You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- AE-036411-001 INDEX For Drawing and EquipmentDocument1 pageAE-036411-001 INDEX For Drawing and Equipmentnarutothunderjet216No ratings yet

- How - To - Guide - List - Classic - Cloud - S4 - Solution ManagerDocument11 pagesHow - To - Guide - List - Classic - Cloud - S4 - Solution ManagerEkrem ErdoganNo ratings yet

- Quiz 5Document7 pagesQuiz 5Jud Rossette Arcebes100% (1)

- 5G Technology Training SeriesDocument6 pages5G Technology Training SeriesmirzaNo ratings yet

- Problem 5 Rental IncomeDocument2 pagesProblem 5 Rental IncomeStephen Jay RioNo ratings yet

- 3.2 Commissioner V CADocument8 pages3.2 Commissioner V CAJayNo ratings yet

- Quiroga v. Parsons Hardware Co.Document1 pageQuiroga v. Parsons Hardware Co.Elle MichNo ratings yet

- 01 Assignment CVP Basics AnswerDocument8 pages01 Assignment CVP Basics AnswerKSNo ratings yet

- IS Ready ReckonerDocument6 pagesIS Ready ReckonerRam SundarNo ratings yet

- General Collection CollegeDocument5 pagesGeneral Collection Collegejeysel calumbaNo ratings yet

- Impact A Guide To Business Communication Canadian 9th Edition Northey Solutions ManualDocument11 pagesImpact A Guide To Business Communication Canadian 9th Edition Northey Solutions ManualMarkJoneskjsme100% (13)

- GWD Energy Profile-20230803 v1.3Document25 pagesGWD Energy Profile-20230803 v1.3burim.istrefi87No ratings yet

- Role of Print Media in Creating Awareness About Community IssuesDocument3 pagesRole of Print Media in Creating Awareness About Community Issuesmaneeha amirNo ratings yet

- BRS Review 2020Document64 pagesBRS Review 2020Osman ÖzenNo ratings yet

- HBS Application FormDocument11 pagesHBS Application Formnaveena115No ratings yet

- Procedure To Acquire Data of The Properties in Delhi OnlineDocument4 pagesProcedure To Acquire Data of The Properties in Delhi Onlinesamridhi dobhalNo ratings yet

- Valuation of Early Stage High-Tech Start-Up Companies: Gunter Festel, Martin Wuermseher, Giacomo CattaneoDocument16 pagesValuation of Early Stage High-Tech Start-Up Companies: Gunter Festel, Martin Wuermseher, Giacomo CattaneoSafwen Ben HniniNo ratings yet

- Jcpenney, Inc: A Case Study About The Impact of Rebranding On Internal and External CommunicationDocument5 pagesJcpenney, Inc: A Case Study About The Impact of Rebranding On Internal and External Communicationsibina.ac sibina.aniyachalilNo ratings yet

- Chapter 11Document8 pagesChapter 11yousufmeahNo ratings yet

- Odisha District Mineral Foundations Rules 2015Document7 pagesOdisha District Mineral Foundations Rules 2015Sunny SinghNo ratings yet

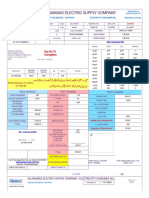

- Iesco Online BillDocument1 pageIesco Online BillRocky BhaiNo ratings yet

- Manual de Derecho Penal Chileno Parte EspecialDocument18 pagesManual de Derecho Penal Chileno Parte EspecialCamila Olguín-Sanhueza0% (1)

- A958A958MDocument5 pagesA958A958MMARCONo ratings yet

- CatalogDocument52 pagesCatalogrcastroroboconperuNo ratings yet

- IRM Quiz 1 QuestionbankDocument7 pagesIRM Quiz 1 Questionbankgnishi2908No ratings yet

- NDA Eng TemplateDocument4 pagesNDA Eng TemplateDenis LambertNo ratings yet

- Pakistan International AirlinesDocument12 pagesPakistan International AirlinesBahawal Shahryar KhanNo ratings yet

- Warehouse Design 2Document33 pagesWarehouse Design 2Truong Diem SuongNo ratings yet

- Mohammed Shahil BBA HR ProjectDocument92 pagesMohammed Shahil BBA HR ProjectskyshahilNo ratings yet

- SGS Textile Sustainability EN 11Document8 pagesSGS Textile Sustainability EN 11Utilities2No ratings yet