You might also like

- REVIEWERDocument12 pagesREVIEWEREva Mae LabardaNo ratings yet

- Solution Manual For Financial Accounting An Integrated Approach 6th Edition by TrotmanDocument34 pagesSolution Manual For Financial Accounting An Integrated Approach 6th Edition by Trotmana540142314100% (2)

- FABM 1 NotesDocument6 pagesFABM 1 Noteshiraeth.naharaNo ratings yet

- External Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesDocument8 pagesExternal Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesAizel AlindoyNo ratings yet

- Introduction To AccountancyDocument8 pagesIntroduction To Accountancyjo jo paopNo ratings yet

- What is Accounting? The Complete GuideDocument12 pagesWhat is Accounting? The Complete GuideJustin MarshallNo ratings yet

- Solution Manual For Financial Accounting An Integrated Approach 5th Edition by TrotmanDocument21 pagesSolution Manual For Financial Accounting An Integrated Approach 5th Edition by Trotmana540142314No ratings yet

- Fundamentals of AccountingDocument26 pagesFundamentals of AccountingSofia Naraine OnilongoNo ratings yet

- Accounting For Lawyers by Solicitor KatuDocument45 pagesAccounting For Lawyers by Solicitor KatuFrancisco Hagai GeorgeNo ratings yet

- Copyofcopy3ofapresentation 150501110626 Conversion Gate01Document11 pagesCopyofcopy3ofapresentation 150501110626 Conversion Gate01Gian LawrenceNo ratings yet

- Chapter 2 - Key Accounting ConceptsDocument5 pagesChapter 2 - Key Accounting ConceptsAlex EiyzNo ratings yet

- Reviewer For AccountingDocument7 pagesReviewer For AccountingRoesell Anne EspeletaNo ratings yet

- CMA Volume IDocument432 pagesCMA Volume IEthan HuntNo ratings yet

- Chapter 1 (1) NowteyDocument8 pagesChapter 1 (1) NowteyAkkamaNo ratings yet

- Midterm Exam (Reviewer)Document84 pagesMidterm Exam (Reviewer)Mj PamintuanNo ratings yet

- ACM Unit 1Document65 pagesACM Unit 1Aritra DeyNo ratings yet

- Bookkeeping Lesson EditedDocument23 pagesBookkeeping Lesson EditedLu CioNo ratings yet

- IFA Chapter 1Document12 pagesIFA Chapter 1Suleyman TesfayeNo ratings yet

- 1.1 IntroductionDocument11 pages1.1 IntroductionKISAKYE MOSESNo ratings yet

- Lecture #1Document29 pagesLecture #1Nicole AngodungNo ratings yet

- CH01-Fundamentals of Accounting Haftom1 AccountingDocument68 pagesCH01-Fundamentals of Accounting Haftom1 AccountingHaftom YitbarekNo ratings yet

- Muh213U-Accounting I: Chapter 1: Accounting and Business EnvironmentDocument21 pagesMuh213U-Accounting I: Chapter 1: Accounting and Business EnvironmentÖmer Faruk AYDINNo ratings yet

- Lesson 1 - Definitions J Concepts and Qualitative CharacteristicsDocument11 pagesLesson 1 - Definitions J Concepts and Qualitative Characteristicschembejosephine40No ratings yet

- Financial Accounting and ReportingDocument8 pagesFinancial Accounting and ReportingJulieta Bucod CutarraNo ratings yet

- Lecture - 1 - Accounting - in - Business - NUS ACC1002 2020 Spring PostDocument42 pagesLecture - 1 - Accounting - in - Business - NUS ACC1002 2020 Spring PostZenyui100% (1)

- Introduction To Financial AccountingDocument19 pagesIntroduction To Financial AccountingRONALD SSEKYANZINo ratings yet

- Auditing Reviewer1Document23 pagesAuditing Reviewer1Lovely Rose ArpiaNo ratings yet

- Modules 1Document4 pagesModules 1JT GalNo ratings yet

- Chap 2 - SFARDocument6 pagesChap 2 - SFARApril Joy ObedozaNo ratings yet

- Financial Accounting OverviewDocument30 pagesFinancial Accounting OverviewMOHD SYUKRI BIN ABDUL WAHAB STUDENTNo ratings yet

