You might also like

- Procurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesFrom EverandProcurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesNo ratings yet

- CERC Guidelines On Capital Cost For Transmission SystemDocument34 pagesCERC Guidelines On Capital Cost For Transmission Systemrahulmangalca9997No ratings yet

- Effect Study Ifric13 enDocument21 pagesEffect Study Ifric13 enFiras AbsaNo ratings yet

- Via Email:: Rule-Comments@sec - GovDocument25 pagesVia Email:: Rule-Comments@sec - GovMarketsWikiNo ratings yet

- Some Economics of Audit Market Reform: Boon Seng Tan, Yew Kee HoDocument13 pagesSome Economics of Audit Market Reform: Boon Seng Tan, Yew Kee HoElena DobreNo ratings yet

- Information Sheet: Overview of The Balancing and Settlement Code (BSC) ArrangementsDocument3 pagesInformation Sheet: Overview of The Balancing and Settlement Code (BSC) ArrangementsJana TufegdzicNo ratings yet

- Regulatory Assets and LiabilitiesDocument5 pagesRegulatory Assets and LiabilitiesMatthew Dickerson100% (1)

- 30 20120709 Roaming Regulation Choice of Decoupling CPDocument72 pages30 20120709 Roaming Regulation Choice of Decoupling CPDanish HashmiNo ratings yet

- Statement of Position 81-1Document34 pagesStatement of Position 81-1Vikas RalhanNo ratings yet

- Case Histories 2015Document43 pagesCase Histories 2015api-315973904No ratings yet

- Fsa cp10 28Document98 pagesFsa cp10 28Sling ShotNo ratings yet

- 2005 Business ManagementDocument11 pages2005 Business ManagementMikus CirulisNo ratings yet

- Profitability Methodology Approach Working Paper - MRNDocument27 pagesProfitability Methodology Approach Working Paper - MRNpotsestella36No ratings yet

- Guidance on Standard e-Tender Document e-PW3Document6 pagesGuidance on Standard e-Tender Document e-PW3abir ratulNo ratings yet

- MAHARASHTRA ELECTRICITY REGULATORY COMMISSION Guidelines For In-Principle Clearance of Proposed Investment Schemes.Document8 pagesMAHARASHTRA ELECTRICITY REGULATORY COMMISSION Guidelines For In-Principle Clearance of Proposed Investment Schemes.Suntech SolarNo ratings yet

- Platforms: Delivering The RDR and Other Issues For Platforms and Nominee-Related ServicesDocument73 pagesPlatforms: Delivering The RDR and Other Issues For Platforms and Nominee-Related ServicesMarketsWikiNo ratings yet

- Benchmark Capital Cost For TPSDocument27 pagesBenchmark Capital Cost For TPSdipenkhandhediyaNo ratings yet

- Enforcing The Digital Markets Act - 1Document41 pagesEnforcing The Digital Markets Act - 1Competition Policy & LawNo ratings yet

- Weighted Average Cost of Capital: Confidential and Legally PrivilegedDocument15 pagesWeighted Average Cost of Capital: Confidential and Legally PrivilegedBet RomanNo ratings yet

- Port+Harcourt+DisCo+Rate+Case+Application July+2023Document3 pagesPort+Harcourt+DisCo+Rate+Case+Application July+2023Ibitola AbayomiNo ratings yet

- IASB Exposure Draft Operational EffectsDocument10 pagesIASB Exposure Draft Operational EffectsMESPERANANo ratings yet

- Welcome To The IFRIC UpdateDocument9 pagesWelcome To The IFRIC UpdateGiancarlo BarredaNo ratings yet

- GOV Competition in Onshore Electricity Networks Consultation ResponseDocument53 pagesGOV Competition in Onshore Electricity Networks Consultation Responsebog.creeperaNo ratings yet

- Recocimiento de Ingresos - MediaDocument8 pagesRecocimiento de Ingresos - MediaEY VenezuelaNo ratings yet

- Know Before You Owe Mortgage Loan InitiativeDocument19 pagesKnow Before You Owe Mortgage Loan InitiativeLori NobleNo ratings yet

- Technical LineDocument27 pagesTechnical LinemalisevicNo ratings yet

- Valuation MethodDocument3 pagesValuation MethodviganjorebicNo ratings yet

- January 2005 6-1 6-101: Local Governments, and Non-Profit OrganizationsDocument31 pagesJanuary 2005 6-1 6-101: Local Governments, and Non-Profit OrganizationsDoxCak3No ratings yet

- Current Cost Accounting Report - July-Dec 2010 (Issued May 2010)Document14 pagesCurrent Cost Accounting Report - July-Dec 2010 (Issued May 2010)Taymur WafiNo ratings yet

