You might also like

- AC 3 - Intermediate Acctg' 1 (Ate Jan Ver)Document119 pagesAC 3 - Intermediate Acctg' 1 (Ate Jan Ver)John Renier Bernardo100% (1)

- Midterm Exam Parcor 2020Document1 pageMidterm Exam Parcor 2020John Alfred CastinoNo ratings yet

- This Study Resource Was: Quiz On Receivable FinancingDocument3 pagesThis Study Resource Was: Quiz On Receivable FinancingKez MaxNo ratings yet

- Partnership DissolutionDocument7 pagesPartnership DissolutionAngel Frolen B. RacinezNo ratings yet

- Microsoft Word - CPAT Reviewer - Law On SalesDocument14 pagesMicrosoft Word - CPAT Reviewer - Law On SaleselaineNo ratings yet

- Chapter 8 Quiz - InventoriesDocument8 pagesChapter 8 Quiz - InventoriesDarleen CantiladoNo ratings yet

- PARCOR - 3Partnership-OperationsDocument31 pagesPARCOR - 3Partnership-OperationsHarriane Mae GonzalesNo ratings yet

- Pas 37 38 40 41 PFRS 1Document5 pagesPas 37 38 40 41 PFRS 1LALALA LULULUNo ratings yet

- Warren's Sporting Goods Rework CostDocument1 pageWarren's Sporting Goods Rework CostWendelyn LingayuNo ratings yet

- Bsa Online Quiz 1 - Overview of AccountingDocument9 pagesBsa Online Quiz 1 - Overview of AccountingRyzeNo ratings yet

- FM 1 Assignment 1Document3 pagesFM 1 Assignment 1Jelly Ann AndresNo ratings yet

- E. Biological AssetsDocument1 pageE. Biological AssetsDerick Ocampo FulgencioNo ratings yet

- 4 - Lecture Notes - Partnership DissolutionDocument18 pages4 - Lecture Notes - Partnership DissolutionNikko Bowie PascualNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- Phunky Phingers Cost ReportsDocument5 pagesPhunky Phingers Cost Reportsruqayya muhammedNo ratings yet

- Quiz Chapter-2 Partnership-Operations 2020-EditionDocument7 pagesQuiz Chapter-2 Partnership-Operations 2020-EditionShaz NagaNo ratings yet

- IC On Petty Cash KeyDocument2 pagesIC On Petty Cash KeyLorie RoncalNo ratings yet

- 9201 - Partnership FormationDocument4 pages9201 - Partnership FormationBrian Dave OrtizNo ratings yet

- Accounting For Special TransactionsDocument43 pagesAccounting For Special TransactionsNezer VergaraNo ratings yet

- CASE 1: PM Company: Total Current Asset 1,750,000Document3 pagesCASE 1: PM Company: Total Current Asset 1,750,000JanineD.MeranioNo ratings yet

- Final Exam Far1Document4 pagesFinal Exam Far1Chloe CatalunaNo ratings yet

- CFAS Notes Chapter 2 Conceptual FrameworkDocument3 pagesCFAS Notes Chapter 2 Conceptual FrameworkUyara LeisbergNo ratings yet

- Farparcor 2 Chapter 1 Exercises Problem AnswersDocument10 pagesFarparcor 2 Chapter 1 Exercises Problem AnswersWillnie Shane LabaroNo ratings yet

- Quiz in Intacc 1 & 2 (Finals)Document1 pageQuiz in Intacc 1 & 2 (Finals)Sandra100% (1)

- Straight Problems Income Tax Bsa2Document2 pagesStraight Problems Income Tax Bsa2dimpy dNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument6 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionAIENNA GABRIELLE FABRO100% (1)

- Philippine Equity Contributed Problems SolutionsDocument4 pagesPhilippine Equity Contributed Problems SolutionsTatianaNo ratings yet

- Assets: Pedro Castro Statement of Financial Position October 1, 2016Document2 pagesAssets: Pedro Castro Statement of Financial Position October 1, 2016Mandy Bloom0% (1)

- Quiz On Partnership LiquidationDocument4 pagesQuiz On Partnership LiquidationTrisha Mae AlburoNo ratings yet

- AFAR-07 (Home-Office & Branch Accounting)Document7 pagesAFAR-07 (Home-Office & Branch Accounting)mysweet surrenderNo ratings yet

