You might also like

- Conceptual FrameworkDocument5 pagesConceptual FrameworkMaica PontillasNo ratings yet

- IntroductionDocument8 pagesIntroductionIsaac MbaiNo ratings yet

- The Objective of General Purpose Financial ReportingDocument86 pagesThe Objective of General Purpose Financial ReportingAlex liaoNo ratings yet

- Test 1Document4 pagesTest 1Leslie CarrollNo ratings yet

- Framework For The Preparation and Presentation of Financial StatementsDocument14 pagesFramework For The Preparation and Presentation of Financial StatementsHasnain MahmoodNo ratings yet

- Financial Accounting 2017 Ist Semester FinalDocument100 pagesFinancial Accounting 2017 Ist Semester FinalLOVERAGE MUNEMONo ratings yet

- Conceptual Framework For Financial Reporting Resume Ch. 2Document6 pagesConceptual Framework For Financial Reporting Resume Ch. 2Dhivena JeonNo ratings yet

- CH-2-Study Guide PDFDocument15 pagesCH-2-Study Guide PDFnirali17No ratings yet

- General Purpose Financial Statements - Handout Part 2Document6 pagesGeneral Purpose Financial Statements - Handout Part 2desyanggandaNo ratings yet

- CPA - FR - Module 1 - The Role and Importance of Financial ReportingDocument11 pagesCPA - FR - Module 1 - The Role and Importance of Financial ReportingqueendillyNo ratings yet

- Module 2 Conceptual Framework For Financial ReportingDocument9 pagesModule 2 Conceptual Framework For Financial ReportingVivo V27No ratings yet

- Chapter 2 - The Conceptual FrameworkDocument5 pagesChapter 2 - The Conceptual FrameworkdiditayumeganNo ratings yet

- Chapter 2Document67 pagesChapter 2Adam MilakaraNo ratings yet

- Lecture 1 NoteDocument5 pagesLecture 1 NoteKanokporn TangthamvanichNo ratings yet

- Chapter 1 (1) NowteyDocument8 pagesChapter 1 (1) NowteyAkkamaNo ratings yet

- Guidelines in Fs PreparationDocument4 pagesGuidelines in Fs PreparationanacldnNo ratings yet

- Module 2Document29 pagesModule 2Katrina DacquelNo ratings yet

- Intermediate Accounting II (ACT 402)Document49 pagesIntermediate Accounting II (ACT 402)Youssef Ashraf TawfikNo ratings yet

- Revised AccountingDocument46 pagesRevised AccountingAli NasarNo ratings yet

- Orca Share Media1668925931673 6999982710921667804Document26 pagesOrca Share Media1668925931673 6999982710921667804Chekani Kristine MamhotNo ratings yet

- Chapter 1: The Objective of General Purpose Financial ReportingDocument22 pagesChapter 1: The Objective of General Purpose Financial ReportingSteven TanNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- L3Document4 pagesL3Emilrose SadiasaNo ratings yet

- Financial ReportingDocument133 pagesFinancial ReportingJOHN KAMANDANo ratings yet

- ACCT-2201 Assignment SiamDocument10 pagesACCT-2201 Assignment Siamsiamahmed2199No ratings yet

- Lecture 2 - Conceptual Framework For Financial Reporting - MODULEDocument8 pagesLecture 2 - Conceptual Framework For Financial Reporting - MODULEAristeia NotesNo ratings yet

- Who Are The Users of Accounting Information and How Do They Benefit From This Information?Document4 pagesWho Are The Users of Accounting Information and How Do They Benefit From This Information?Marco PaulNo ratings yet

- Conceptual Framework For Financial ReportingDocument54 pagesConceptual Framework For Financial ReportingAlthea Claire Yhapon100% (1)

- Conceptual FrameworkDocument45 pagesConceptual FrameworkKendall JennerNo ratings yet

- Chapter 2Document4 pagesChapter 2Ethan ChristiansNo ratings yet

- Chapter 1 Conceptual FrameworkDocument5 pagesChapter 1 Conceptual FrameworkJOMAR FERRERNo ratings yet

- Framework For The Preparation and Presentation of The Financial StatementsDocument28 pagesFramework For The Preparation and Presentation of The Financial StatementsTin ManaogNo ratings yet

- #02 Conceptual FrameworkDocument5 pages#02 Conceptual FrameworkZaaavnn VannnnnNo ratings yet

