You might also like

- Nume Clasă Statistică: Observaţii: Nota: Serii Disponibile Începând Din 8 Ianuarie 2003 MetodologieDocument3 pagesNume Clasă Statistică: Observaţii: Nota: Serii Disponibile Începând Din 8 Ianuarie 2003 MetodologieAnna AniNo ratings yet

- Graph of The Cash Rate. Graph: Long DescriptionDocument17 pagesGraph of The Cash Rate. Graph: Long DescriptionSyed KunmirNo ratings yet

- ECB Interest Rates @21 March 2016Document1 pageECB Interest Rates @21 March 2016CameliaNo ratings yet

- 27 - Conditional FormattingDocument12 pages27 - Conditional FormattingSyed Mohsin AliNo ratings yet

- Interest Rates of The CBA Operations in Financial Market (%)Document4 pagesInterest Rates of The CBA Operations in Financial Market (%)Alen TadevosyanNo ratings yet

- Kartu Stock Tepung Ujk 2 TGL 22 Feb 2023Document1 pageKartu Stock Tepung Ujk 2 TGL 22 Feb 2023NindraNo ratings yet

- Japan/Ex Rate US/Ex Rate Spain/Ex Rate Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10Document6 pagesJapan/Ex Rate US/Ex Rate Spain/Ex Rate Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10nishimoniNo ratings yet

- GSFS Historical ICD LDS DecDocument5 pagesGSFS Historical ICD LDS DecKunal Abhilashbhai DelwadiaNo ratings yet

- Meses Remu. Basica Asig. Familiar D. S. 045-03-EF D. S. 016-04-EF D. U. 017-2006 LEY #29142 Bono Juridi CcionalDocument4 pagesMeses Remu. Basica Asig. Familiar D. S. 045-03-EF D. S. 016-04-EF D. U. 017-2006 LEY #29142 Bono Juridi CcionalElmer Dixon Paitan HuamaniNo ratings yet

- CondoActive November2010Document3 pagesCondoActive November2010STAORNo ratings yet

- BNRDOBLDocument3 pagesBNRDOBLAlexandra BaesuNo ratings yet

- Monthly Returns (%) Date S&P 500 DateDocument5 pagesMonthly Returns (%) Date S&P 500 Daterishabh poniyaNo ratings yet

- Deflation Fears GrowDocument3 pagesDeflation Fears Growderailedcapitalism.comNo ratings yet

- Group 1 - Echo - Economic ReportDocument18 pagesGroup 1 - Echo - Economic ReportDale RomeroNo ratings yet

- Order MarDocument19 pagesOrder Marhayder aliNo ratings yet

- Interest Rate Structure of Commercial Banks-2060-07Document2 pagesInterest Rate Structure of Commercial Banks-2060-07paudel_111111No ratings yet

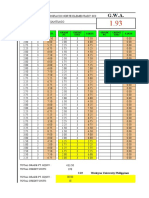

- GWA-Conversion 11Document6 pagesGWA-Conversion 11Sharlene Lynnette PabloNo ratings yet

- Demand ForecastingDocument3 pagesDemand ForecastingTahmid Ismail 1831665642No ratings yet

- Pemakaian Lem Ujk 2 TGL 22 Feb 2023Document1 pagePemakaian Lem Ujk 2 TGL 22 Feb 2023NindraNo ratings yet

- 05.perhitungan HujanDocument31 pages05.perhitungan HujanMphNo ratings yet

- 2021-01-Model Precios Gral PRESUP Dic-21Document331 pages2021-01-Model Precios Gral PRESUP Dic-21Florencia MucarzelNo ratings yet

- World Steel Prices 11-Apr-07Document11 pagesWorld Steel Prices 11-Apr-07joblessiceNo ratings yet

- Hedged Strategy CheatsheetDocument2 pagesHedged Strategy CheatsheetAdam100% (3)

- Shift NO Teacher Target Date: Present Points Earned AM 1 Abby 28 June 2-30, 2014 10 15 20Document2 pagesShift NO Teacher Target Date: Present Points Earned AM 1 Abby 28 June 2-30, 2014 10 15 20Christine Aev OlasaNo ratings yet

