You might also like

- Bank Assurance Applied at Sbi Project Report Mba FinanceDocument106 pagesBank Assurance Applied at Sbi Project Report Mba FinanceBabasab Patil (Karrisatte)50% (2)

- Yes Bank Mainstreaming Development Into Indian BankingDocument20 pagesYes Bank Mainstreaming Development Into Indian Bankinggauarv_singh13No ratings yet

- Distribution Channel of SBI Life Insurance - S&DDocument14 pagesDistribution Channel of SBI Life Insurance - S&DNaina BakshiNo ratings yet

- Accounting Practice SetDocument33 pagesAccounting Practice SetANDAYA SHERLYN67% (3)

- BancassuranceDocument7 pagesBancassuranceAbraham PradeepNo ratings yet

- An Analysis On Contribution of Bancassurance On Financial Performance of Bank of IndiDocument13 pagesAn Analysis On Contribution of Bancassurance On Financial Performance of Bank of IndiAlexander DeckerNo ratings yet

- Bancassurance in IndiaDocument13 pagesBancassurance in IndiaSahil SinglaNo ratings yet

- BANCASSURANCEDocument15 pagesBANCASSURANCEBhavsimran S. Syal0% (1)

- 11 - Chapter 4Document92 pages11 - Chapter 4sushilaNo ratings yet

- BancassuranceDocument24 pagesBancassuranceRushikesh KulkarniNo ratings yet

- A Study of Branchless Banking in AchieviDocument10 pagesA Study of Branchless Banking in AchieviMiftah AlfaridNo ratings yet

- Bancassurance ProjectDocument32 pagesBancassurance Projectajayajayajayajay7777No ratings yet

- Unit - 5: Overview of Current Trends in Service IndustriesDocument16 pagesUnit - 5: Overview of Current Trends in Service IndustriesRiya KaushikNo ratings yet

- Bancassurance: An Indian PerspectiveDocument17 pagesBancassurance: An Indian Perspectivealmeidabrijet100% (1)

- Introduction to Bancassurance: Merging Banking and InsuranceDocument61 pagesIntroduction to Bancassurance: Merging Banking and Insuranceprabs9869No ratings yet

- Introduction to Bancassurance: Bank-Insurance PartnershipsDocument56 pagesIntroduction to Bancassurance: Bank-Insurance PartnershipsRavi Bhushan SharmaNo ratings yet

- Life Insurance Market in India: Dr. Sudas RoyDocument21 pagesLife Insurance Market in India: Dr. Sudas RoypriyamdawnNo ratings yet

- Project On Standard Charted BankDocument82 pagesProject On Standard Charted BankViPul82% (11)

- Indian Banking SectorsDocument4 pagesIndian Banking SectorsAamir KhanNo ratings yet

- Banking - Positives NegativesDocument9 pagesBanking - Positives NegativesraviNo ratings yet

- Presentation: BancassuranceDocument14 pagesPresentation: BancassurancemenonpratishNo ratings yet

- Bancassurance India Insurance Bank DistributionDocument4 pagesBancassurance India Insurance Bank Distributionsrinath121No ratings yet

- Group Report on Commercial BanksDocument85 pagesGroup Report on Commercial BanksPriyank Agarwal100% (1)

- Ban Cass UrnaceDocument29 pagesBan Cass UrnaceShobhit SaxenaNo ratings yet

- BancassuranceDocument15 pagesBancassuranceRakesh BhanjNo ratings yet

- Retail Banking: Indian Financial SystemDocument17 pagesRetail Banking: Indian Financial SystemKunal KothariNo ratings yet

- Industry Reports - ISB Consulting Casebook 2021Document36 pagesIndustry Reports - ISB Consulting Casebook 2021BalajiNo ratings yet

- Project Report: Executive SummaryDocument32 pagesProject Report: Executive SummaryAbhijit PhoenixNo ratings yet

- Thesis Topics in Banking SectorDocument8 pagesThesis Topics in Banking Sectorarianadavishighpoint100% (2)

- Analysis of Icici and PNB Marketing EssayDocument13 pagesAnalysis of Icici and PNB Marketing EssayRonald MurphyNo ratings yet

- Insurance: Name-Mukta Wadhwa Class - Roll No. - 52 Topic - BancassuranceDocument15 pagesInsurance: Name-Mukta Wadhwa Class - Roll No. - 52 Topic - Bancassurancemuktawadhwa4No ratings yet

