You might also like

- BioPharma Case StudyDocument4 pagesBioPharma Case StudyNaman Chhaya100% (3)

- Consumer Behaviour, 2nd Edition - Chapter 1Document42 pagesConsumer Behaviour, 2nd Edition - Chapter 1guptamadras100% (1)

- Pestle AustriaDocument1 pagePestle AustriaRananjay Singh100% (1)

- Hyper Launch BrochureDocument22 pagesHyper Launch BrochureQuintin McDonaldNo ratings yet

- Business Studies ProjectDocument37 pagesBusiness Studies Projectrishabhmah55% (31)

- Understanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassDocument24 pagesUnderstanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassCharlene KronstedtNo ratings yet

- presentation 4 2020-1Document42 pagespresentation 4 2020-1jimmy mlelwaNo ratings yet

- Unit 2: Forms of Commercial Organizations: Meaning, Features, Merits and Limitations of The Following FormsDocument35 pagesUnit 2: Forms of Commercial Organizations: Meaning, Features, Merits and Limitations of The Following FormsYashAgarwalNo ratings yet

- FirmDocument31 pagesFirmKiran MamadapurNo ratings yet

- Business OrganizationDocument26 pagesBusiness OrganizationAhmad NisarNo ratings yet

- Unit 2 Forms of BusinessDocument19 pagesUnit 2 Forms of Businessbrajdeep0% (1)

- Forms of Business OrganisationDocument42 pagesForms of Business OrganisationJohn NasasiraNo ratings yet

- 2. Types of Business OrganizationsDocument59 pages2. Types of Business Organizationsmohak vilechaNo ratings yet

- Forms of Business OrganisationDocument15 pagesForms of Business OrganisationPunit KumarNo ratings yet

- Business Structure and Organization: MeaningDocument17 pagesBusiness Structure and Organization: MeaningNavaneethakrishnan RangaswamyNo ratings yet

- Forms of Business OrganizationDocument46 pagesForms of Business OrganizationAmanjot SachdevaNo ratings yet

- Chap-1 Form of BusinessDocument12 pagesChap-1 Form of BusinessSunita BasakNo ratings yet

- Forms of Business Organisation ExplainedDocument36 pagesForms of Business Organisation ExplainedApril DaltonNo ratings yet

- Forms of Business Ownership and RegistrationDocument26 pagesForms of Business Ownership and Registrationchrissa padolinaNo ratings yet

- Forms of Business Organisations: Sole Proprietorship, Partnership, Joint Stock Companies and Co-operativesDocument49 pagesForms of Business Organisations: Sole Proprietorship, Partnership, Joint Stock Companies and Co-operativesJooooooooNo ratings yet

- Types of Business OrganizationsDocument35 pagesTypes of Business OrganizationsSIMRAN SHARMANo ratings yet

- Forms of Business: Sole Proprietorship and PartnershipDocument17 pagesForms of Business: Sole Proprietorship and PartnershipTavleen KaurNo ratings yet

- What Is Business?Document10 pagesWhat Is Business?Roshan GyawaliNo ratings yet

- Forms of Business UnitsDocument115 pagesForms of Business UnitsJaseme OtoyoNo ratings yet

- Principles of Management Module - 1 IntroductionDocument12 pagesPrinciples of Management Module - 1 Introductionnishutha3340No ratings yet

- Hand Out 8Document7 pagesHand Out 8abdool saheedNo ratings yet

- Entrepreneurship Unit 1 Understanding Businesses: DR Ella Kangaude-NkataDocument24 pagesEntrepreneurship Unit 1 Understanding Businesses: DR Ella Kangaude-NkataMartin ChikumbeniNo ratings yet

- Forms of Business OrganisationDocument9 pagesForms of Business OrganisationvmktptNo ratings yet

- Unit 3-Bom-GeDocument72 pagesUnit 3-Bom-GeGeet NarulaNo ratings yet

- Legal structures for operating a business in KenyaDocument8 pagesLegal structures for operating a business in KenyaMemory ApiyoNo ratings yet

- Starting a Business GuideDocument10 pagesStarting a Business GuiderohanNo ratings yet

- UntitledDocument22 pagesUntitledOwani JimmyNo ratings yet

- Forms of Business OrganisationDocument11 pagesForms of Business Organisationuche0% (1)

- Business Structure Types and Registration ProcessDocument22 pagesBusiness Structure Types and Registration ProcessDerrick Maatla MoadiNo ratings yet