- 50 Macroeconomic IndicatorsDocument54 pages50 Macroeconomic Indicatorskrishnanshu sarafNo ratings yet

- Cardex Jul Agos 20011Document127 pagesCardex Jul Agos 20011Brandon Tamara ChipaNo ratings yet

- Cycles of GoldDocument18 pagesCycles of GoldfinancegovNo ratings yet

- Income and Expense1Document3 pagesIncome and Expense1si537217No ratings yet

- Random Account LedgerDocument5 pagesRandom Account LedgerAri SchwartzNo ratings yet

- Wealth Street Capital 3 - Account Ledger PDFDocument5 pagesWealth Street Capital 3 - Account Ledger PDFAri SchwartzNo ratings yet

- Lowest Since 1955 Lowest Since 1961 Lowest Since 1955Document1 pageLowest Since 1955 Lowest Since 1961 Lowest Since 1955Piyush ShahNo ratings yet

- Correlation (Nifty and GDP)Document3 pagesCorrelation (Nifty and GDP)pulkitnarang1606No ratings yet

- The Fii Money and The Market TrendDocument8 pagesThe Fii Money and The Market Trendganeshgce09No ratings yet

- YouDocument2 pagesYouhaikal japan shopNo ratings yet

- Bill Evans Business Bank Economic Briefing-March 2023Document36 pagesBill Evans Business Bank Economic Briefing-March 2023chingweisuNo ratings yet

- Seasonally Adjusted U-6 DataDocument26 pagesSeasonally Adjusted U-6 DataZerohedgeNo ratings yet

- Presentation On: Submitted byDocument19 pagesPresentation On: Submitted byabhay_prakash_ranjanNo ratings yet

- Dataset EA MPDDocument105 pagesDataset EA MPDuniversal dubaiNo ratings yet

- Project Report For Paper Cup MachineDocument22 pagesProject Report For Paper Cup MachineSHRUTI AGRAWALNo ratings yet

- 47.75 Hours: Plan BalanceDocument1 page47.75 Hours: Plan Balancejjohnson4sky.comNo ratings yet

- Daftar Nilai Us Jenjang SD Mi Kecamatan LinggabayuDocument1 pageDaftar Nilai Us Jenjang SD Mi Kecamatan LinggabayuRafelly Seth TrcNo ratings yet

- Cash Reserve Ratio and Interest RatesDocument27 pagesCash Reserve Ratio and Interest Ratesritusharma19832000No ratings yet

- Consumo Diario Real NGR Semana Fecha Venta Diaria Tarjetas de Crédito Tarjetas de Débito EfectivoDocument39 pagesConsumo Diario Real NGR Semana Fecha Venta Diaria Tarjetas de Crédito Tarjetas de Débito EfectivoCristian ReyesNo ratings yet

- India'S Balance of Payments (Bop) During First Quarter (April-June 2006) of 2006-07Document6 pagesIndia'S Balance of Payments (Bop) During First Quarter (April-June 2006) of 2006-07vijaysai31No ratings yet

- January February March April May June July August Septemb Er Novemb Er Decemb ErDocument2 pagesJanuary February March April May June July August Septemb Er Novemb Er Decemb ErLorde WagayenNo ratings yet

- Household Goods RetailingDocument2 pagesHousehold Goods Retailingabeda shaikhNo ratings yet

- Clase - Teoria Portafolio FinalDocument12 pagesClase - Teoria Portafolio FinalMilagros Mendoza QuintanillaNo ratings yet

- Riot - Us 16 April 2008 PDFDocument1 pageRiot - Us 16 April 2008 PDFnarbiliNo ratings yet

- Data Bars Color Scales Icon Sets Greater Than 400 Within Top 40%Document1 pageData Bars Color Scales Icon Sets Greater Than 400 Within Top 40%khaleddddNo ratings yet

- Structure of Interest Rates - I: Service Charges/Mark Up Rates of Refinance Facility For SmesDocument4 pagesStructure of Interest Rates - I: Service Charges/Mark Up Rates of Refinance Facility For Smessherman ullahNo ratings yet

- Jabatan Perkhidmatan Veterinar Harga Daging Ayam 2020Document3 pagesJabatan Perkhidmatan Veterinar Harga Daging Ayam 2020Paklo NaimNo ratings yet