- Conceptual Framework: Objective of Financial ReportingDocument47 pagesConceptual Framework: Objective of Financial Reporting버니 모지코No ratings yet

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiNo ratings yet

- Accounting Standard of BangladeshDocument9 pagesAccounting Standard of BangladeshZahidnsuNo ratings yet

- CMA Volume IDocument432 pagesCMA Volume IEthan HuntNo ratings yet

- Chapter 01: Conceptual FrameworkDocument14 pagesChapter 01: Conceptual FrameworkCorin Ahmed CorinNo ratings yet

- PART 2 - Financial Accounting and Reporting OverviewDocument4 pagesPART 2 - Financial Accounting and Reporting OverviewHeidee BitancorNo ratings yet

- Chapter 1Document6 pagesChapter 1Rendra SeptikoNo ratings yet

- Conceptual Framework Module 1Document6 pagesConceptual Framework Module 1Jaime LaronaNo ratings yet

- Lesson 1 - Definitions J Concepts and Qualitative CharacteristicsDocument11 pagesLesson 1 - Definitions J Concepts and Qualitative Characteristicschembejosephine40No ratings yet

- Copyofcopy3ofapresentation 150501110626 Conversion Gate01Document11 pagesCopyofcopy3ofapresentation 150501110626 Conversion Gate01Gian LawrenceNo ratings yet

- Contemporary Ch2 NotesDocument3 pagesContemporary Ch2 NotesdhfbbbbbbbbbbbbbbbbbhNo ratings yet

- Financial AccountingDocument59 pagesFinancial AccountingKamal SinghNo ratings yet

- IFA Chapter 1Document12 pagesIFA Chapter 1Suleyman TesfayeNo ratings yet

- AC201 Notes PART 1Document25 pagesAC201 Notes PART 1mollymgonigle1No ratings yet

- J&K Training ManualDocument116 pagesJ&K Training ManualMajanja Ashery100% (1)

- Toa Iasb Conceptual FrameworkDocument11 pagesToa Iasb Conceptual FrameworkreinaNo ratings yet

- Summary Chapter 2Document5 pagesSummary Chapter 2Ahmad RifkiiNo ratings yet

- Conceptual Framework For Financial ReportingDocument8 pagesConceptual Framework For Financial ReportingQueeny Man-oyaoNo ratings yet

- Dwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFDocument35 pagesDwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFinactionwantwit.a8i0100% (12)

- ACCCOB2 Financial Accounting Discussion PDFDocument5 pagesACCCOB2 Financial Accounting Discussion PDFJose GuerreroNo ratings yet

- Pragyani S Maharjan 12/8/15 Accounting 507 - Text Chapter 2 - Conceptual Framework Basic QuestionsDocument6 pagesPragyani S Maharjan 12/8/15 Accounting 507 - Text Chapter 2 - Conceptual Framework Basic QuestionsPragyani ShresthaNo ratings yet

- Module 3 Conceptual Frameworks and Accounting StandardsDocument10 pagesModule 3 Conceptual Frameworks and Accounting StandardsJonabelle DalesNo ratings yet

- W2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1Document5 pagesW2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1leare ruazaNo ratings yet

- Intermediate Financial Accounting I 1 1Document192 pagesIntermediate Financial Accounting I 1 1natinaelbahiru74No ratings yet

- Lecture #1Document29 pagesLecture #1Nicole AngodungNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Module 11 - DramaDocument3 pagesModule 11 - DramaApril Joy ObedozaNo ratings yet

- Module 10 - DanceDocument9 pagesModule 10 - DanceApril Joy ObedozaNo ratings yet

- Annual Income Tax TableDocument1 pageAnnual Income Tax TableApril Joy ObedozaNo ratings yet

- Chap 1 - SFARDocument2 pagesChap 1 - SFARApril Joy ObedozaNo ratings yet

- Auditing - 1-10Document2 pagesAuditing - 1-10April Joy ObedozaNo ratings yet

- Income Based ValuationDocument25 pagesIncome Based ValuationApril Joy ObedozaNo ratings yet

- Module 12 - Prose and PoetryDocument4 pagesModule 12 - Prose and PoetryApril Joy ObedozaNo ratings yet

