You might also like

- Class 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIDocument70 pagesClass 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIPathan KausarNo ratings yet

- Financial statements analysisDocument3 pagesFinancial statements analysisFEBRI IRAWANNo ratings yet

- Financial Statements AdjustmentsDocument65 pagesFinancial Statements AdjustmentsBhartiNo ratings yet

- Diagnostic Quiz On Accounting 2Document9 pagesDiagnostic Quiz On Accounting 2Anne Ford67% (3)

- Financial Statements 2Document65 pagesFinancial Statements 2srisrirockstarNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- 1st Assignment - 2023Document15 pages1st Assignment - 2023harmanchahalNo ratings yet

- Financial StatementsDocument65 pagesFinancial StatementsApollo Institute of Hospital AdministrationNo ratings yet

- Journal and Ledger With List of Accounts PDFDocument2 pagesJournal and Ledger With List of Accounts PDFJen RossNo ratings yet

- Unit 3 AdjustmentsDocument8 pagesUnit 3 Adjustmentsdilipkumar.1267No ratings yet

- TASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraDocument4 pagesTASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraSincy MathewNo ratings yet

- Chapter 1-Problem 1 To 5: Charles Company Balance Sheet As On 31st Dec AssetsDocument9 pagesChapter 1-Problem 1 To 5: Charles Company Balance Sheet As On 31st Dec AssetsSimran HarchandaniNo ratings yet

- Acct 2301 Spring 2010 TestDocument6 pagesAcct 2301 Spring 2010 Testamittutorials1985No ratings yet

- Basic Accounting EquationsDocument26 pagesBasic Accounting EquationsPradeep GuptaNo ratings yet

- Running a Small BusinessDocument20 pagesRunning a Small BusinessJenecil JavierNo ratings yet

- PRACTICE-SET-IN-BASIC-ACCOUNTING-converted (Repaired)Document33 pagesPRACTICE-SET-IN-BASIC-ACCOUNTING-converted (Repaired)mary josefaNo ratings yet

- Accounting Tutorials Day 1Document8 pagesAccounting Tutorials Day 1Richboy Jude VillenaNo ratings yet

- Lecture No. 2 - Financial Statements & Illustrative ProblemDocument6 pagesLecture No. 2 - Financial Statements & Illustrative ProblemJA LAYUG100% (1)

- SET 1. Q.1 Explain Any Two Accounting Concepts With Example? AnsDocument9 pagesSET 1. Q.1 Explain Any Two Accounting Concepts With Example? AnsmuravbookNo ratings yet

- Dream Guitar Shop Financial ProjectionsDocument3 pagesDream Guitar Shop Financial ProjectionsJennilyn SolimanNo ratings yet

- Lecture No 2Document4 pagesLecture No 2Avia Chelsy DeangNo ratings yet

- Financial Accounting & AnalysisDocument2 pagesFinancial Accounting & AnalysisTangerine Ila TomarNo ratings yet

- Lecture 2Document23 pagesLecture 2Dalia SamirNo ratings yet

- Accounting 2 - Unit 3 - Lesson 1 To 3Document62 pagesAccounting 2 - Unit 3 - Lesson 1 To 3Merdwindelle AllagonesNo ratings yet

- Corporate Liquidation Problem SetDocument7 pagesCorporate Liquidation Problem SetMary Rose ArguellesNo ratings yet

- Only Chosen Records Are Maintained, Some Transaction Are Recorded in Narrative FormDocument3 pagesOnly Chosen Records Are Maintained, Some Transaction Are Recorded in Narrative FormmarinNo ratings yet

- Acct615 NjitDocument24 pagesAcct615 NjithjnNo ratings yet

- Financial Prep EntrepreneursDocument66 pagesFinancial Prep EntrepreneursRAHKAESH NAIR A L UTHAIYA NAIR100% (1)

- Accounting AssignmentDocument16 pagesAccounting AssignmentAarya SharmaNo ratings yet

- Statement of Cash Flows ExplainedDocument6 pagesStatement of Cash Flows ExplainedJmaseNo ratings yet

- Philippine high school student's accounting worksheetDocument7 pagesPhilippine high school student's accounting worksheetCha Eun WooNo ratings yet

- FABM 1 Lesson 7 The Accounting EquationDocument19 pagesFABM 1 Lesson 7 The Accounting EquationTiffany Ceniza100% (1)

- Acctg 111 Assign3 ReviewerDocument5 pagesAcctg 111 Assign3 ReviewerChris Jay LatibanNo ratings yet

