You might also like

- Credit Repair Letters To Remove Debt StrawmanDocument75 pagesCredit Repair Letters To Remove Debt StrawmanRon Mowles98% (220)

- Fabm2: Quarter 1 Module 2 New Normal ABM For Grade 12Document16 pagesFabm2: Quarter 1 Module 2 New Normal ABM For Grade 12Nonilon RoblesNo ratings yet

- Q1 M1 M4 Business Finance Activity SheetDocument10 pagesQ1 M1 M4 Business Finance Activity SheetTrina LariosaNo ratings yet

- KPL Swing Trading SystemDocument6 pagesKPL Swing Trading SystemRushank ShuklaNo ratings yet

- Money Market and Capital MarketDocument36 pagesMoney Market and Capital Marketmisakisakura1102No ratings yet

- Analysis and Interpretation Name: - of Financial Statements 2 SectionDocument5 pagesAnalysis and Interpretation Name: - of Financial Statements 2 SectionMylene Santiago100% (1)

- 2018 Audited Financial StatementDocument175 pages2018 Audited Financial StatementTULIO, Jeremy I.No ratings yet

- Ch. 2. Asset Pricing Theory (721383S) : Juha Joenväärä University of Oulu March 2014Document31 pagesCh. 2. Asset Pricing Theory (721383S) : Juha Joenväärä University of Oulu March 2014Asma DahmenNo ratings yet

- Ong Motors CorporationDocument4 pagesOng Motors CorporationJudy Ann Acruz100% (1)

- GEN 010 For BSA INVESTMENTS IN DEBT SECURITIESDocument7 pagesGEN 010 For BSA INVESTMENTS IN DEBT SECURITIESJoy RadaNo ratings yet

- John Paulson Risk in Risk ArbitrageDocument11 pagesJohn Paulson Risk in Risk ArbitrageChapersonNo ratings yet

- Quiz Bank Recon and Proof of CashDocument3 pagesQuiz Bank Recon and Proof of CashAlexander ONo ratings yet

- Fabm2 SLK Week 2 - 3 SCIDocument11 pagesFabm2 SLK Week 2 - 3 SCIMylene SantiagoNo ratings yet

- Accounting Cycle of A Service Business-Step 5-Adjusting EntriesDocument18 pagesAccounting Cycle of A Service Business-Step 5-Adjusting EntriesdelgadojudithNo ratings yet

- ABM-FABM2 12 - Q1 - W2 - Mod2Document16 pagesABM-FABM2 12 - Q1 - W2 - Mod2Jose John Vocal83% (18)

- Module #6Document20 pagesModule #6Joy RadaNo ratings yet

- MODULE 7 and 8 ACCDocument3 pagesMODULE 7 and 8 ACCnorie jane pacisNo ratings yet

- ACC 113 - SAS - Day - 15Document11 pagesACC 113 - SAS - Day - 15Joy QuitorianoNo ratings yet

- IC102 Accounting 1 (Week 7 M3-L3) - HandoutsDocument27 pagesIC102 Accounting 1 (Week 7 M3-L3) - HandoutsLj TvNo ratings yet

- Tanauan Institute, Inc.: Completing The Cycle For A Merchandising Business Part 1Document7 pagesTanauan Institute, Inc.: Completing The Cycle For A Merchandising Business Part 1Hanna CaraigNo ratings yet

- ACC 113 - SAS - Day - 19Document11 pagesACC 113 - SAS - Day - 19Joy QuitorianoNo ratings yet

- Ncert SolutionsDocument33 pagesNcert SolutionsArif ShaikhNo ratings yet

- Management PresentationDocument61 pagesManagement Presentationiffat.stu2018No ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Budgeting: Accounting CycleDocument3 pagesBudgeting: Accounting CycleDyane CruzNo ratings yet

- Lesson Title: Revenue Recognition - Consignment AccountingDocument8 pagesLesson Title: Revenue Recognition - Consignment AccountingFeedback Or BawiNo ratings yet

- Dr. M. D. Chase Long Beach State University Accounting 300A-10A The Operating Cycle: Worksheet/Closing EntriesDocument20 pagesDr. M. D. Chase Long Beach State University Accounting 300A-10A The Operating Cycle: Worksheet/Closing EntriesDanilo QuinsayNo ratings yet

- Attachment - 1 - 2024-02-26T035237.776Document8 pagesAttachment - 1 - 2024-02-26T035237.776chriswairuraNo ratings yet

- ACC 113 - SAS - Day - 2Document8 pagesACC 113 - SAS - Day - 2Joy QuitorianoNo ratings yet

- POA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809amDocument65 pagesPOA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809ammuhammad atifNo ratings yet

