You might also like

- Direction: Read and Select The Best Answer For The Following QuestionsDocument40 pagesDirection: Read and Select The Best Answer For The Following QuestionsDennis VelasquezNo ratings yet

- Ia2 Examination 1 Theories Liabilities and Provisions - CompressDocument3 pagesIa2 Examination 1 Theories Liabilities and Provisions - CompressTRECIA AMOR PAMILARNo ratings yet

- Reviewer in Theory of Accounts Multiple ChoiceDocument17 pagesReviewer in Theory of Accounts Multiple ChoiceDaniella Mae ElipNo ratings yet

- ToA Quizzer 10 - Provisions, ContingenciesDocument4 pagesToA Quizzer 10 - Provisions, ContingenciesEuniceChung0% (1)

- Liability FinalDocument26 pagesLiability FinalJomarie UyNo ratings yet

- 9 - Liabilities Theory of Accounts 9 - Liabilities Theory of AccountsDocument8 pages9 - Liabilities Theory of Accounts 9 - Liabilities Theory of AccountsandreamrieNo ratings yet

- Liability Accounting Quiz: Key Terms like Accrual, Provision, Contingent LiabilitiesDocument7 pagesLiability Accounting Quiz: Key Terms like Accrual, Provision, Contingent LiabilitiesJheally SeirNo ratings yet

- B. A Liability of Uncertain Timing or AmountDocument15 pagesB. A Liability of Uncertain Timing or Amountcherry blossomNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- IntAcc 1 Reviewer - Module 2 (Theories)Document8 pagesIntAcc 1 Reviewer - Module 2 (Theories)Lizette Janiya SumantingNo ratings yet

- TheoriesDocument28 pagesTheoriesYou Knock On My DoorNo ratings yet

- Current LiabDocument24 pagesCurrent LiabSamantha Marie ArevaloNo ratings yet

- Current Liabilities Provisions and Contingencies TheoriesDocument12 pagesCurrent Liabilities Provisions and Contingencies TheoriesKristine Trisha Anne SabornidoNo ratings yet

- Mock ExamDocument22 pagesMock ExamAlyana DubloisNo ratings yet

- Ias 37Document2 pagesIas 37Bilal GhuneimNo ratings yet

- LiabilitiesDocument6 pagesLiabilitiesJi YuNo ratings yet

- Current LiabilitiesDocument3 pagesCurrent LiabilitiesKoko LaineNo ratings yet

- Types of LiabilitiesDocument11 pagesTypes of LiabilitiesJayson Manalo GañaNo ratings yet

- Quiz in Fin Man AssetsDocument7 pagesQuiz in Fin Man AssetsCherseaLizetteRoyPicaNo ratings yet

- Acctg 3b Midterm ExamDocument10 pagesAcctg 3b Midterm ExamDonalyn BannagaoNo ratings yet

- Pairamid Part 1Document75 pagesPairamid Part 1Peterpaul SilacanNo ratings yet

- Test Bank Reviewer Part 2Document4 pagesTest Bank Reviewer Part 2tres gian de guzmanNo ratings yet

- Audit Prob Part 2Document6 pagesAudit Prob Part 2Koko LaineNo ratings yet

- Intacc Reviewer Quiz #1Document39 pagesIntacc Reviewer Quiz #1UNKNOWNN0% (1)

- Accounting Quiz with 31 Multiple Choice QuestionsDocument9 pagesAccounting Quiz with 31 Multiple Choice Questionsmarites yuNo ratings yet

- MCQ-Conceptual LiabilitiesDocument25 pagesMCQ-Conceptual LiabilitiesKrishele G. GotejerNo ratings yet

- Financial Accounting and Reporting: Multiple ChoiceDocument54 pagesFinancial Accounting and Reporting: Multiple ChoiceLouiseNo ratings yet

- Acctexam - Current Liabilities and ContingenciesDocument7 pagesAcctexam - Current Liabilities and ContingenciesAsheNo ratings yet

- 7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent AssetsDocument6 pages7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent Assetsjsmozol3434qcNo ratings yet

- Theories Conceptual Framework and Accouting Standards Answer KeyDocument7 pagesTheories Conceptual Framework and Accouting Standards Answer KeyEl AgricheNo ratings yet