- Auditing 1-12Document2 pagesAuditing 1-12April Joy ObedozaNo ratings yet

- Chap 3-4Document58 pagesChap 3-4April Joy ObedozaNo ratings yet

- Auditing - 1-9Document1 pageAuditing - 1-9April Joy ObedozaNo ratings yet

- Strategic Decision Making ProcessDocument14 pagesStrategic Decision Making ProcessApril Joy ObedozaNo ratings yet

- Writing A Business PlanDocument3 pagesWriting A Business PlanApril Joy ObedozaNo ratings yet

- Statistics. AssessmentDocument3 pagesStatistics. AssessmentApril Joy ObedozaNo ratings yet

- Table of ContentsDocument5 pagesTable of ContentsApril Joy ObedozaNo ratings yet

- Statistical Analysis With Software Application Long QuizDocument2 pagesStatistical Analysis With Software Application Long QuizApril Joy ObedozaNo ratings yet

- Group 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityDocument6 pagesGroup 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityApril Joy ObedozaNo ratings yet

- MODULE 11 My Father Goes To CourtDocument3 pagesMODULE 11 My Father Goes To CourtApril Joy ObedozaNo ratings yet

- Module 6Document8 pagesModule 6April Joy ObedozaNo ratings yet

- Governance, Business Ethics, Risk Management and Internal Control ReportingDocument5 pagesGovernance, Business Ethics, Risk Management and Internal Control ReportingApril Joy ObedozaNo ratings yet

- Module 12 My Father's TragedyDocument3 pagesModule 12 My Father's TragedyApril Joy Obedoza100% (1)

- Group 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityDocument35 pagesGroup 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityApril Joy ObedozaNo ratings yet

- Name: Obedoza April Joy Lopez Course & Block: - Bsa 3-A - Subject: Life & Works of Carlos Bulosan SCHEDULEDocument3 pagesName: Obedoza April Joy Lopez Course & Block: - Bsa 3-A - Subject: Life & Works of Carlos Bulosan SCHEDULEApril Joy ObedozaNo ratings yet

- Life and Works of Carlos Bulosan - Module 1 AssessmentDocument2 pagesLife and Works of Carlos Bulosan - Module 1 AssessmentApril Joy ObedozaNo ratings yet

- Module 12 Art CriticismDocument3 pagesModule 12 Art CriticismApril Joy Obedoza100% (1)

- Assessment 2 Reading Visual ArtsDocument3 pagesAssessment 2 Reading Visual ArtsApril Joy ObedozaNo ratings yet

- Module 11 Art Context AnalysisDocument4 pagesModule 11 Art Context AnalysisApril Joy ObedozaNo ratings yet

- Joseph P. Prieto #32 Bulala St. Zone 5, Piaz (Plaza) Villasis Pangasinan CP # 09068081124Document3 pagesJoseph P. Prieto #32 Bulala St. Zone 5, Piaz (Plaza) Villasis Pangasinan CP # 09068081124April Joy ObedozaNo ratings yet

- Art Appreciation. Act. 2Document3 pagesArt Appreciation. Act. 2April Joy ObedozaNo ratings yet

- Chap 7. StrategicDocument4 pagesChap 7. StrategicApril Joy ObedozaNo ratings yet

- Statements Projected Profit & LossDocument6 pagesStatements Projected Profit & LossApril Joy ObedozaNo ratings yet

- Financial Accounting First Canadian Edition Canadian 1st Edition Waybright Test Bank DownloadDocument39 pagesFinancial Accounting First Canadian Edition Canadian 1st Edition Waybright Test Bank DownloadSherry Belvin100% (24)

- Chapter 1 - Introduction To Published AccountsDocument20 pagesChapter 1 - Introduction To Published AccountsParas VohraNo ratings yet

- 1516168684ECO P12 M24 E-TextDocument15 pages1516168684ECO P12 M24 E-TextVinay Kumar KumarNo ratings yet

- (B) 3,100 9,545 (F) 82 (H) 11 (I) 6 (J) (D) 39,780Document3 pages(B) 3,100 9,545 (F) 82 (H) 11 (I) 6 (J) (D) 39,780Kavya GopakumarNo ratings yet

- Pages From Stigler The Economist As Preacher, and Other Essays 1982-2Document4 pagesPages From Stigler The Economist As Preacher, and Other Essays 1982-2Kopija KopijaNo ratings yet