- Essential business revision: entrepreneurs, resources, ownership formsDocument60 pagesEssential business revision: entrepreneurs, resources, ownership formsxalishaxpxNo ratings yet

- Unit 1: Introduction To Business and Economics 1. Business Organisation MeaningDocument16 pagesUnit 1: Introduction To Business and Economics 1. Business Organisation MeaningMohd YounusNo ratings yet

- BUSINESS STUDIES FORM TWO NOTES BY MRDocument83 pagesBUSINESS STUDIES FORM TWO NOTES BY MRPatroba WamalwaNo ratings yet

- Assess Feasibility New Venture Legal Forms BusinessDocument35 pagesAssess Feasibility New Venture Legal Forms BusinessDiriba GobenaNo ratings yet

- Week 1 Session 1: Form of Business OrganizationDocument32 pagesWeek 1 Session 1: Form of Business OrganizationMyla D. DimayugaNo ratings yet

- Session 7Document10 pagesSession 7kalu kioNo ratings yet

- Math 12-ABM Org - Mgt-Q1-Week-8Document20 pagesMath 12-ABM Org - Mgt-Q1-Week-8Nice D. ElseNo ratings yet

- Types of Business Enterprises ExplainedDocument16 pagesTypes of Business Enterprises ExplainedMinerva VSNo ratings yet

- BEFA Chapter 1Document31 pagesBEFA Chapter 1Tarun BoyaNo ratings yet

- Business EthicsDocument50 pagesBusiness EthicsAvegail Ocampo TorresNo ratings yet

- Forms of Business OrganisationDocument17 pagesForms of Business OrganisationZorman TaskyNo ratings yet

- Forms of BusinessDocument10 pagesForms of BusinessSeuwandi KeerthiratneNo ratings yet

- BAC1 Business OrganizationDocument28 pagesBAC1 Business OrganizationBryant Daniel Arguelles GacusNo ratings yet

- Sole Proprietorship: Ownership PatternsDocument7 pagesSole Proprietorship: Ownership PatternsDeepak SharmaNo ratings yet

- Forms of Business: Sole ProprietorshipDocument40 pagesForms of Business: Sole ProprietorshipNyx MetopeNo ratings yet

- Entrep 2Document28 pagesEntrep 2Sara SantiagoNo ratings yet

- Lesson 1 Origins and Roles of Business OrganizationDocument7 pagesLesson 1 Origins and Roles of Business Organizationerrorollllllllllll100% (1)

- Innovation As An Entrepreneur and Different Types of Enterprises and CompaniesDocument51 pagesInnovation As An Entrepreneur and Different Types of Enterprises and Companiespaulkhor74No ratings yet

- 4 Forms of Business OrganizationsDocument30 pages4 Forms of Business Organizationsapi-2670235120% (1)

- Success in Incorporating Small Businesses: (Twelve Cardinal Steps to Establish a Business in New York)From EverandSuccess in Incorporating Small Businesses: (Twelve Cardinal Steps to Establish a Business in New York)No ratings yet

- Chapter 2 Forms of BusinessDocument70 pagesChapter 2 Forms of Businessmanjushaa1618No ratings yet

- Lecture 9Document42 pagesLecture 9Trí NguyễnNo ratings yet

- Business Ethics Reviewer (1st Periodical)Document20 pagesBusiness Ethics Reviewer (1st Periodical)casumbalmckaylacharmianNo ratings yet

- BusinessDocument46 pagesBusinessAvishya JaswalNo ratings yet

- Mefa - Mech III - Civil - II - Unit-5Document10 pagesMefa - Mech III - Civil - II - Unit-5wasimrahmanwapsNo ratings yet

- Unit - 3 NDocument13 pagesUnit - 3 NSri BalajiNo ratings yet

- ME-Module-10-Organization-of-Firms StudentsDocument8 pagesME-Module-10-Organization-of-Firms StudentsAngelica PallarcaNo ratings yet

- Sole ProprietorshipDocument22 pagesSole ProprietorshipManish Mishra0% (1)

- Start Up LawDocument41 pagesStart Up LawMALKANI DISHA DEEPAKNo ratings yet

- Top Home-Based Business Ideas for 2020: 00 Proven Passive Income Ideas To Make Money with Your Home Based Business & Gain Financial FreedomFrom EverandTop Home-Based Business Ideas for 2020: 00 Proven Passive Income Ideas To Make Money with Your Home Based Business & Gain Financial FreedomNo ratings yet