- Week 5 Lecture Notes (1 Slide)Document67 pagesWeek 5 Lecture Notes (1 Slide)MEIWEI LINo ratings yet

- Closing EntriesDocument13 pagesClosing EntriesAlliyah Manzano CalvoNo ratings yet

- Learning Guide: Accounts and Budget ServiceDocument33 pagesLearning Guide: Accounts and Budget ServicerameNo ratings yet

- Module 10 - The Financial Statements IIDocument11 pagesModule 10 - The Financial Statements IINina AlexineNo ratings yet

- Sas#23 Acc104Document6 pagesSas#23 Acc104Charisse April MaisoNo ratings yet

- Sas21 Acc115Document7 pagesSas21 Acc115crpa.lina.cocNo ratings yet

- Acc 118 Mod 3Document8 pagesAcc 118 Mod 3Rona Amor MundaNo ratings yet

- M8 Correcting Closing Reversing Entries and Financial StatementsDocument10 pagesM8 Correcting Closing Reversing Entries and Financial StatementsMicha AlcainNo ratings yet

- LAS ABM - FABM12 Ic D 5 6 Week 2Document7 pagesLAS ABM - FABM12 Ic D 5 6 Week 2ROMMEL RABONo ratings yet

- Task 4Document7 pagesTask 4babluanandNo ratings yet

- Manage Finances Within The BudgetDocument12 pagesManage Finances Within The BudgetEsteban BuitragoNo ratings yet

- FUNDAMENTALS OF ABM 1 Section 7Document13 pagesFUNDAMENTALS OF ABM 1 Section 7Allysa Kim RubisNo ratings yet

- Q4 Applied Entrepreneurship 11 12 WEEK 4Document4 pagesQ4 Applied Entrepreneurship 11 12 WEEK 4Marife Buctot CulabaNo ratings yet

- Learning Guide: Accounts and Budget ServiceDocument33 pagesLearning Guide: Accounts and Budget ServiceMitiku BerhanuNo ratings yet

- Accounting 1 Module 3Document20 pagesAccounting 1 Module 3Rose Marie Recorte100% (1)

- Chapter 10 - Mid Test TranslationDocument11 pagesChapter 10 - Mid Test TranslationraniNo ratings yet

- Business and Management 2: Fundamentals of AccountancyDocument11 pagesBusiness and Management 2: Fundamentals of AccountancyZed MercyNo ratings yet

- Admas University: Answer SheetDocument6 pagesAdmas University: Answer SheetSamuel100% (2)

- Hhtfa8e ch01 WP 1Document87 pagesHhtfa8e ch01 WP 1rishirawr0% (1)

- Leve 2 Coc ExamDocument45 pagesLeve 2 Coc Exameferem92% (38)

- Financial Acctg Reporting 1 Chapter 5Document20 pagesFinancial Acctg Reporting 1 Chapter 5Charise Jane ZullaNo ratings yet

- Module #11Document7 pagesModule #11Joy RadaNo ratings yet

- Leve 2 Coc ExamDocument45 pagesLeve 2 Coc Examsamuel asefa100% (2)

- FABM2 Quarter 1 Module and WorksheetsDocument27 pagesFABM2 Quarter 1 Module and WorksheetsHeart polvos100% (1)

- DK Goel Solutions Class 11 Chapter 22 DK Goel Book Available For FreeDocument1 pageDK Goel Solutions Class 11 Chapter 22 DK Goel Book Available For Freetwinkle banganiNo ratings yet

- 7-Completing The Accounting CycleDocument12 pages7-Completing The Accounting Cyclechobiipiggy26No ratings yet

- Managerial Level: May 2007 ExaminationsDocument35 pagesManagerial Level: May 2007 ExaminationsIsavic AlsinaNo ratings yet

- Business Finance Note 2Document19 pagesBusiness Finance Note 2Ruth MuñozNo ratings yet

- Q1 LAS Business Finance 12 Week 3-4Document11 pagesQ1 LAS Business Finance 12 Week 3-4Flare ColterizoNo ratings yet

- Q1 LAS Business Finance 12 Week 3-4Document11 pagesQ1 LAS Business Finance 12 Week 3-4Gerlie BorneaNo ratings yet

- Unit-18 Understanding Profit & Loss StatementDocument8 pagesUnit-18 Understanding Profit & Loss StatementAdefolajuwon ShoberuNo ratings yet

- FABM2 Module 2. Statement of Comprehensive IncomeDocument13 pagesFABM2 Module 2. Statement of Comprehensive IncomeSITTIE RAYMAH ABDULLAHNo ratings yet