- Elements of Financial StatementDocument33 pagesElements of Financial StatementKertik Singh100% (1)

- B203B-Week 4 - (Accounting-1)Document11 pagesB203B-Week 4 - (Accounting-1)ahmed helmyNo ratings yet

- Lecture Basic ConsiderationsDocument4 pagesLecture Basic ConsiderationsAdelina AquinoNo ratings yet

- FA FOR BADM Unit 2Document17 pagesFA FOR BADM Unit 2GUDATA ABARANo ratings yet

- Company Management. The Management Team Needs To Understand TheDocument3 pagesCompany Management. The Management Team Needs To Understand TheGopali AoshieaneNo ratings yet

- Test 1Document4 pagesTest 1Leslie CarrollNo ratings yet

- Accounting:: Information For Decision MakingDocument29 pagesAccounting:: Information For Decision MakingKhursheed Ahmad KhanNo ratings yet

- Notes 1: "Accounting Is The Language of Business."Document4 pagesNotes 1: "Accounting Is The Language of Business."Krissha GalonNo ratings yet

- Chapter One: Accounting Practice and PrinciplesDocument16 pagesChapter One: Accounting Practice and PrinciplesTesfamlak MulatuNo ratings yet

- FabmDocument7 pagesFabmRYLE MEGAN CARRANZONo ratings yet

- LESSON 6 Accounting Concepts and PrinciplesDocument5 pagesLESSON 6 Accounting Concepts and PrinciplesUnamadable UnleomarableNo ratings yet

- Accounting Week 3Document11 pagesAccounting Week 3janeNo ratings yet

- Understanding The Entity and Its EnvironmentDocument15 pagesUnderstanding The Entity and Its EnvironmentClarissa Micah VillanuevaNo ratings yet

- Managerial Accounting - NotesDocument14 pagesManagerial Accounting - NotesMary Joanne PatolilicNo ratings yet

- Auditing Theo Intro of AuditingDocument39 pagesAuditing Theo Intro of AuditingVain nielNo ratings yet

- CFAS Easy To Learn (Conceptual Framework)Document61 pagesCFAS Easy To Learn (Conceptual Framework)Borg Camlan100% (1)

- Financial Accounting: by - Prof. Gazia SayedDocument44 pagesFinancial Accounting: by - Prof. Gazia SayedAyushi KavthankarNo ratings yet

- Chapter 2 - The Conceptual FrameworkDocument5 pagesChapter 2 - The Conceptual FrameworkdiditayumeganNo ratings yet

- Corporate ReportingDocument20 pagesCorporate Reportingay nnNo ratings yet

- Chapter 5 Principls and ConceptsDocument10 pagesChapter 5 Principls and ConceptsawlachewNo ratings yet

- Week 1 AccDocument24 pagesWeek 1 AccLawrence MosizaNo ratings yet

- Conceptual Framework - 0Document9 pagesConceptual Framework - 0alabaaleahmarieNo ratings yet

- Accounting FundamentalsDocument27 pagesAccounting FundamentalsMarta MeaNo ratings yet

- Chapter-1 Introduction To Accounting and BusinessDocument17 pagesChapter-1 Introduction To Accounting and BusinessTsegaye Belay100% (1)

- IASB Conceptual Framework for Financial AccountingDocument9 pagesIASB Conceptual Framework for Financial AccountingAmelia TaylorNo ratings yet

- Framework For The Preparation and Presentation of The Financial StatementsDocument28 pagesFramework For The Preparation and Presentation of The Financial StatementsTin ManaogNo ratings yet

- Introduction To AccountingDocument6 pagesIntroduction To AccountingNicole_Gella_G_1555No ratings yet

- BAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryDocument111 pagesBAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryWachirajaneNo ratings yet

- Module 3 Conceptual Frameworks and Accounting StandardsDocument10 pagesModule 3 Conceptual Frameworks and Accounting StandardsJonabelle DalesNo ratings yet

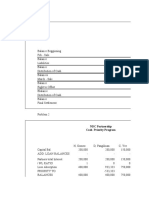

- Trial Balance: Meriel and Sienna CompanyDocument1 pageTrial Balance: Meriel and Sienna Companyreagan blaireNo ratings yet