- REFERENCE READING 1.2 Finance For ManagerDocument5 pagesREFERENCE READING 1.2 Finance For ManagerDeepak MahatoNo ratings yet

- Material Complementario - Cafes Monte BiancoDocument20 pagesMaterial Complementario - Cafes Monte BiancoGlenda ChiquilloNo ratings yet

- DAYA 2019 Annual ReportDocument192 pagesDAYA 2019 Annual Reportanggita nur kNo ratings yet

- FA 1 Distance ModuleDocument175 pagesFA 1 Distance ModuleBereket Desalegn100% (5)

- How To Write A Traditional Business Plan: Step 1Document5 pagesHow To Write A Traditional Business Plan: Step 1Leslie Ann Elazegui UntalanNo ratings yet

- Accounts HeadDocument7 pagesAccounts HeadRobiul khanNo ratings yet

- Principles of Islamic Economics: © DR Muhammad Hamidullah Library, IIU, Islamabad. Http://iri - Iiu.edu - PKDocument19 pagesPrinciples of Islamic Economics: © DR Muhammad Hamidullah Library, IIU, Islamabad. Http://iri - Iiu.edu - PKHami KhaNNo ratings yet

- Is Excel Participant - Simplified v2Document10 pagesIs Excel Participant - Simplified v2Aaron Pool0% (2)

- ROBYG S A Financial Statements For The Year Ended 31 December 2021Document39 pagesROBYG S A Financial Statements For The Year Ended 31 December 2021Alejandro BujanNo ratings yet

- Wealth Taxes in India: - Ms. Dhwani MainkarDocument12 pagesWealth Taxes in India: - Ms. Dhwani MainkarNeha Sharma100% (1)

- Jawaban Allocation CostDocument3 pagesJawaban Allocation CostChelsea WulanNo ratings yet

- Revised January 1992 Daily Wage PayrollDocument4 pagesRevised January 1992 Daily Wage PayrollJhem Martinez100% (1)

- Chapter Exercises 3: Chapter Exercises 3: Taxpayers: TaxpayersDocument24 pagesChapter Exercises 3: Chapter Exercises 3: Taxpayers: TaxpayersKenneth Tupas UrbiztondoNo ratings yet

- Eco Practice Booklet Combined File May 2023Document107 pagesEco Practice Booklet Combined File May 2023prince soniNo ratings yet

- How I Made 1 MM Res Lling SoftwareDocument77 pagesHow I Made 1 MM Res Lling SoftwareAshwin100% (1)

- George Reisman's Blog On Economics, Politics, Society, and Culture - Piketty's Capital - Wrong Theory - Destructive ProgramDocument25 pagesGeorge Reisman's Blog On Economics, Politics, Society, and Culture - Piketty's Capital - Wrong Theory - Destructive ProgramrarescraciuNo ratings yet

- Study Material XII EconomicsDocument52 pagesStudy Material XII EconomicsuniquekoshishNo ratings yet

- Form PDF 114320560260722Document9 pagesForm PDF 114320560260722DeepNo ratings yet

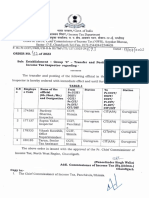

- Transfer and Posting in The Cadre of ITI Dated 13.07.2023.Document2 pagesTransfer and Posting in The Cadre of ITI Dated 13.07.2023.InspectorNo ratings yet

- Computation For Exercise 1Document10 pagesComputation For Exercise 1Xyzra AlfonsoNo ratings yet

- Module 1C - ACCCOB2 - Conceptual Framework For Financial Reporting - FHVDocument56 pagesModule 1C - ACCCOB2 - Conceptual Framework For Financial Reporting - FHVCale Robert RascoNo ratings yet

- Abm Acctg Firm Section 2am 2Document40 pagesAbm Acctg Firm Section 2am 2Diana Rosales CalNo ratings yet

- 3271010Document4 pages3271010mohitgaba19No ratings yet

- Individual Illustration and Activity No. 2Document22 pagesIndividual Illustration and Activity No. 2Angela CanayaNo ratings yet

- Pengaruh PDRB, Inflasi Dan Rasio Gini Terhadap Pengangguran Terbuka Di Provinsi DKI JakartaDocument12 pagesPengaruh PDRB, Inflasi Dan Rasio Gini Terhadap Pengangguran Terbuka Di Provinsi DKI JakartaMahendraNo ratings yet