You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- SP-Notes Q3-W2 (Note#3)Document4 pagesSP-Notes Q3-W2 (Note#3)Paulo Amposta CarpioNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Note #10: Sampling Distribution of The Sample MeanDocument2 pagesNote #10: Sampling Distribution of The Sample MeanPaulo Amposta CarpioNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Carpio - PauloMiguel - Worksheet 6Document2 pagesCarpio - PauloMiguel - Worksheet 6Paulo Amposta CarpioNo ratings yet

- Teacher Induction Program (TIP) : Core CourseDocument121 pagesTeacher Induction Program (TIP) : Core CoursePaulo Amposta CarpioNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Cxa For Froilan Pi-It BalistoyDocument2 pagesCxa For Froilan Pi-It BalistoyPaulo Amposta CarpioNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- SP-Q3 Note#7 Area Under Normal CurveDocument4 pagesSP-Q3 Note#7 Area Under Normal CurvePaulo Amposta CarpioNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Ok ECRA G12 Bandura CPAR OLOROCISIMO 1stsem - SY2022 2023 U10.16Document2 pagesOk ECRA G12 Bandura CPAR OLOROCISIMO 1stsem - SY2022 2023 U10.16Paulo Amposta CarpioNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Q3 W2 TemplateDocument1 pageQ3 W2 TemplatePaulo Amposta CarpioNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- SP-Q3 Note#5 Normal Random VariableDocument2 pagesSP-Q3 Note#5 Normal Random VariablePaulo Amposta CarpioNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Q3 Week 1 TemplateDocument2 pagesQ3 Week 1 TemplatePaulo Amposta CarpioNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Etech WK2Document3 pagesEtech WK2Paulo Amposta CarpioNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Teacher Induction Program (TIP) : CourseDocument104 pagesTeacher Induction Program (TIP) : CoursePaulo Amposta CarpioNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Teacher Induction Program (TIP) : Core CourseDocument94 pagesTeacher Induction Program (TIP) : Core CoursePaulo Amposta CarpioNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Teacher Induction Program (TIP) : Core CourseDocument74 pagesTeacher Induction Program (TIP) : Core CoursePaulo Amposta CarpioNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Etech WK4Document4 pagesEtech WK4Paulo Amposta CarpioNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- St. Edward School SHS Daily Check-In / Homeroom Guidance Program 2nd Semester, SY 2021-2022Document8 pagesSt. Edward School SHS Daily Check-In / Homeroom Guidance Program 2nd Semester, SY 2021-2022Paulo Amposta CarpioNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- 11 Third Quarter: Learning Area Grade Level Quarter Date I. Lesson Title Ii. Most Essential Learning Competencies (Melcs)Document4 pages11 Third Quarter: Learning Area Grade Level Quarter Date I. Lesson Title Ii. Most Essential Learning Competencies (Melcs)Paulo Amposta CarpioNo ratings yet

- Etech WK1Document3 pagesEtech WK1Paulo Amposta CarpioNo ratings yet

- Q4-ABM-Organization and Management-11-Week-3Document4 pagesQ4-ABM-Organization and Management-11-Week-3Paulo Amposta CarpioNo ratings yet

- Accounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesAccounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesFundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- GPGSHS Psychosocial Support ActivityDocument46 pagesGPGSHS Psychosocial Support ActivityPaulo Amposta CarpioNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesFundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Republic of The Philippines Department of Education: Gen. Pantaleon Garcia Senior High SchoolDocument6 pagesRepublic of The Philippines Department of Education: Gen. Pantaleon Garcia Senior High SchoolPaulo Amposta CarpioNo ratings yet

- Q4-ABM-Organization and Management-11-Week-2Document3 pagesQ4-ABM-Organization and Management-11-Week-2Paulo Amposta CarpioNo ratings yet

- Aava Mineral Water Case - Presentation - Group A2 - 24 Jul 20 PDFDocument9 pagesAava Mineral Water Case - Presentation - Group A2 - 24 Jul 20 PDFSaagar ChitkaraNo ratings yet

- Business Economics I 4Document121 pagesBusiness Economics I 4GrenvilNo ratings yet

- Executive Summery: Basic Idea and Project BackgroundDocument16 pagesExecutive Summery: Basic Idea and Project BackgroundHermela tedla100% (2)

- Entrepreunrship: 4 Grading EntrepDocument5 pagesEntrepreunrship: 4 Grading EntrepJustin VelezNo ratings yet

- Case Study On Miracle-Mind CompanyDocument16 pagesCase Study On Miracle-Mind CompanyVishalNo ratings yet

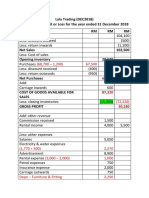

- Lala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTDocument3 pagesLala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTAFIQ RAFIQIN RAHMADNo ratings yet

- GST 9th Edition BookDocument542 pagesGST 9th Edition BookLalli DeviNo ratings yet