- Activity Inventory Estimation and Biological AssetsDocument4 pagesActivity Inventory Estimation and Biological Assetsreagan blaireNo ratings yet

- Quiz Notes and Loans Receivable SY 2022 2023 SolutionDocument4 pagesQuiz Notes and Loans Receivable SY 2022 2023 Solutionreagan blaireNo ratings yet

- Assignment Partnership Installment LiquidationDocument3 pagesAssignment Partnership Installment Liquidationreagan blaireNo ratings yet

- Vendor Contact List: Meriel and Sienna CompanyDocument1 pageVendor Contact List: Meriel and Sienna Companyreagan blaireNo ratings yet

- VAT Is Under Business TaxationDocument5 pagesVAT Is Under Business Taxationreagan blaireNo ratings yet

- History and Classifications of Philippine Folk DanceDocument2 pagesHistory and Classifications of Philippine Folk Dancereagan blaireNo ratings yet

- Uitf Offsite Exam Reminders.Document29 pagesUitf Offsite Exam Reminders.reagan blaireNo ratings yet

- Customer Balance Summary: Meriel and Sienna CompanyDocument1 pageCustomer Balance Summary: Meriel and Sienna Companyreagan blaireNo ratings yet

- Steve JobsDocument1 pageSteve Jobsreagan blaireNo ratings yet

- Conceptual FrameworkDocument1 pageConceptual Frameworkreagan blaireNo ratings yet

- Special Journals and Voucher SystemDocument8 pagesSpecial Journals and Voucher Systemreagan blaireNo ratings yet

- Long-distance love, betrayal and finding faithDocument2 pagesLong-distance love, betrayal and finding faithreagan blaireNo ratings yet

- Economic DevelopmentDocument1 pageEconomic Developmentreagan blaireNo ratings yet

- Managerial Science Bayes TheoremDocument3 pagesManagerial Science Bayes Theoremreagan blaireNo ratings yet

- Cbs 1Document1 pageCbs 1reagan blaireNo ratings yet

- Partnership FormationDocument22 pagesPartnership Formationreagan blaireNo ratings yet

- Underwrite WDocument1 pageUnderwrite Wreagan blaireNo ratings yet

- Book 1Document3 pagesBook 1reagan blaireNo ratings yet

- Auq NaDocument5 pagesAuq Nareagan blaireNo ratings yet

- Value Chain Analysis and Five Force AnalysisDocument22 pagesValue Chain Analysis and Five Force Analysisreagan blaireNo ratings yet

- Comprehensive Guide to Basic AccountingDocument27 pagesComprehensive Guide to Basic Accountingreagan blaireNo ratings yet

- Cost Accounting Cost Behavior AssignmentDocument3 pagesCost Accounting Cost Behavior Assignmentreagan blaireNo ratings yet

- Cost Accounting Assignment Correlation AnalysisDocument14 pagesCost Accounting Assignment Correlation Analysisreagan blaireNo ratings yet

- Managerial Econ QuzzizDocument3 pagesManagerial Econ Quzzizreagan blaireNo ratings yet

- 11Document1 page11reagan blaireNo ratings yet

- Economic Development, Artesano 1Document1 pageEconomic Development, Artesano 1reagan blaireNo ratings yet

- Me Unfinished NotesDocument9 pagesMe Unfinished Notesreagan blaireNo ratings yet

- Schedule appointments easilyDocument2 pagesSchedule appointments easilyreagan blaireNo ratings yet

- Financial ControllershipDocument7 pagesFinancial ControllershipKaye LaborteNo ratings yet

- Cwopa Sers Comprehensive Annual Financial Report 2003Document96 pagesCwopa Sers Comprehensive Annual Financial Report 2003EHNo ratings yet

- Hotel Internal Audit - Hotel Human ResourcesDocument50 pagesHotel Internal Audit - Hotel Human Resourcesmahmut yıldırımNo ratings yet

- Revised-Tarmizi-Materi Rapat Kerja Forum Spi PTNBHDocument16 pagesRevised-Tarmizi-Materi Rapat Kerja Forum Spi PTNBHhanifaNo ratings yet