- Franchising Consignment KeyDocument22 pagesFranchising Consignment KeyMichael Jay SantosNo ratings yet

- Acct-111e - Quiz CompDocument18 pagesAcct-111e - Quiz CompJap Keren LirazanNo ratings yet

- Quiz On Partnership FormationDocument2 pagesQuiz On Partnership FormationVher Christopher DucayNo ratings yet

- A Business, Such As A Partnership, As To File Its Partnership Agreement and Register Its Firm's Name With These Government Agencies, Except OneDocument1 pageA Business, Such As A Partnership, As To File Its Partnership Agreement and Register Its Firm's Name With These Government Agencies, Except OneJAHNHANNALEI MARTICIONo ratings yet

- 6937 - Statement of Cash FlowsDocument2 pages6937 - Statement of Cash FlowsAljur SalamedaNo ratings yet

- StalasaDocument23 pagesStalasajessa mae zerdaNo ratings yet

- Exercises Ppe PDFDocument6 pagesExercises Ppe PDFمعن الفاعوري100% (1)

- Toaz - Info Quiz 3 PRDocument25 pagesToaz - Info Quiz 3 PRAprille Xay TupasNo ratings yet

- Solution Chapter 14Document26 pagesSolution Chapter 14grace guiuanNo ratings yet

- Home Office & Branch Accounting Problems SolvedDocument3 pagesHome Office & Branch Accounting Problems SolvedChristianAquinoNo ratings yet

- Requirement: A New Set of Books Will Be Opened by The Partnership Roces' Books Sales' BooksDocument7 pagesRequirement: A New Set of Books Will Be Opened by The Partnership Roces' Books Sales' BooksJunzen Ralph YapNo ratings yet

- Repealed PD 692 Known As Revised Accountancy LawDocument8 pagesRepealed PD 692 Known As Revised Accountancy LawLian RamirezNo ratings yet

- Wasting Assets Impairment of AssetsDocument14 pagesWasting Assets Impairment of AssetsJohn Ferd M. FerminNo ratings yet

- Advanced Accounting Part 1 Quiz SolutionsDocument20 pagesAdvanced Accounting Part 1 Quiz SolutionsNikki GarciaNo ratings yet

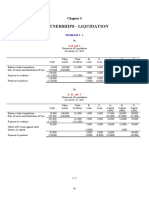

- Partnerships - Liquidation: Problem 3 - 1Document20 pagesPartnerships - Liquidation: Problem 3 - 1marieieiemNo ratings yet

- (Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 1 (Partnership) - Answers On Multiple Choice Computation #21 To 25Document1 page(Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 1 (Partnership) - Answers On Multiple Choice Computation #21 To 25John Carlos DoringoNo ratings yet

- Partnership FormationDocument3 pagesPartnership FormationJules AguilarNo ratings yet

- CfasDocument32 pagesCfasLouiseNo ratings yet

- Chapter 4 Dissolution Q A Final Chapter 4 Dissolution Q A FinalDocument26 pagesChapter 4 Dissolution Q A Final Chapter 4 Dissolution Q A Finalrandom17341No ratings yet

- Problems 3 PRELIM TASK FINALDocument4 pagesProblems 3 PRELIM TASK FINALJohn Francis RosasNo ratings yet

- Partnership Dissolution: QuizDocument5 pagesPartnership Dissolution: QuizLee SuarezNo ratings yet

- Partnership DissolutionDocument5 pagesPartnership DissolutionKathleenNo ratings yet

- Oblicon ReviewerDocument110 pagesOblicon ReviewerThe ApprenticeNo ratings yet

- Midterm Exam Accntg For Special TransactionsDocument8 pagesMidterm Exam Accntg For Special TransactionsJustine Flores100% (1)

- Assignment On Partnership DissolutionDocument2 pagesAssignment On Partnership DissolutionGhillian Mae Guiang100% (1)

- Ae12 Course File Econ DevDocument49 pagesAe12 Course File Econ DevEki OmallaoNo ratings yet

- Pre FinactDocument6 pagesPre FinactMenardNo ratings yet

- Partnership Formation and Capital Adjustment CasesDocument3 pagesPartnership Formation and Capital Adjustment CasesAlfred DalaganNo ratings yet