- BottleneckDocument5 pagesBottleneckcpl_09No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sony Marketing MixDocument3 pagesSony Marketing MixSaith UmairNo ratings yet

- IPO-Individual Purchase Orders in SAP MM & SDDocument9 pagesIPO-Individual Purchase Orders in SAP MM & SDPooja Pandey67% (3)

- JETIR1808315Document18 pagesJETIR1808315PriyanshNo ratings yet

- 4 The Sale of Goods Act, 1930Document8 pages4 The Sale of Goods Act, 1930Sudheer VishwakarmaNo ratings yet

- Buy Delta 8 THC Bulk @Delta8.ScienceDocument10 pagesBuy Delta 8 THC Bulk @Delta8.ScienceDelta 8 ScienceNo ratings yet

- Business Advantage Advanced Unit3 Making A Sales Pitch Video PDFDocument6 pagesBusiness Advantage Advanced Unit3 Making A Sales Pitch Video PDFHiếu Nguyễn MinhNo ratings yet

- Kim ReportingManAccDocument5 pagesKim ReportingManAccKimberly Kaye Olarte FranciscoNo ratings yet

- Financial Ratios Analysis of NestleDocument18 pagesFinancial Ratios Analysis of NestleNur WahidaNo ratings yet

- BATADocument31 pagesBATATHINGS GO VIRALNo ratings yet

- UPS Full ProofDocument1 pageUPS Full Proofyotel52289No ratings yet

- Pricing Products: Pricing StrategiesDocument50 pagesPricing Products: Pricing StrategiesShifa ChishtiNo ratings yet

- Designing Distribution Networks & Applications To E-BusinessDocument32 pagesDesigning Distribution Networks & Applications To E-BusinessJoann TeyNo ratings yet

- Iventory Management Control System in Coca ColaDocument45 pagesIventory Management Control System in Coca ColaMAHESH MUTHYALANo ratings yet

- Acc 106 p3 Exam Set ADocument14 pagesAcc 106 p3 Exam Set ALexzy Chant LopezNo ratings yet

- Raw Material Consumed Rs 15,000 Direct Labour Charges Rs 9,000 Machine Hours Worked 900 Machine Hours Rate 5. Units Produced 17,100Document5 pagesRaw Material Consumed Rs 15,000 Direct Labour Charges Rs 9,000 Machine Hours Worked 900 Machine Hours Rate 5. Units Produced 17,100Jagadeish jagaNo ratings yet

- Edmingle Hiring PostDocument2 pagesEdmingle Hiring PostcompangelNo ratings yet

- Fundamentals of Cost Analysis For Decision Making: True / False QuestionsDocument231 pagesFundamentals of Cost Analysis For Decision Making: True / False QuestionsElaine Gimarino0% (1)

- Sales Budgeting: Sales and Distribution ManagementDocument9 pagesSales Budgeting: Sales and Distribution ManagementBalramNo ratings yet

- Pepsi - Logistics Pepsi - LogisticsDocument15 pagesPepsi - Logistics Pepsi - LogisticsjamilNo ratings yet

- SCM Whats New in Oracle Fusion Cloud Supply PlanningDocument66 pagesSCM Whats New in Oracle Fusion Cloud Supply PlanningYajuvendar GaddamNo ratings yet

- Assignment: Question 1: Why Purchasing Is Important?Document21 pagesAssignment: Question 1: Why Purchasing Is Important?AnzarAijazNo ratings yet

- Breakeven Analysis 2 01042021 104341amDocument27 pagesBreakeven Analysis 2 01042021 104341amrimshaNo ratings yet

- To Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryFrom EverandTo Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryRating: 4 out of 5 stars4/5 (26)

- Summary of Zero to One: Notes on Startups, or How to Build the FutureFrom EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureRating: 4.5 out of 5 stars4.5/5 (100)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (90)

- The Master Key System: 28 Parts, Questions and AnswersFrom EverandThe Master Key System: 28 Parts, Questions and AnswersRating: 5 out of 5 stars5/5 (62)

- Having It All: Achieving Your Life's Goals and DreamsFrom EverandHaving It All: Achieving Your Life's Goals and DreamsRating: 4.5 out of 5 stars4.5/5 (65)

- SYSTEMology: Create time, reduce errors and scale your profits with proven business systemsFrom EverandSYSTEMology: Create time, reduce errors and scale your profits with proven business systemsRating: 5 out of 5 stars5/5 (48)

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurFrom Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurRating: 4.5 out of 5 stars4.5/5 (3)

- The Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelFrom EverandThe Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelRating: 5 out of 5 stars5/5 (51)

- Secrets of the Millionaire Mind: Mastering the Inner Game of WealthFrom EverandSecrets of the Millionaire Mind: Mastering the Inner Game of WealthRating: 4.5 out of 5 stars4.5/5 (1027)