- Audit Report - TuburanDocument87 pagesAudit Report - TuburanMaria100% (1)

- Governance Report 2021Document20 pagesGovernance Report 2021Raul De La CruzNo ratings yet

- Financial Accounting Auditing - Paper V PDFDocument335 pagesFinancial Accounting Auditing - Paper V PDFRaju P VishwakarmaNo ratings yet

- Maintenance Training Organisation Approval: - UncontrolledDocument38 pagesMaintenance Training Organisation Approval: - UncontrolledAmwaras HelimalayaNo ratings yet

- Booklet Sterility AssuranceDocument33 pagesBooklet Sterility AssurancesukohomaNo ratings yet

- AT-06 (FS Audit Processs - Pre-Engagement)Document2 pagesAT-06 (FS Audit Processs - Pre-Engagement)Bernadette PanicanNo ratings yet

- Letter of BidDocument2 pagesLetter of BidRam pakhrinNo ratings yet

- ch15 Audit of The Payroll and Personnel CycleDocument55 pagesch15 Audit of The Payroll and Personnel CycleHarold Dela FuenteNo ratings yet

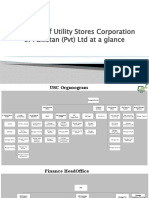

- Structure of Utility Stores Corporation of Pakistan (PVT) LTD at A GlanceDocument9 pagesStructure of Utility Stores Corporation of Pakistan (PVT) LTD at A GlanceMuhammad UsmanNo ratings yet

- SKILLS Financial and Corporate Reporting MODULE-IVDocument257 pagesSKILLS Financial and Corporate Reporting MODULE-IVanon_636625652100% (1)

- Psa Updates: The New Auditing StandardsDocument16 pagesPsa Updates: The New Auditing StandardsMae AstovezaNo ratings yet

- Check List For Security Audit 01Document8 pagesCheck List For Security Audit 01Rajvir ShramaNo ratings yet

- Carec Manual 1 Rsa English FinDocument51 pagesCarec Manual 1 Rsa English FinIlie BricicaruNo ratings yet

- Safety Culture Improvement through Consistent MessagingDocument28 pagesSafety Culture Improvement through Consistent MessagingRahmat Adi Saputra100% (4)

- Accountant (General) Immigration To Australia PR VisaDocument5 pagesAccountant (General) Immigration To Australia PR Visapriyank parikhNo ratings yet

- Ofi Compliance - Bhola ChoudhryDocument3 pagesOfi Compliance - Bhola ChoudhryDwitikrushna RoutNo ratings yet

- Assurance Services and The Integrity of Financial Reporting, 8 Edition William C. Boynton Raymond N. JohnsonDocument21 pagesAssurance Services and The Integrity of Financial Reporting, 8 Edition William C. Boynton Raymond N. JohnsonmerantidownloaderNo ratings yet

- Energy Consumption Audit For Chinhoyi University of Technology HotelDocument6 pagesEnergy Consumption Audit For Chinhoyi University of Technology HotelBethel NhamoNo ratings yet

- Vietnam National University audit assignmentDocument21 pagesVietnam National University audit assignmentPí Ká Heo100% (1)

- Accounting & Finance CertificateDocument3 pagesAccounting & Finance CertificateIslam MohsenNo ratings yet

- ATQ1SCBD3Document11 pagesATQ1SCBD3Helios HexNo ratings yet

- Corporate Frauds - Its Impact To Economy and Business EnvironmentDocument17 pagesCorporate Frauds - Its Impact To Economy and Business EnvironmentSoumendra Roy100% (3)

- Engagement LetterDocument5 pagesEngagement LetterJherico Gabriel B. OcomenNo ratings yet

- Haccp: Implementation in Food IndustriesDocument152 pagesHaccp: Implementation in Food IndustriesMacario Roy Jr AmoresNo ratings yet

- P3 Performance StrategyDocument4 pagesP3 Performance Strategyumer12No ratings yet

- 2071 Solvency Margin Directive For Non Life Insurer 1Document9 pages2071 Solvency Margin Directive For Non Life Insurer 1Htet Lynn HtunNo ratings yet