- Banc AssuranceDocument90 pagesBanc AssuranceRohit SharmaNo ratings yet

- Trends and Development in Financial Sector: NCRD'S Sterling Institute of Management StudiesDocument15 pagesTrends and Development in Financial Sector: NCRD'S Sterling Institute of Management StudiesShreelekha PillaiNo ratings yet

- Nagindas Khandwa La CollegeDocument20 pagesNagindas Khandwa La CollegeSonam ShindeNo ratings yet

- Introduction To BancassuranceDocument50 pagesIntroduction To BancassuranceGarima Gupta100% (1)

- Bank Assurance PDFDocument61 pagesBank Assurance PDFYash SutarNo ratings yet

- Reengineering The Business of Banking in IndiaDocument18 pagesReengineering The Business of Banking in IndiaHemant DeshmukhNo ratings yet

- Bancassurance: New Marketing Product For The BanksDocument21 pagesBancassurance: New Marketing Product For The BanksBhoomika SahuNo ratings yet

- A Study On Bancassurance at State Bank of India, AgraDocument108 pagesA Study On Bancassurance at State Bank of India, AgrasuryakantshrotriyaNo ratings yet

- Financial InclusiionDocument37 pagesFinancial InclusiionPehoo ThakurNo ratings yet

- NavdeepDocument18 pagesNavdeepArshdeep SinghNo ratings yet

- Banking and NBFC - Module 4 - NBFC Products Deposit BasedDocument43 pagesBanking and NBFC - Module 4 - NBFC Products Deposit Basednandhakumark152No ratings yet

- Analysis of Icici BankDocument7 pagesAnalysis of Icici BankAnkur MathurNo ratings yet

- Executive SummaryDocument12 pagesExecutive Summaryabhishek_karumbaiahNo ratings yet

- Scope of The Bank ManagementDocument5 pagesScope of The Bank ManagementHari PrasadNo ratings yet

- Industry Analysis: Current Trends in The IndustryDocument7 pagesIndustry Analysis: Current Trends in The IndustryAshish GutgutiaNo ratings yet

- UTI BankDocument69 pagesUTI BankSnehal RunwalNo ratings yet

- 2.12, Ms. Babita YadavDocument23 pages2.12, Ms. Babita Yadavpoojamittal_260% (1)

- A Project On Banking SectorDocument81 pagesA Project On Banking SectorAkbar SinghNo ratings yet

- BancassuranceDocument76 pagesBancassurancekevalcool25050% (2)

- Standerd ChartedDocument58 pagesStanderd ChartedashishgargNo ratings yet

- Indian BankingDocument4 pagesIndian Bankingrahul vatsyayanNo ratings yet

- "Mobile Banking" SBI by Komal Sawant: A Project Report ONDocument27 pages"Mobile Banking" SBI by Komal Sawant: A Project Report ONsanket yelaweNo ratings yet

- Banc AssuranceDocument3 pagesBanc AssurancepavneetsinghrainaNo ratings yet

- Retail BankingDocument45 pagesRetail BankingdrlalitmohanNo ratings yet

- To Kindle Interest in Economic Affairs... To Empower The Student Community... WWW - Sib.co - in Ho @sib - Co.inDocument8 pagesTo Kindle Interest in Economic Affairs... To Empower The Student Community... WWW - Sib.co - in Ho @sib - Co.inViplove BohraNo ratings yet

- Financial Inclusion, Microfinance and Micro InsuranceDocument14 pagesFinancial Inclusion, Microfinance and Micro InsuranceBalendu BhagatNo ratings yet

- Report On Micro FinanceDocument55 pagesReport On Micro Financearvind.vns14395% (73)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- AP TopUp 26042012Document2 pagesAP TopUp 26042012Ravi KrishnaNo ratings yet

- Indian Software IndustryDocument6 pagesIndian Software IndustryRavi KrishnaNo ratings yet

- Budget Speech - 7 DecemberDocument20 pagesBudget Speech - 7 DecemberSwadeep ChhetriNo ratings yet

- Indian Pharma Industry Presentation 010709Document88 pagesIndian Pharma Industry Presentation 010709workosaur100% (2)

