocument11 pagesAlpha, Beta, Gamma divisions budget and variance analysisRUPIKA R GNo ratings yet

- Day 4 (My)Document11 pagesDay 4 (My)Jhilmil JeswaniNo ratings yet

- 02 Tamiform Hilda Ngelah - Exercise 02 CostDocument7 pages02 Tamiform Hilda Ngelah - Exercise 02 Costrita tamohNo ratings yet

- DR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingDocument6 pagesDR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingSaumya JainNo ratings yet

- MAE RevisionDocument57 pagesMAE RevisionsaloniNo ratings yet

- Assignment PDFDocument15 pagesAssignment PDFpavanihirushaNo ratings yet

- Retain/drop A Segment E12-2Document6 pagesRetain/drop A Segment E12-2Khanh NgocNo ratings yet

- DAy 13 ClassDocument18 pagesDAy 13 ClassHardik MishraNo ratings yet

- Working Capital - Inventory & CASH MANAGEMENTDocument24 pagesWorking Capital - Inventory & CASH MANAGEMENTenicanNo ratings yet

- Job Costing & Contract Costing WorksheetDocument7 pagesJob Costing & Contract Costing Worksheetakash borseNo ratings yet

- Sales Budgeting (Dec 16)Document5 pagesSales Budgeting (Dec 16)Jaganath Reddy GFkKwVvllyNo ratings yet

- COST ANALYSIS OF BOJACK HORSEMAN CHARACTERSDocument4 pagesCOST ANALYSIS OF BOJACK HORSEMAN CHARACTERSFRANCIS GREGORY KUNo ratings yet

- Revision Class Notes 6 Jun 21Document7 pagesRevision Class Notes 6 Jun 21Rania barabaNo ratings yet

- Accounting For Production LossesDocument6 pagesAccounting For Production LossesMary Ann NatividadNo ratings yet

- BudgetDocument12 pagesBudgetmaxev92106No ratings yet

- Cost of Production StatementDocument1 pageCost of Production StatementDhruv Ratan DeyNo ratings yet

- Problem Set 1 PDFDocument3 pagesProblem Set 1 PDFrenjith0% (2)

- Sno Description Cost in Rs Cost in RsDocument8 pagesSno Description Cost in Rs Cost in RsCH NAIRNo ratings yet

- Chapter 4 ExerciseDocument7 pagesChapter 4 ExerciseJoe DicksonNo ratings yet

- Statement of Cost Analysis for Assignment 1Document3 pagesStatement of Cost Analysis for Assignment 1Pawanaps SrivastavaNo ratings yet

- Day 15 - CVP QuestionsDocument4 pagesDay 15 - CVP QuestionsRashmi Ranjan DashNo ratings yet

- Budgetary Control and Production Cost EstimationDocument15 pagesBudgetary Control and Production Cost EstimationAnimesh KalitaNo ratings yet

- Allison's Manufacturing BudgetsDocument12 pagesAllison's Manufacturing BudgetsjenieNo ratings yet

- ACCA F5 Class NotesDocument177 pagesACCA F5 Class NotesAzeezNo ratings yet

- 06 Tcheutsoua Marie Christelle Exercise 06Document6 pages06 Tcheutsoua Marie Christelle Exercise 06rita tamohNo ratings yet

- Calculating weighted average cost and change in fair value of biological assetsDocument7 pagesCalculating weighted average cost and change in fair value of biological assetsSinclair faith galarioNo ratings yet

- Cost SheetDocument4 pagesCost Sheetpravinmore1589No ratings yet

- Cost Analysis and Profitability ReportDocument3 pagesCost Analysis and Profitability ReportWEI QUAN LEENo ratings yet

- ABC - Process.Cost Allocation.Document21 pagesABC - Process.Cost Allocation.Keyt VintageNo ratings yet

- Excel Practise Questions and SolutionsDocument18 pagesExcel Practise Questions and SolutionsFahad NadeemNo ratings yet