- Week 2-1 SlidesDocument30 pagesWeek 2-1 SlidesLIAW ANN YINo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- ACCT1111 Chapter 2 LectureDocument61 pagesACCT1111 Chapter 2 LectureWky Jim100% (1)

- Session 1 Practice 3Document4 pagesSession 1 Practice 3yimin liuNo ratings yet

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaNo ratings yet

- Financial Accounting by PmtycoonDocument56 pagesFinancial Accounting by PmtycoonsachinNo ratings yet

- Liquidation of CorporationDocument15 pagesLiquidation of CorporationMacie MenesesNo ratings yet

- MB0025 Financial and Management AccountingDocument7 pagesMB0025 Financial and Management Accountingvarsha100% (1)

- Acc 111Document10 pagesAcc 111adrian CharlesNo ratings yet

- Venture Valuation MethodsDocument2 pagesVenture Valuation MethodsEmily HackNo ratings yet

- TEML10ACTIVITY 38 2nd CDocument3 pagesTEML10ACTIVITY 38 2nd CJennilyn SolimanNo ratings yet

- 1 Accounting Equation UniqueDocument3 pages1 Accounting Equation UniqueSohan AgrawalNo ratings yet

- Accounting Principles 10th Edition Weygandt & Kimmel Chapter 1Document40 pagesAccounting Principles 10th Edition Weygandt & Kimmel Chapter 1ZisanNo ratings yet

- Lesson 4: Analyzing TransactionsDocument3 pagesLesson 4: Analyzing TransactionsDante SausaNo ratings yet

- Lesson 4 Week 5 FABM 2Document21 pagesLesson 4 Week 5 FABM 2Mikel Nelson AmpoNo ratings yet

- L03 - Accounting Classification and EquationsDocument29 pagesL03 - Accounting Classification and EquationsmardhiahNo ratings yet

- As 22.deffered - TaxDocument7 pagesAs 22.deffered - TaxabrastogiNo ratings yet

- Unit - 1 Accounting Equations & Journal & Ledger & TBDocument43 pagesUnit - 1 Accounting Equations & Journal & Ledger & TBShreyash PardeshiNo ratings yet

- Fabm SG 11 Q3 0903Document32 pagesFabm SG 11 Q3 0903James Kirby CuervoNo ratings yet

- Chap 3 Accounting Classification & Equation (Basic+Expended) - ClassDocument37 pagesChap 3 Accounting Classification & Equation (Basic+Expended) - Classnabkill100% (1)

- Working Paper-Chapters 1-4 Naser AbdelkarimDocument5 pagesWorking Paper-Chapters 1-4 Naser AbdelkarimHasan NajiNo ratings yet

- Unit 3 - Trial BalanceDocument11 pagesUnit 3 - Trial Balancegogo chanNo ratings yet

- Journal EntryDocument15 pagesJournal EntryNajOh Marie D ENo ratings yet

- ACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationDocument34 pagesACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationAbu AhmedNo ratings yet

- Unit - II Module IIIDocument7 pagesUnit - II Module IIIpltNo ratings yet

- Eco 3Document1 pageEco 3NISHANTH P CHOYAL 2228512No ratings yet

- Eco 1Document1 pageEco 1NISHANTH P CHOYAL 2228512No ratings yet

- EconomicsDocument1 pageEconomicsNISHANTH P CHOYAL 2228512No ratings yet

- Eco 2Document1 pageEco 2NISHANTH P CHOYAL 2228512No ratings yet

- Concepts of AccountingDocument1 pageConcepts of AccountingNISHANTH P CHOYAL 2228512No ratings yet

- Concepts of FinanceDocument1 pageConcepts of FinanceNISHANTH P CHOYAL 2228512No ratings yet

- (A) To Present A True: The BDocument1 page(A) To Present A True: The BNISHANTH P CHOYAL 2228512No ratings yet

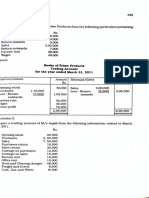

- Books of Prime Products Account For The Year Ended March 31, 2011 CRDocument1 pageBooks of Prime Products Account For The Year Ended March 31, 2011 CRNISHANTH P CHOYAL 2228512No ratings yet

- Name PlateDocument13 pagesName PlateNISHANTH P CHOYAL 2228512No ratings yet

- 11 Working Capital ManagementDocument34 pages11 Working Capital Managementaashulheda100% (1)