- Fabm 121.week 6-10 ModuleDocument22 pagesFabm 121.week 6-10 Modulekhaizer matias100% (1)

- Chapter 5Document33 pagesChapter 5meahangela.labadan.23No ratings yet

- Fabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionDocument16 pagesFabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionJosephine C QuibidoNo ratings yet

- Tanauan Institute, Inc.: Using The Worksheet and Closing and Reversing Entries - Finishing The Accounting CycleDocument10 pagesTanauan Institute, Inc.: Using The Worksheet and Closing and Reversing Entries - Finishing The Accounting CycleHanna CaraigNo ratings yet

- Accounting GR 10 - MBL-LIPs-Week10Document5 pagesAccounting GR 10 - MBL-LIPs-Week10wandeerNo ratings yet

- Module #16Document21 pagesModule #16Joy RadaNo ratings yet

- Module #23Document8 pagesModule #23Joy RadaNo ratings yet

- Module #18Document7 pagesModule #18Joy RadaNo ratings yet

- Module #2Document8 pagesModule #2Joy RadaNo ratings yet

- Module #11Document7 pagesModule #11Joy RadaNo ratings yet

- Module #10Document7 pagesModule #10Joy RadaNo ratings yet

- Module #1Document7 pagesModule #1Joy RadaNo ratings yet

- Fundamental Analysis of TCSDocument15 pagesFundamental Analysis of TCSarupritNo ratings yet

- Ats Taxation PDFDocument372 pagesAts Taxation PDFOlawaleNo ratings yet

- Matalino Corporation FSDocument2 pagesMatalino Corporation FSAiron AlongNo ratings yet

- 8db6 - ING Insurance - Asia-PacificDocument16 pages8db6 - ING Insurance - Asia-PacificJessica LopezNo ratings yet

- Adjusting Entries FSDocument31 pagesAdjusting Entries FSMylene Salvador100% (1)

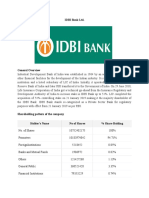

- IDBI Bank LTDDocument3 pagesIDBI Bank LTDSololoNo ratings yet

- AUTO - 0ar Aop 2014 PDFDocument276 pagesAUTO - 0ar Aop 2014 PDFAndro BonerezNo ratings yet

- $CMRY Equity Research ReportDocument10 pages$CMRY Equity Research ReportAzka RifkyNo ratings yet

- IFRS Core Tools PDFDocument33 pagesIFRS Core Tools PDFGere TassewNo ratings yet

- Consumer Cards Overview Side by SideDocument6 pagesConsumer Cards Overview Side by SidewewaewaNo ratings yet

- Plan de Conturi Engleza 2016 PDFDocument4 pagesPlan de Conturi Engleza 2016 PDFMadalina BogdanNo ratings yet

- Scheme of WorkDocument65 pagesScheme of WorkMUHAMMAD SAUD A LEVEL BURKINo ratings yet

- Mint 23-8 DelhiDocument18 pagesMint 23-8 DelhiGoutham SunderNo ratings yet

- 0 Airbus BrazilDocument6 pages0 Airbus BrazilZohra BoureniNo ratings yet

- Run For Your Life Group Task - FinalDocument4 pagesRun For Your Life Group Task - Finalits2koolNo ratings yet

- ECON PS 1 With Soln by Julius GrazaDocument3 pagesECON PS 1 With Soln by Julius GrazaEzlan HarithNo ratings yet

- RWA Tokenization - The Next Generation of Capital MarketsDocument47 pagesRWA Tokenization - The Next Generation of Capital Marketssriharsha.vellanki.nitieNo ratings yet

- Accounting Ch10Document77 pagesAccounting Ch10Julaeva KhaironesyyaNo ratings yet

- Property, Plant & Equipment: Associate Professor Parmod ChandDocument46 pagesProperty, Plant & Equipment: Associate Professor Parmod ChandSunila DeviNo ratings yet

- Contol Soal Partnership Akuntansi Keuangan Lanjutan 1Document3 pagesContol Soal Partnership Akuntansi Keuangan Lanjutan 1Istiqlal RamadhanNo ratings yet

- Part 1. Multiple Choice Questions There Are 10 Questions in This Part. Answer ALL Questions. Give ONE Answer Only For EachDocument5 pagesPart 1. Multiple Choice Questions There Are 10 Questions in This Part. Answer ALL Questions. Give ONE Answer Only For EachDung ThùyNo ratings yet

- Abc Analysis-Adv Accounts May 2024Document1 pageAbc Analysis-Adv Accounts May 2024Looney ApacheNo ratings yet