- Reggie's BudgetDocument5 pagesReggie's BudgetYazan AdamNo ratings yet

- Cost Concepts - Cost SheetDocument24 pagesCost Concepts - Cost SheetFaraz SiddiquiNo ratings yet

- Costing Systems - Lessons ExamplesDocument15 pagesCosting Systems - Lessons ExamplesNicolasNo ratings yet

- Unit -4Document26 pagesUnit -4MOHAIDEEN THARIQ MNo ratings yet

- 03 Tadzoa Francis EXO 03 COSTDocument4 pages03 Tadzoa Francis EXO 03 COSTrita tamohNo ratings yet

- 1 Quantity Sold Per Month Unit Sales Price Total Revenue Per Month Changes in Total RevenueDocument15 pages1 Quantity Sold Per Month Unit Sales Price Total Revenue Per Month Changes in Total RevenueGillu BilluNo ratings yet

- (M-5) Budgeting 2Document26 pages(M-5) Budgeting 2Yolo GuyNo ratings yet

- Section - A: Question - 1Document10 pagesSection - A: Question - 1Sameen ShafaatNo ratings yet

- Manufacturing AccountsDocument2 pagesManufacturing AccountsMohamed IrshaNo ratings yet

- Tunku Puteri Intan Safinaz School of Accountancy Case StudyDocument26 pagesTunku Puteri Intan Safinaz School of Accountancy Case Studymohd reiNo ratings yet

- Classic Pen Solution Cost Allocation and DriversDocument1 pageClassic Pen Solution Cost Allocation and DriversTushar DuaNo ratings yet

- Acn 4Document3 pagesAcn 4Navidul IslamNo ratings yet

- Narsee Monjee Institute of Management Studies: Statistical Inference For Decision Making Bayes' Theorem and ApplicationsDocument4 pagesNarsee Monjee Institute of Management Studies: Statistical Inference For Decision Making Bayes' Theorem and ApplicationsSHIVANGI AGRAWALNo ratings yet

- Social Media Marketing Strategies for Shipping CompaniesDocument4 pagesSocial Media Marketing Strategies for Shipping CompaniesSHIVANGI AGRAWALNo ratings yet

- Hospital evaluates drug dosage and composition accuracyDocument7 pagesHospital evaluates drug dosage and composition accuracySHIVANGI AGRAWALNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument7 pagesNarsee Monjee Institute of Management StudiesSHIVANGI AGRAWALNo ratings yet

- The Supply Chain story of AmulDocument6 pagesThe Supply Chain story of AmulSHIVANGI AGRAWALNo ratings yet

- Master List of HR Interview Questions - GenmanDocument4 pagesMaster List of HR Interview Questions - GenmanSHIVANGI AGRAWALNo ratings yet

- P&G Process DetailsDocument3 pagesP&G Process DetailsSHIVANGI AGRAWALNo ratings yet

- P&G Interviews BtribeDocument10 pagesP&G Interviews BtribeSHIVANGI AGRAWALNo ratings yet

- P&G Process DetailsDocument3 pagesP&G Process DetailsSHIVANGI AGRAWALNo ratings yet

- P&G Interview QuestionsDocument3 pagesP&G Interview QuestionsSHIVANGI AGRAWALNo ratings yet

- DivF - Grp3 - Managing - Diversity - at - Spencer - Owens - SHIVANGI AGRAWALDocument3 pagesDivF - Grp3 - Managing - Diversity - at - Spencer - Owens - SHIVANGI AGRAWALSHIVANGI AGRAWALNo ratings yet

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Swati67% (3)

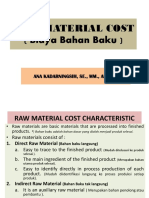

- Chapter 2 - Raw Material CostDocument29 pagesChapter 2 - Raw Material CostLia CollineNo ratings yet

- The Theory and Estimation of CostDocument38 pagesThe Theory and Estimation of Costde essensioNo ratings yet

- Introduction To Cost AccountingDocument30 pagesIntroduction To Cost AccountingParamjit Sharma100% (18)