- ReviewerDocument15 pagesReviewerALMA MORENANo ratings yet

- Forming a Partnership with Cash and LandDocument2 pagesForming a Partnership with Cash and LandArian AmuraoNo ratings yet

- Outsourcing. The Concept: June 2012Document9 pagesOutsourcing. The Concept: June 2012sayaliNo ratings yet

- Dominance of MNCsDocument11 pagesDominance of MNCssuchitaNo ratings yet

- StitchDocument10 pagesStitchSherouk Eid100% (1)

- Students' creative writing and language skills benefit more from reading books than online newspapersDocument36 pagesStudents' creative writing and language skills benefit more from reading books than online newspapersTrần NgọcNo ratings yet

- Price PatternsDocument40 pagesPrice PatternsHimadieNo ratings yet

- Sample Techsheet ReadulDocument2 pagesSample Techsheet Readulimportantdocs1542No ratings yet

- V-Belts and Pulleys Design GuideDocument2 pagesV-Belts and Pulleys Design GuideLurking RogueNo ratings yet

- Admission of A PartnerDocument5 pagesAdmission of A PartnerHigreeve SrudhiNo ratings yet

- Find Question 4Document2 pagesFind Question 4hasgonde123No ratings yet

- 382 1458 1 PBDocument11 pages382 1458 1 PBDaniela DanaNo ratings yet

- AoSUM Program - FINALDocument5 pagesAoSUM Program - FINALSofia CornelioNo ratings yet

- FSAV 6e - Errata 092022Document28 pagesFSAV 6e - Errata 092022Aruzhan TanirbergenNo ratings yet

- 30-April-2021 Weekly UpdateDocument11 pages30-April-2021 Weekly UpdateShamraiz KhanNo ratings yet

- Direct Demand FunctionsDocument5 pagesDirect Demand FunctionsLagopNo ratings yet

- Soft Furnishing SpecsDocument11 pagesSoft Furnishing SpecsMiguel EllaNo ratings yet

- Explaining How The Absence of Non-White Individuals in Workplace Environments Increases Production Output: "White Synergy" Revisited. 2018Document6 pagesExplaining How The Absence of Non-White Individuals in Workplace Environments Increases Production Output: "White Synergy" Revisited. 2018Anonymous h8Wfzl0% (1)

- Preparing Cash Flow StatementsDocument4 pagesPreparing Cash Flow StatementsCindy Lota100% (1)

- NEGOTIATION IMPROVEMENTDocument5 pagesNEGOTIATION IMPROVEMENTAyda KhadivaNo ratings yet

- Strictly Confidential: (For Internal and Restricted Use Only)Document27 pagesStrictly Confidential: (For Internal and Restricted Use Only)bhaiyarakeshNo ratings yet

- CPC Manual: Ethiopian Customs CommissionDocument45 pagesCPC Manual: Ethiopian Customs CommissionTessema Alemu100% (2)

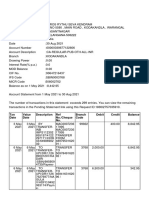

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument40 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balance184H0 Yellu Anusha VCENo ratings yet

- I-Byte Resources July 2021Document65 pagesI-Byte Resources July 2021IT ShadesNo ratings yet

- U3 Regional Integration & Trade ArrangementsDocument40 pagesU3 Regional Integration & Trade ArrangementsArun MishraNo ratings yet

- Angeline Tham - AngkasDocument2 pagesAngeline Tham - AngkasDaniella YbutNo ratings yet

- Mixture Part 5Document9 pagesMixture Part 5mehedee129No ratings yet

- Aims Annual Report 2020Document122 pagesAims Annual Report 2020Felicia IvenaNo ratings yet

- My - Statement - 01 Jul, 2023 - 09 Jul, 2023 - 8050668560Document13 pagesMy - Statement - 01 Jul, 2023 - 09 Jul, 2023 - 8050668560The HulkNo ratings yet

- Brother BAS-311E, ELDocument123 pagesBrother BAS-311E, ELAgnaldo VanzuitaNo ratings yet

- Bill of Quantity - Replacement of Roofing & CeilingDocument2 pagesBill of Quantity - Replacement of Roofing & CeilingEdwin FranciscoNo ratings yet

- SAILDocument17 pagesSAILnareshNo ratings yet