You might also like

- ELS - Q1 - Week 6aDocument9 pagesELS - Q1 - Week 6aMahika BatumbakalNo ratings yet

- Las q2 Fabm 2 Week 4Document10 pagesLas q2 Fabm 2 Week 4Mahika BatumbakalNo ratings yet

- LAS Q2 FABM 2 Week 3Document12 pagesLAS Q2 FABM 2 Week 3Mahika BatumbakalNo ratings yet

- StatProb - Q4 - Worksheet No. 3 - Testing Hypothesis On Population ProportionDocument2 pagesStatProb - Q4 - Worksheet No. 3 - Testing Hypothesis On Population ProportionMahika BatumbakalNo ratings yet

- StatProb - Q4 - Worksheet No. 2 - Hypothesis Testing About The Population MeanDocument1 pageStatProb - Q4 - Worksheet No. 2 - Hypothesis Testing About The Population MeanMahika BatumbakalNo ratings yet

- PS Q2 Week-5Document10 pagesPS Q2 Week-5Mahika BatumbakalNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Personal Finance Course. Mock Exam 2021.2022.without AnswerDocument2 pagesPersonal Finance Course. Mock Exam 2021.2022.without AnswerLê TThu HàNo ratings yet

- University of Cambridge International Examinations International General Certificate of Secondary Education Accounting Paper 1 Multiple Choice October/November 2005 1 HourDocument12 pagesUniversity of Cambridge International Examinations International General Certificate of Secondary Education Accounting Paper 1 Multiple Choice October/November 2005 1 HourzeelNo ratings yet

- Consolidated Balance Sheet: As at 31st March, 2021Document2 pagesConsolidated Balance Sheet: As at 31st March, 2021Only For StudyNo ratings yet

- Your Zestmoney AgreementDocument12 pagesYour Zestmoney AgreementPrasanth ParimiNo ratings yet

- This Is FreedomDocument31 pagesThis Is FreedomNurhussein RaopanNo ratings yet

- Domingo vs. GarlitosDocument2 pagesDomingo vs. GarlitosMark Gabriel B. MarangaNo ratings yet

- Assets Book Value Estimated Realizable ValuesDocument3 pagesAssets Book Value Estimated Realizable ValuesEllyza SerranoNo ratings yet

- Far Drill2Document4 pagesFar Drill2Jung Hwan SoNo ratings yet

- Solutions To Exercises - Chapter 17Document6 pagesSolutions To Exercises - Chapter 17Ng. Minh ThảoNo ratings yet

- Credit and Collection ReportDocument14 pagesCredit and Collection ReportCarlos John Talania 1923No ratings yet

- Acknowledgment Receipt: Loan Account Number: 4002038493Document2 pagesAcknowledgment Receipt: Loan Account Number: 4002038493bess0910No ratings yet

- Comparison of Corporation Code and Revised Corporation Code DMDocument150 pagesComparison of Corporation Code and Revised Corporation Code DMArmand Jerome CaradaNo ratings yet

- Strat Cost 8-24Document4 pagesStrat Cost 8-24Vivienne Rozenn LaytoNo ratings yet

- Lesson 1 - Engineering EconomicsDocument14 pagesLesson 1 - Engineering EconomicsGerald Gloriane CallejaNo ratings yet

- Details of The Offer:: "Spend Rs. 1,500 On Domestic E-Commerce Transactions and Get Rs. 250 Cashback" Terms & ConditionsDocument3 pagesDetails of The Offer:: "Spend Rs. 1,500 On Domestic E-Commerce Transactions and Get Rs. 250 Cashback" Terms & ConditionsMohamedNo ratings yet

- Indian Accounting Standard 23 - Borrowing CostDocument10 pagesIndian Accounting Standard 23 - Borrowing CostSonali LadiNo ratings yet

- BofA - The Next Default Cycle Research Report - HY-51472Document17 pagesBofA - The Next Default Cycle Research Report - HY-51472ManeeshNo ratings yet

- Chapter 6 AnnuityDocument62 pagesChapter 6 Annuity2022885126No ratings yet

- Question Test Far560 June 2017 Csofp DragonDocument3 pagesQuestion Test Far560 June 2017 Csofp DragonhdyhNo ratings yet

- Credit ReportDocument10 pagesCredit ReportAubree GatesNo ratings yet

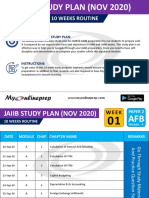

- Jaiib 10 Weeks Study Plan Nov 2020Document11 pagesJaiib 10 Weeks Study Plan Nov 2020Siva BantuNo ratings yet

- Sec-A.T1-100. AnswerDocument83 pagesSec-A.T1-100. AnswermmranaduNo ratings yet

- Abigail Santos Boutique, Worksheet and Financial Statement For MerchandisingDocument9 pagesAbigail Santos Boutique, Worksheet and Financial Statement For MerchandisingFeiya LiuNo ratings yet

- MODULE 5 Part 2.Document5 pagesMODULE 5 Part 2.Charissa Jamis ChingwaNo ratings yet

- Special Power of AttorneyDocument2 pagesSpecial Power of Attorneymiron68No ratings yet

- IA2 Prelim ExamDocument7 pagesIA2 Prelim ExamJohn FloresNo ratings yet

- Ajdpd2330g 2023Document4 pagesAjdpd2330g 2023TAX INDIANo ratings yet

- Engels SEM1 SECONDDocument2 pagesEngels SEM1 SECONDJolien DeceuninckNo ratings yet

- Math 120 - Project 2 - FinanceDocument3 pagesMath 120 - Project 2 - FinanceDouglas M. DougyNo ratings yet

- BL2 LongquizDocument2 pagesBL2 LongquizJanna Mari FriasNo ratings yet