- Home Based Business Ideas: Business Ideas You Can Do With Little Or No MoneyFrom EverandHome Based Business Ideas: Business Ideas You Can Do With Little Or No MoneyNo ratings yet

- Economics Complete (1)Document103 pagesEconomics Complete (1)JimmiNo ratings yet

- Economic Analysis- FundamentalsDocument21 pagesEconomic Analysis- FundamentalsJimmiNo ratings yet

- Economic Analysis- FundamentalsDocument21 pagesEconomic Analysis- FundamentalsJimmiNo ratings yet

- ProspectusDocument3 pagesProspectusJimmiNo ratings yet

- Moa & AoaDocument24 pagesMoa & AoaJimmiNo ratings yet

- Odoo Partnership Program EMEA AgendaDocument28 pagesOdoo Partnership Program EMEA AgendaEric Teo100% (2)

- TCPL Integrated Annual Report - FY2020-21Document288 pagesTCPL Integrated Annual Report - FY2020-21Mark LucasNo ratings yet

- Nike PresentationsDocument54 pagesNike PresentationsSubhan AhmedNo ratings yet

- DetailsNewCreditAssigned Mar23 OthersecuritiesDocument16 pagesDetailsNewCreditAssigned Mar23 OthersecuritiesasamitarannumNo ratings yet

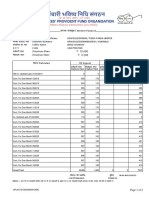

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Att-2.1 SowDocument5 pagesAtt-2.1 SowAgung FitrillaNo ratings yet

- Quotation - Householders - LAPSONDocument1 pageQuotation - Householders - LAPSONCredsureNo ratings yet

- MBA and MSC RESEARCH PROPOSALDocument19 pagesMBA and MSC RESEARCH PROPOSALmuthomi.bookshop.storeNo ratings yet

- NIC Asia Bank Brand PositioningDocument29 pagesNIC Asia Bank Brand PositioningRaushan ChaudharyNo ratings yet

- Introduction & CreationDocument34 pagesIntroduction & CreationirfafNo ratings yet

- Nabanita Das - Senior Integration (Software AG Webmethods) Consultant 03242023Document12 pagesNabanita Das - Senior Integration (Software AG Webmethods) Consultant 03242023vipul tiwariNo ratings yet

- Cost Accounting: Level 3Document19 pagesCost Accounting: Level 3Hein Linn Kyaw100% (1)

- C&I JSA 09 GeneralDocument1 pageC&I JSA 09 Generalamit kumarNo ratings yet

- What Does ATEX Mean?: Quality - Reliability - EfficiencyDocument4 pagesWhat Does ATEX Mean?: Quality - Reliability - EfficiencyNayyar SkNo ratings yet

- 30 Free Leed Ap BD+C Sample QuestionsDocument23 pages30 Free Leed Ap BD+C Sample QuestionsSubhranshu PandaNo ratings yet

- ES 301 Assignment #1 engineering economy problems and solutionsDocument2 pagesES 301 Assignment #1 engineering economy problems and solutionsErika Rez LapatisNo ratings yet

- Jollisavers Meals TV Ad DeconstructedDocument4 pagesJollisavers Meals TV Ad DeconstructedMa. Rhona Faye MedesNo ratings yet

- Chapter 4 MCQsDocument3 pagesChapter 4 MCQsprince ahenkoraNo ratings yet

- Business 5511 Group Project 0007ADocument15 pagesBusiness 5511 Group Project 0007ALinh NguyenNo ratings yet

- Sas#20 Bam242Document9 pagesSas#20 Bam242Everly Mae ElondoNo ratings yet

- New Invt MGT KesoramDocument69 pagesNew Invt MGT Kesoramtulasinad123No ratings yet

- Financial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceDocument72 pagesFinancial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceRod SisonNo ratings yet

- Marcopper Mining CorpDocument7 pagesMarcopper Mining CorpChristine Ivy Delos SantosNo ratings yet

- 3-in-1 Stylus Business PlanDocument24 pages3-in-1 Stylus Business Planalliahdane valenciaNo ratings yet

- Evaluation of Proposals For BOT ProjectsDocument6 pagesEvaluation of Proposals For BOT ProjectsTjandra LiemNo ratings yet