- Deloitte VertDocument28 pagesDeloitte VertThoaNo ratings yet

- Mini CompDocument4 pagesMini CompVinox KusumaNo ratings yet

- Telecom Regulatory Authority of India: Consultation Paper On Validity Period of Tariff OffersDocument9 pagesTelecom Regulatory Authority of India: Consultation Paper On Validity Period of Tariff Offersmitul yadavNo ratings yet

- Before The Federal Communications Commission Washington, D.C. 20554Document32 pagesBefore The Federal Communications Commission Washington, D.C. 20554Sameen RizviNo ratings yet

- WindEurope Response To ACER ConsultationDocument10 pagesWindEurope Response To ACER ConsultationGerard PoncinNo ratings yet

- Reporting on Audited Financial StatementsDocument16 pagesReporting on Audited Financial StatementsAndrecarvalho97No ratings yet

- Cable and Wireless Vs IBMDocument10 pagesCable and Wireless Vs IBMPratik BakshiNo ratings yet

- Economic Analysis of The Specific Proposal: 8.1 PurposeDocument14 pagesEconomic Analysis of The Specific Proposal: 8.1 PurposevasucristalNo ratings yet

- Regulatory Implementation of The Statement of Principles Regarding The Activities of Credit Rating AgenciesDocument38 pagesRegulatory Implementation of The Statement of Principles Regarding The Activities of Credit Rating AgenciesChou ChantraNo ratings yet

- ADB Warehouse FinancingDocument40 pagesADB Warehouse Financingradakan298No ratings yet

- 2018 09 26 10 57 52 ePW3Document104 pages2018 09 26 10 57 52 ePW3Abu Shahadat Muhammad SayeemNo ratings yet

- Analyzing The Relationship Between Regulation and Investment in The Telecom SectorDocument36 pagesAnalyzing The Relationship Between Regulation and Investment in The Telecom SectorGaurab SharmaNo ratings yet

- OFCOM Annual Plan 2007-2008Document42 pagesOFCOM Annual Plan 2007-2008pendleradio99No ratings yet

- Questions and Ansers in Public ProcurementDocument80 pagesQuestions and Ansers in Public ProcurementapmegremisNo ratings yet

- Master-Builders-Review-of-Best-Practice-Principles-February-2021Document4 pagesMaster-Builders-Review-of-Best-Practice-Principles-February-2021jamie.seeto.87No ratings yet

- Cost of Capital AnalysisDocument26 pagesCost of Capital AnalysisSanjeev SanjayNo ratings yet

- B Weighted Average Cost of Capital (WACC)Document36 pagesB Weighted Average Cost of Capital (WACC)IshanSaneNo ratings yet

- Full Business Case FBC TemplateDocument7 pagesFull Business Case FBC Templatebrengle diversified ltdNo ratings yet

- NERA Electricity Tariff Structure PDFDocument129 pagesNERA Electricity Tariff Structure PDFsheetalNo ratings yet

- Week 9 Final AssignmentssDocument11 pagesWeek 9 Final AssignmentssKan SonNo ratings yet

- Clarifying EOI requirements for real-time monitoring and audit of telecom service qualityDocument9 pagesClarifying EOI requirements for real-time monitoring and audit of telecom service qualitySelvaraj KalimuthuNo ratings yet

- Final_CP-Response-Report-_Clean_260923 (1)Document19 pagesFinal_CP-Response-Report-_Clean_260923 (1)harold.chenNo ratings yet

- PIBs Accounting Separation 2002Document11 pagesPIBs Accounting Separation 2002AirfikiNo ratings yet

- Correlacion EBOPS CPCDocument11 pagesCorrelacion EBOPS CPCMara GomezNo ratings yet

- Online Infringement of Copyright and The Digital Economy Act 2010 Published June 26 2012Document129 pagesOnline Infringement of Copyright and The Digital Economy Act 2010 Published June 26 2012TheGift73No ratings yet

- VULA Margin Draft StatementDocument282 pagesVULA Margin Draft StatementalabamafatNo ratings yet

- EITF - Issue16C - Summary1 - 12september2016 EyDocument35 pagesEITF - Issue16C - Summary1 - 12september2016 EyŞtefan AlinNo ratings yet

- Uae Corporate Tax Transfer Pricing GuideDocument7 pagesUae Corporate Tax Transfer Pricing GuideMuhammad UmarNo ratings yet

- Outsourcing of Core Legal Service Functions: How to Capitalise on Opportunities for Law FirmsFrom EverandOutsourcing of Core Legal Service Functions: How to Capitalise on Opportunities for Law FirmsNo ratings yet

- Irregularities, Frauds and the Necessity of Technical Auditing in Construction IndustryFrom EverandIrregularities, Frauds and the Necessity of Technical Auditing in Construction IndustryNo ratings yet