- Jawaban Latihan InventoryDocument10 pagesJawaban Latihan Inventoryp3trusratuanikNo ratings yet

- Domestic Term Deposit Rates History FinalDocument2 pagesDomestic Term Deposit Rates History FinalNethajiNo ratings yet

- Excel PracticeDocument13 pagesExcel Practicesahuaditya2009No ratings yet

- HBS Table No. 44 Major Monetary Policy Measures - Bank Rate, CRR & SLRDocument7 pagesHBS Table No. 44 Major Monetary Policy Measures - Bank Rate, CRR & SLRSOHAM DEONo ratings yet

- ACC102 - Fundamentals of Accounting IIDocument10 pagesACC102 - Fundamentals of Accounting IIalka murarkaNo ratings yet

- Three Months EIBOR Rates Trend - HSBC Review MonthsDocument1 pageThree Months EIBOR Rates Trend - HSBC Review Monthsmohammed el erianNo ratings yet

- Capital Asset Pricing Model PT. Astra International Tbk. (ASII) PT. Astra International Tbk. (ASII) Ihsg Tahun Bulan Harga Saham Ri Tahun Bulan Harga Saham RMDocument2 pagesCapital Asset Pricing Model PT. Astra International Tbk. (ASII) PT. Astra International Tbk. (ASII) Ihsg Tahun Bulan Harga Saham Ri Tahun Bulan Harga Saham RMStephant Delahoya SihombingNo ratings yet

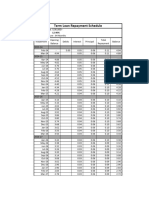

- Term Loan Repayment ScheduleDocument2 pagesTerm Loan Repayment ScheduleVijay HemwaniNo ratings yet

- 1 Jan .... 4 ArticlesDocument10 pages1 Jan .... 4 Articlesnafa nuksanNo ratings yet

- F1 1 Corporate India Women On Boards Nov 2022 73e437d36eDocument38 pagesF1 1 Corporate India Women On Boards Nov 2022 73e437d36enafa nuksanNo ratings yet

- Petrol Price U and Down How Many TimesDocument2 pagesPetrol Price U and Down How Many Timesnafa nuksanNo ratings yet

- World Bank View On Commodity Prices 02 13Document4 pagesWorld Bank View On Commodity Prices 02 13nafa nuksanNo ratings yet

- Rental Index Q4 Oct 2022Document18 pagesRental Index Q4 Oct 2022nafa nuksanNo ratings yet

- Rajya Sabha Unstarred Question No-1832 Loans Written OffDocument6 pagesRajya Sabha Unstarred Question No-1832 Loans Written Offnafa nuksanNo ratings yet

- Rajya Sabha Unstarred Question No-1592Document2 pagesRajya Sabha Unstarred Question No-1592nafa nuksanNo ratings yet

- Statewise LPG ConnectionsDocument2 pagesStatewise LPG Connectionsnafa nuksanNo ratings yet

- MSME Unts Statewise and EmploymentDocument2 pagesMSME Unts Statewise and Employmentnafa nuksanNo ratings yet

- Lok Sabha Un-Starred Question No. 2311Document5 pagesLok Sabha Un-Starred Question No. 2311nafa nuksanNo ratings yet

- Nature of EconomyDocument9 pagesNature of Economypriyanka shahNo ratings yet

- Jurnal Goldchip 2Document39 pagesJurnal Goldchip 2DewaSatriaNo ratings yet

- First Come First Serve Scheme 2022 CircularDocument2 pagesFirst Come First Serve Scheme 2022 CircularAshish SharmaNo ratings yet

- Quiz 4 Intangible Assets QuestionsDocument3 pagesQuiz 4 Intangible Assets QuestionsJessica Marie MigrasoNo ratings yet

- John J Murphy - Technical Analysis of The Financial MarketsDocument596 pagesJohn J Murphy - Technical Analysis of The Financial Marketsbarbarajeanlavender97% (75)

- Internship ReportDocument33 pagesInternship Reportstreamingmedia786No ratings yet