- Sec 167Document8 pagesSec 167Ravi KrishnaNo ratings yet

- PT. Telkomsel LTE Monitoring Rollout: High Level Topology For Mobile Backhaul Performance MonitoringDocument5 pagesPT. Telkomsel LTE Monitoring Rollout: High Level Topology For Mobile Backhaul Performance MonitoringLodewijk SitompulNo ratings yet

- AKW104 CourseOutlineDocument8 pagesAKW104 CourseOutlineHazwani HussainNo ratings yet

- Legal Risks of NursesDocument7 pagesLegal Risks of NursesBrian DeanNo ratings yet

- Ins 10815398 051117-2Document1 pageIns 10815398 051117-2fadliNo ratings yet

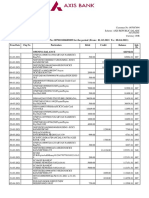

- Statement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)Document3 pagesStatement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)LakshayNo ratings yet

- APPS Rating and ReviewsDocument83 pagesAPPS Rating and ReviewsApurbh Singh KashyapNo ratings yet

- Este Documento Es Aceptado Tributariamente Por SunatDocument2 pagesEste Documento Es Aceptado Tributariamente Por SunatMelissa CongonaNo ratings yet

- DHL Ecommerce Parcel International DirectDocument3 pagesDHL Ecommerce Parcel International DirectLorena ChagarteguiNo ratings yet

- CEM CJs Conformance Certification Report Huawei SmartCare For STC Final v1.3 1Document141 pagesCEM CJs Conformance Certification Report Huawei SmartCare For STC Final v1.3 1Sir GembuLNo ratings yet

- ROIMC033109Document1 pageROIMC033109marinescu danNo ratings yet

- Plastic Money Types and History ExplainedDocument49 pagesPlastic Money Types and History ExplainedTanya Hughes100% (1)

- Demand Letter Ms LeonyDocument2 pagesDemand Letter Ms Leonyfe garcia macasaetNo ratings yet

- Distribution Channels Master ThesisDocument4 pagesDistribution Channels Master Thesismichelelataseattle100% (2)

- Purple Futuristic Pitch Deck PresentationDocument30 pagesPurple Futuristic Pitch Deck PresentationEljine OchoaNo ratings yet

- Icare Recover PDFDocument1 pageIcare Recover PDFPIETRO DAVID DE LUCANo ratings yet

- Flipkart Company Profile and Growth AnalysisDocument18 pagesFlipkart Company Profile and Growth AnalysisKrishnaNo ratings yet

- Du Tran New Partner - Press ReleaseDocument1 pageDu Tran New Partner - Press ReleaseTranDuVanNo ratings yet

- Airtel Xstream Vs JioFiber Vs Tata Sky Vs BSNL Vs Excitel Rs 999 Internet PlanDocument3 pagesAirtel Xstream Vs JioFiber Vs Tata Sky Vs BSNL Vs Excitel Rs 999 Internet PlanhinduNo ratings yet

- 11th Accountancy Full Study Material English Medium 2023-24Document64 pages11th Accountancy Full Study Material English Medium 2023-24osama guyzz100% (1)

- Auditing Expenditure Cycle TestsDocument22 pagesAuditing Expenditure Cycle Testsmacmac29No ratings yet

- Itil v3 Highlights Web Version v15 1234429588478670 1Document0 pagesItil v3 Highlights Web Version v15 1234429588478670 1cmurrieta20092426No ratings yet

- Case1 Central TransportDocument1 pageCase1 Central TransportCarolina0% (1)

- Quiz Daw 1Document3 pagesQuiz Daw 1Justin Rome PagulayanNo ratings yet

- NostroDocument8 pagesNostrosahilagl23_121905585No ratings yet

- Invoice 022Document1 pageInvoice 022SiddhantNo ratings yet

- CIF and FOB ContractsDocument14 pagesCIF and FOB ContractsRoshni ThammaiahNo ratings yet

- Dealership Pricelist Format1 On Road With Accessories Aug-21 - IndividualDocument8 pagesDealership Pricelist Format1 On Road With Accessories Aug-21 - IndividualHrishikesh SwamiNo ratings yet

- Ecom Customer JourneyDocument10 pagesEcom Customer JourneySudip RoyNo ratings yet

- 3 Golden Rules of Accounting ExplainedDocument6 pages3 Golden Rules of Accounting ExplainedYakkstar 21No ratings yet