- Gans Stern (2003) - The Product Market and The Market For Ideas Commercialization Strategies For Technology EntrepreneursDocument18 pagesGans Stern (2003) - The Product Market and The Market For Ideas Commercialization Strategies For Technology EntrepreneursdadaisgreatNo ratings yet

- BCGDocument36 pagesBCGdadaisgreat100% (1)

- M&A ShilaDocument5 pagesM&A ShiladadaisgreatNo ratings yet

- Dummy FileDocument1 pageDummy FiledadaisgreatNo ratings yet

- Federal Reserve System ExplainedDocument2 pagesFederal Reserve System ExplainedNishil ShahNo ratings yet

- CFA Level I FormulaSheetDocument12 pagesCFA Level I FormulaSheetthomas94joseph100% (3)

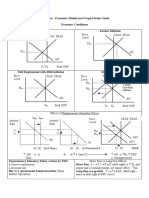

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideGabriel Jimenez100% (7)

- Written Assignment Unit 5Document5 pagesWritten Assignment Unit 5Mandella HarveyNo ratings yet

- TCS Placement Paper, General C Aptitude QuestionsDocument566 pagesTCS Placement Paper, General C Aptitude QuestionsPulkit Mohan67% (3)

- Reporte de The Boston Consulting Group Sobre El PerúDocument44 pagesReporte de The Boston Consulting Group Sobre El PerúAlejandro Castro BackusNo ratings yet

- National Housing Bank Annual Report 2010-2011Document101 pagesNational Housing Bank Annual Report 2010-2011Micheal JacksonNo ratings yet

- Financial Times (UK Edition) No. 41,380 (20 Jul 2023)Document24 pagesFinancial Times (UK Edition) No. 41,380 (20 Jul 2023)mariuscsmNo ratings yet

- CurrentDocument120 pagesCurrentthestark324No ratings yet

- Ico Truebit VitalikDocument21 pagesIco Truebit VitalikAshish RpNo ratings yet

- Importance of Central Banks for Currency StabilityDocument1 pageImportance of Central Banks for Currency StabilitylutfiNo ratings yet

- Interest Rate Spread On Bank Profitability: The Case of Ghanaian BanksDocument12 pagesInterest Rate Spread On Bank Profitability: The Case of Ghanaian BanksKiller BrothersNo ratings yet

- The Economist (20210417) - CalibreDocument226 pagesThe Economist (20210417) - CalibreMd. Sazzad HossainNo ratings yet

- Current Assets Management and FinancialDocument13 pagesCurrent Assets Management and FinancialShemu PlcNo ratings yet

- The Deficit Myth: Modern Monetary Theory and The Birth of The People's EconomyDocument20 pagesThe Deficit Myth: Modern Monetary Theory and The Birth of The People's EconomyjacintoNo ratings yet

- Inflation Rate, Foreign Direct Investment, Interest Rate, and Economic Growth in Sub Sahara Africa Evidence From Emerging NationsDocument8 pagesInflation Rate, Foreign Direct Investment, Interest Rate, and Economic Growth in Sub Sahara Africa Evidence From Emerging NationsEditor IJTSRDNo ratings yet

- Grade 8 2ndterm Revision Sheets2023-2024Document33 pagesGrade 8 2ndterm Revision Sheets2023-2024hyy54841No ratings yet

- Lecture of Mishkin CH 01Document31 pagesLecture of Mishkin CH 01Phuoc DangNo ratings yet

- International Banking and Foreign Exchnage ManagementDocument6 pagesInternational Banking and Foreign Exchnage ManagementPrashant AhujaNo ratings yet

- How To Make Pakistan Future BrightDocument12 pagesHow To Make Pakistan Future BrightJunaid JamshaidNo ratings yet

- PRM1 - Assignment 2Document16 pagesPRM1 - Assignment 2Dawn SimNo ratings yet

- A Primer on Money, Banking, and GoldDocument8 pagesA Primer on Money, Banking, and Goldad9292No ratings yet

- Noon ProjectDocument11 pagesNoon ProjectUbl HrNo ratings yet

- Universal FM CaseDocument6 pagesUniversal FM Casekiller drama100% (1)

- Week 2 NewDocument54 pagesWeek 2 NewKemale ZamanliNo ratings yet

- Term Paper Poverty in Pakistan 2006Document42 pagesTerm Paper Poverty in Pakistan 2006muhammadtaimoorkhan100% (5)

- A Debate About Prohibition ofDocument3 pagesA Debate About Prohibition ofLance Kelly P. ManlangitNo ratings yet

- Sessions 9 and 10 - Investment - Money Demand and SupplyDocument103 pagesSessions 9 and 10 - Investment - Money Demand and SupplyAbhay SahuNo ratings yet

- Melakuu AbebeDocument26 pagesMelakuu AbebemelemengistNo ratings yet