- Theme 5 Management Science and Financial Management Course GuideDocument48 pagesTheme 5 Management Science and Financial Management Course Guidedanielnebeyat7No ratings yet

- Assumption College Final Exam ReviewDocument7 pagesAssumption College Final Exam ReviewJudithaNo ratings yet

- 6 Pas 23 28 PDFDocument1 page6 Pas 23 28 PDFcherry blossomNo ratings yet

- FM1 ActivityDocument4 pagesFM1 ActivityChieMae Benson Quinto100% (1)

- Project Report On Starting A New Business.... (Comfort Jeans)Document30 pagesProject Report On Starting A New Business.... (Comfort Jeans)lalitsingh76% (72)

- Chapter 1-Fundamentals of Financial AccountingDocument20 pagesChapter 1-Fundamentals of Financial AccountingAudrey ReyesNo ratings yet

- Chapter 1 With Quick CheckDocument48 pagesChapter 1 With Quick CheckSigit AryantoNo ratings yet

- 9706 m17 Ms 22Document11 pages9706 m17 Ms 22FarrukhsgNo ratings yet

- MYOB Accounting GlossaryDocument14 pagesMYOB Accounting GlossarySyirleen Adlyna OthmanNo ratings yet

- Sol Q5Document5 pagesSol Q5Elle VernezNo ratings yet

- REPORT ON BINGO INDUSTRIES' STRATEGIES AND PERFORMANCEDocument8 pagesREPORT ON BINGO INDUSTRIES' STRATEGIES AND PERFORMANCERaghav Rawat 2027407No ratings yet

- Advanced Financial Accounting 6th Edition Beechy Test BankDocument38 pagesAdvanced Financial Accounting 6th Edition Beechy Test Bankpottpotlacew8mf1t100% (15)

- Balance Sheet: As at 31st March, 2019Document2 pagesBalance Sheet: As at 31st March, 2019Mandeep BatraNo ratings yet

- Corporate Governance and Firm Performance in Emerging MarketsDocument40 pagesCorporate Governance and Firm Performance in Emerging MarketsThương PhạmNo ratings yet

- Gulf Air Co-Phil Branch v. CIRDocument3 pagesGulf Air Co-Phil Branch v. CIRJustine GaverzaNo ratings yet

- Economic Value Added Momentum TraditionalprofitabilitymeasuresDocument14 pagesEconomic Value Added Momentum TraditionalprofitabilitymeasuresWilliamCNo ratings yet

- Stone Container CorporationDocument11 pagesStone Container CorporationMeena100% (3)

- Investment Vs SavingsDocument2 pagesInvestment Vs Savingsgaurav dedhiaNo ratings yet

- Share Accounting-WPS OfficeDocument5 pagesShare Accounting-WPS OfficeSurendra SharmaNo ratings yet

- Grantmakers in the Arts National Capitalization Project Literature ReviewDocument19 pagesGrantmakers in the Arts National Capitalization Project Literature ReviewRoel SisonNo ratings yet

- Professional Ethics - , Accountancy For Lawyers and Bench-BarDocument27 pagesProfessional Ethics - , Accountancy For Lawyers and Bench-BarArpan Kamal100% (6)

- Financial Analysis Case StudyDocument14 pagesFinancial Analysis Case StudyPratik Prakash BhosaleNo ratings yet

- Dividend Decisions SolutionsDocument13 pagesDividend Decisions SolutionsHarsha VardhanNo ratings yet

- PT Zamklik Closing Journal Entry December 2022 (In Rupiah)Document1 pagePT Zamklik Closing Journal Entry December 2022 (In Rupiah)ahmadiNo ratings yet

- Cost Accounting: The Institute of Chartered Accountants of PakistanDocument4 pagesCost Accounting: The Institute of Chartered Accountants of PakistanShehrozSTNo ratings yet

- Types of Tenders ExplainedDocument7 pagesTypes of Tenders ExplainedajithNo ratings yet

- MBA Accounting 4 Managers MSTDocument2 pagesMBA Accounting 4 Managers MSTrichadinrajNo ratings yet

- Topic 5 - Single-Entry MethodDocument49 pagesTopic 5 - Single-Entry MethodMary Yvonne AresNo ratings yet

- On January 1 2018 The General Ledger of Dynamite FireworksDocument2 pagesOn January 1 2018 The General Ledger of Dynamite FireworksAmit PandeyNo ratings yet