- Chapter 13Document38 pagesChapter 13Kimmy ShawwyNo ratings yet

- Shareholders Equity PDF FreeDocument111 pagesShareholders Equity PDF FreeJoseph Asis100% (1)

- Ldersgate Ollege Ourse Udit Chool OF Usiness AND Ccountancy Odule IabilitiesDocument4 pagesLdersgate Ollege Ourse Udit Chool OF Usiness AND Ccountancy Odule Iabilitiescha11No ratings yet

- Receivables Theory Explained in 30 QuestionsDocument6 pagesReceivables Theory Explained in 30 QuestionsandreamrieNo ratings yet

- Mountain View College Intermediate Accounting 2 Exam Multiple Choice QuestionsDocument8 pagesMountain View College Intermediate Accounting 2 Exam Multiple Choice QuestionsHardly Dare GonzalesNo ratings yet

- Statement of Financial PositionDocument7 pagesStatement of Financial PositionshengNo ratings yet

- Cash and Cash Equivalents, Accounts Receivable, Bad DebtsDocument5 pagesCash and Cash Equivalents, Accounts Receivable, Bad DebtsDennis VelasquezNo ratings yet

- 6840 - PAS 37 Provisions Contingent Liabilities and Contingent AssetsDocument6 pages6840 - PAS 37 Provisions Contingent Liabilities and Contingent AssetsAhmad Noainy AntapNo ratings yet

- Select The Best Answer From The Choices Given.: TheoryDocument14 pagesSelect The Best Answer From The Choices Given.: TheoryROMAR A. PIGANo ratings yet

- Reviewer 1 - 6 Intacc 2Document58 pagesReviewer 1 - 6 Intacc 2Ivory ClaudioNo ratings yet

- Post Test AK2Document51 pagesPost Test AK2thalita najellaNo ratings yet

- Quizzer #10 LiabilitiesDocument19 pagesQuizzer #10 LiabilitiesKimmy ShawwyNo ratings yet

- Exam ReviewerDocument10 pagesExam Reviewerjoseph christopher vicenteNo ratings yet

- Ia 2 - ReviewerDocument3 pagesIa 2 - ReviewerCenelyn PajarillaNo ratings yet

- Final Exam CDocument12 pagesFinal Exam Cnhorelajne03No ratings yet

- Chapter 13 intermediate accounting liabilitiesDocument8 pagesChapter 13 intermediate accounting liabilitiesMarlind3No ratings yet

- To Print 1Document15 pagesTo Print 1Scrunchies AvenueNo ratings yet

- Auditing MiscDocument11 pagesAuditing MiscLlyod Francis LaylayNo ratings yet

- Chapter 2 NOTES PAYABLE SUMMARY & PROBLEMSDocument12 pagesChapter 2 NOTES PAYABLE SUMMARY & PROBLEMSellyzamae quiraoNo ratings yet

- Current AssetsDocument53 pagesCurrent AssetsIris Mnemosyne100% (1)

- QuizDocument32 pagesQuizEloisaNo ratings yet

- Intermediate Accouting Testbank ch13Document23 pagesIntermediate Accouting Testbank ch13cthunder_192% (12)

- Accounting of ReceivablesDocument4 pagesAccounting of Receivableshellohello50% (2)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Direction: Read and Select The Best Answer For The Following QuestionsDocument5 pagesDirection: Read and Select The Best Answer For The Following QuestionsRenz Francis LimNo ratings yet

- IAS 37 - SummaryDocument4 pagesIAS 37 - SummaryRenz Francis LimNo ratings yet

- Notes in Research and Development CostsDocument1 pageNotes in Research and Development CostsRenz Francis LimNo ratings yet

- Handout - Impairment of Assets - SCDocument10 pagesHandout - Impairment of Assets - SCRenz Francis LimNo ratings yet

- Classifications of LiabilitiesDocument1 pageClassifications of LiabilitiesRenz Francis LimNo ratings yet

- Alert Company S Shareholders Equity Prior To Any of The Following PDFDocument1 pageAlert Company S Shareholders Equity Prior To Any of The Following PDFHassan JanNo ratings yet