- Jurnal Akuntansi Keuangan dan ManajemenDocument15 pagesJurnal Akuntansi Keuangan dan ManajemenR Indra S SipahutarNo ratings yet

- Exercise ManaccoDocument5 pagesExercise ManaccoGracelle Mae OrallerNo ratings yet

- Chapter 10--Profit and Cost Center Performance EvaluationDocument575 pagesChapter 10--Profit and Cost Center Performance EvaluationRobert AlexanderNo ratings yet

- Def 3Document48 pagesDef 3Alberto Miguel YuNo ratings yet

- MANACC Lesson 1 Introduction To Managerial Accounting Reviewer 1Document13 pagesMANACC Lesson 1 Introduction To Managerial Accounting Reviewer 1Rodolfo ManalacNo ratings yet

- Assignment Problems-Wk 4-Adnan-N0033642335Document8 pagesAssignment Problems-Wk 4-Adnan-N0033642335Mohammad AdnanNo ratings yet

- Understanding Cost Accounting ConceptsDocument8 pagesUnderstanding Cost Accounting ConceptsMeg sharkNo ratings yet

- Cost AccountingDocument12 pagesCost AccountingStephanie Mendoza0% (1)

- Solution Manual For John E. Freund's Mathematical Statistics With Applications 8/e MillerDocument9 pagesSolution Manual For John E. Freund's Mathematical Statistics With Applications 8/e MillerNehaNo ratings yet

- Chapter 5-Cost-Volume-Profit-Analysis.: Summer, 2011. Edited May 23, 2011Document98 pagesChapter 5-Cost-Volume-Profit-Analysis.: Summer, 2011. Edited May 23, 2011AlexElvirNo ratings yet

- CVP Tutorial SheetDocument4 pagesCVP Tutorial SheetDaneille Baker0% (1)

- Cost Behavior and Cost-Volume-Profit Analysis: Opening CommentsDocument16 pagesCost Behavior and Cost-Volume-Profit Analysis: Opening CommentsNnickyle LaboresNo ratings yet

- Illustrative-Problem-2 (Normal and Abnormal Losses)Document22 pagesIllustrative-Problem-2 (Normal and Abnormal Losses)rei biatchNo ratings yet

- Ubs Placement BrochureDocument48 pagesUbs Placement BrochureKaran DayrothNo ratings yet

- CH 7 Incremental AnalysisDocument42 pagesCH 7 Incremental AnalysisrusfazairaafNo ratings yet

- INVENTORY MANAGEMENT EOQ CALCULATIONS AND DISCOUNTSDocument17 pagesINVENTORY MANAGEMENT EOQ CALCULATIONS AND DISCOUNTSAb PiousNo ratings yet

- SCGMDocument2 pagesSCGMHassan IqbalNo ratings yet

- Ica Afm 2022Document64 pagesIca Afm 2022Muhammed FayisNo ratings yet

- Managerial Accounting SyllabusDocument5 pagesManagerial Accounting SyllabusGwendolyn Chloe PurnamaNo ratings yet

- Profile: Family CMADocument2 pagesProfile: Family CMAgrmani1981No ratings yet

- BCAS 14 ActivityDocument11 pagesBCAS 14 Activitymitu afrinNo ratings yet

- Cost Accounting: InstructionsDocument2 pagesCost Accounting: InstructionsSYED ALI SHAH SYED MUKHTIYAR ALINo ratings yet

- Reviewer in Cost Accounting (Midterm)Document11 pagesReviewer in Cost Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- Basic Concept FileDocument97 pagesBasic Concept FileArsalan AliNo ratings yet

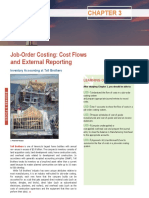

- Chapter 2 - Job Costing & ProcessDocument73 pagesChapter 2 - Job Costing & ProcessKimMmMmNo ratings yet

- 8508Document403 pages8508ilyas muhammad100% (1)