- As We All Are AwareDocument17 pagesAs We All Are AwaremgrfanNo ratings yet

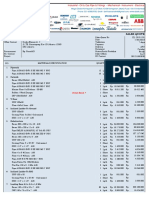

- Order Confirmation PDFDocument2 pagesOrder Confirmation PDFDisk HunterNo ratings yet

- UK Financial Regulation Ed23-5 PDFDocument298 pagesUK Financial Regulation Ed23-5 PDFVincenzo Somma100% (2)

- E - Interim Report 2020Document166 pagesE - Interim Report 2020New KabisaNo ratings yet

- Full Download Test Bank For M Finance 4th Edition Marcia Cornett Troy Adair John Nofsinger PDF Full ChapterDocument34 pagesFull Download Test Bank For M Finance 4th Edition Marcia Cornett Troy Adair John Nofsinger PDF Full Chapterexequycheluract6oi100% (22)

- E PSDA Assignment For Project Management (BBA 302) Date of Submission: 13 April 2020Document12 pagesE PSDA Assignment For Project Management (BBA 302) Date of Submission: 13 April 2020Naman SethNo ratings yet

- Permanent Associate MembersDocument20 pagesPermanent Associate MembersRishi GandhiNo ratings yet

- SK BirDocument2 pagesSK BirGem LarezaNo ratings yet

- Lecture 04 - Currency DerivativesDocument10 pagesLecture 04 - Currency DerivativesTrương Ngọc Minh ĐăngNo ratings yet

- 10 K 12 31 19 9Document85 pages10 K 12 31 19 9Conny CastroNo ratings yet

- Penawaran BerthaDocument2 pagesPenawaran BerthaTito AdiNo ratings yet

- PAS 1 Presentation of Financial Statements: Quiz 1: Multiple ChoiceDocument3 pagesPAS 1 Presentation of Financial Statements: Quiz 1: Multiple Choicetrixie mae88% (8)

- cl-12 Economics Lesson Plan 2023-24Document30 pagescl-12 Economics Lesson Plan 2023-24kuldeepbhatt0786No ratings yet

- Maharashtra-14 Results1Document103 pagesMaharashtra-14 Results1Sandesh KaradNo ratings yet

- When Is The Best Time To Buy A StockDocument11 pagesWhen Is The Best Time To Buy A StockAnonymous w6TIxI0G8lNo ratings yet

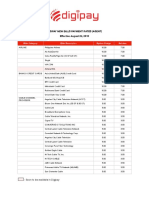

- DIGIPAY New Rates Agent PDFDocument41 pagesDIGIPAY New Rates Agent PDFMye-Khel Lagunay AwayanNo ratings yet

- Chapter 2Document30 pagesChapter 2DianaNo ratings yet

- Finmar ReviewerDocument5 pagesFinmar ReviewerGelly Dominique GuijoNo ratings yet

- Microeconomics 21st Edition McConnell Solutions Manual 1Document10 pagesMicroeconomics 21st Edition McConnell Solutions Manual 1russell100% (48)

- Measuring The Cost of LivingDocument5 pagesMeasuring The Cost of LivingEdmar OducayenNo ratings yet

- OMZIL MID YEAR 2021 FINANCIAL RESULTS FINAL From Lawrence 31AUG21Document10 pagesOMZIL MID YEAR 2021 FINANCIAL RESULTS FINAL From Lawrence 31AUG21Mandisi MoyoNo ratings yet

- Wallstreetjournal 20171128 TheWallStreetJournalDocument34 pagesWallstreetjournal 20171128 TheWallStreetJournalsadaq84No ratings yet

- Heros Convent HR - Sec.School First Term Examination Class - 4 Maths M.M.80Document3 pagesHeros Convent HR - Sec.School First Term Examination Class - 4 Maths M.M.80sunny singhNo ratings yet

- Hatten Land Forms Joint Venture With Singapore Fintech Group Hydra XDocument4 pagesHatten Land Forms Joint Venture With Singapore Fintech Group Hydra XWeR1 Consultants Pte LtdNo ratings yet

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Risk Management: Concepts and Guidance, Fifth EditionFrom EverandRisk Management: Concepts and Guidance, Fifth EditionRating: 4.5 out of 5 stars4.5/5 (10)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Data Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBIFrom EverandData Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBINo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)