- Role of Tech in Promoting Financial InclusionDocument66 pagesRole of Tech in Promoting Financial InclusionKheang VesalNo ratings yet

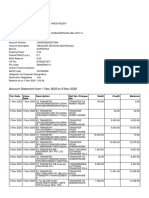

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyNo ratings yet

- Sec 41-45 Corporation CodeDocument9 pagesSec 41-45 Corporation CodeCarlMarkInopia100% (1)

- S6-10 Digital Lending - Lending Club and AffirmDocument22 pagesS6-10 Digital Lending - Lending Club and AffirmVivek SinghNo ratings yet

- Room Credit Hour Class Time Days Course Name Sectio N Course IdDocument2 pagesRoom Credit Hour Class Time Days Course Name Sectio N Course IdImran KhanNo ratings yet

- Chapter 3 - Accounting PrinciplesDocument23 pagesChapter 3 - Accounting PrinciplesVivek GargNo ratings yet

- IGCSE IGCSE Cambridge Accounting (0452) MS For ClassifiedDocument492 pagesIGCSE IGCSE Cambridge Accounting (0452) MS For ClassifiedBraha BabikerNo ratings yet

- House No. 123-A,, Street No. 12, Lane # 4, Chaklala Scheme 3, Rawalpindi, Cantonement. Adnan AhmedDocument4 pagesHouse No. 123-A,, Street No. 12, Lane # 4, Chaklala Scheme 3, Rawalpindi, Cantonement. Adnan AhmedAdnan AfridiNo ratings yet

- Iqmethod ValuationDocument48 pagesIqmethod ValuationAkash VaidNo ratings yet

- P 50Document2 pagesP 50Emily DeerNo ratings yet

- Accounting for Business Combinations and Internal ReconstructionsDocument27 pagesAccounting for Business Combinations and Internal ReconstructionsbinuNo ratings yet

- Ricardo Vargas Roi Pmo Slides enDocument61 pagesRicardo Vargas Roi Pmo Slides ensNo ratings yet

- BPI V SECDocument2 pagesBPI V SECArellano AureNo ratings yet

- 2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Document4 pages2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Rainy GoodwillNo ratings yet

- ESG Handbook - FCA UKDocument20 pagesESG Handbook - FCA UKEmdad YusufNo ratings yet

- CÂU HỎI TRẮC NGHIỆM CHƯƠNG 5 PPPIFE 1Document5 pagesCÂU HỎI TRẮC NGHIỆM CHƯƠNG 5 PPPIFE 1Nhi PhanNo ratings yet

- Brockhaus-Long ApproximationDocument8 pagesBrockhaus-Long Approximationmainak.chatterjee03No ratings yet

- Banking Regulation Act 1949Document13 pagesBanking Regulation Act 1949jhumli0% (1)

- Chapter 2Document2 pagesChapter 211.15. Hoàng Nguyễn Thanh HươngNo ratings yet

- Frank Peters Show - ReviewDocument12 pagesFrank Peters Show - ReviewitalianangelsNo ratings yet

- SBI Education Loan for IMI New Delhi StudentsDocument2 pagesSBI Education Loan for IMI New Delhi StudentsRahulJotwaniNo ratings yet

- Vulture CapitalistDocument2 pagesVulture Capitalistjosh321No ratings yet

- Multiple Choice Assessment QuestionsDocument7 pagesMultiple Choice Assessment QuestionsLaiven RyleNo ratings yet

- Forex StrategyDocument11 pagesForex StrategyNoman Khan100% (1)

- Fixed Income - AnswersDocument6 pagesFixed Income - AnswersNeerajNo ratings yet

- Annuity (PMT)Document54 pagesAnnuity (PMT)bayu fajarNo ratings yet

- Bank Management Financial Services Rose 9th Edition Solutions ManualDocument18 pagesBank Management Financial Services Rose 9th Edition Solutions ManualJamesWolfefsgr100% (38)

- The Global Capitalist Crisis:: Its Origins, Nature and ImpactDocument45 pagesThe Global Capitalist Crisis:: Its Origins, Nature and Impactanmol149No ratings yet

- Essay On InflationDocument2 pagesEssay On InflationAlyani Korner100% (5)