You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaFrom EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNo ratings yet

- Unit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)Document6 pagesUnit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)aiswarya sNo ratings yet

- Chapter 7 Exercises With SolutionDocument5 pagesChapter 7 Exercises With Solutionmohammad khataybehNo ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Exercises No1 CCash Equiv and Bank ReconDocument3 pagesExercises No1 CCash Equiv and Bank Recondelrosario.kenneth996No ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Acctg 102 Prelim Quiz 1 With SolutionDocument9 pagesAcctg 102 Prelim Quiz 1 With SolutionYsabel ApostolNo ratings yet

- Chapter 2 Last PartDocument11 pagesChapter 2 Last PartXENA LOPEZ100% (2)

- (03B) Cash SPECIAL Quiz ANSWER KEYDocument6 pages(03B) Cash SPECIAL Quiz ANSWER KEYGabriel Adrian ObungenNo ratings yet

- Summary For The Preparation of Bank Reconciliation StatementDocument5 pagesSummary For The Preparation of Bank Reconciliation StatementGhalib HussainNo ratings yet

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDocument23 pagesPittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNo ratings yet

- Additional Illustrations-14Document8 pagesAdditional Illustrations-14Gulneer LambaNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- Quiz 1Document3 pagesQuiz 1Van MateoNo ratings yet

- Practical Accounting by Valix Practical Accounting by ValixDocument24 pagesPractical Accounting by Valix Practical Accounting by ValixMartha Nicole MaristelaNo ratings yet

- Diagnostic QuizDocument3 pagesDiagnostic QuizXENA LOPEZNo ratings yet

- Accounting IAS Model Answers Series 4 2009Document16 pagesAccounting IAS Model Answers Series 4 2009Aung Zaw HtweNo ratings yet

- Additional Illustrations-13Document5 pagesAdditional Illustrations-13Deepak YadavNo ratings yet

- IA Chapter-8-10Document8 pagesIA Chapter-8-10Christine Joyce EnriquezNo ratings yet

- Bank Reconciliation StatementDocument9 pagesBank Reconciliation StatementMarvin tvNo ratings yet

- UntitledDocument5 pagesUntitledShevina Maghari shsnohsNo ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Months To Go Until They MatureDocument5 pagesMonths To Go Until They MatureJude SantosNo ratings yet

- Cash and Cash Equivalents Quizzer 1Document5 pagesCash and Cash Equivalents Quizzer 1yna kyleneNo ratings yet

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- CHAPTER-15 - Bank Reconciliation System Practical QuestionsDocument49 pagesCHAPTER-15 - Bank Reconciliation System Practical QuestionsBHARAT MAHAN RAI 22BBA10031No ratings yet

- Cash and Cash Equivalents C5 Valix 2006Document5 pagesCash and Cash Equivalents C5 Valix 2006Ghaill CruzNo ratings yet

- Ervin 2Document48 pagesErvin 2micaangelgonzales.smmcNo ratings yet

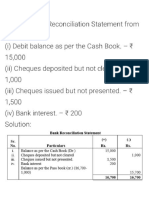

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

- Cash and Cash EquivalentDocument32 pagesCash and Cash EquivalentArbie D. DecimioNo ratings yet

- Problem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer ADocument37 pagesProblem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer AAldrin Lozano87% (15)

- Bank AccountingDocument8 pagesBank Accountinggordonomond2022No ratings yet

- Updates - Midterm Lspu ExamDocument6 pagesUpdates - Midterm Lspu ExamAngelo HilomaNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationjinyangsuelNo ratings yet

- Bank Reconciliation Dollar CompDocument5 pagesBank Reconciliation Dollar CompCJ alandy100% (2)

- Bank Reconciliation StetementsDocument5 pagesBank Reconciliation StetementsSheikh RakinNo ratings yet

- Module 10 Financial StatementsDocument17 pagesModule 10 Financial StatementsChristine CariñoNo ratings yet

- Samplepractice Exam 15 October 2020 Questions and AnswersDocument6 pagesSamplepractice Exam 15 October 2020 Questions and AnswersMartha Nicole MaristelaNo ratings yet

- Cafc Test Paper Acc 03Document9 pagesCafc Test Paper Acc 03Vandana GuptaNo ratings yet

- Akuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Document2 pagesAkuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Muhamad Rizal DinyatNo ratings yet

- Problem 1: Partially Secured UnsecuredDocument2 pagesProblem 1: Partially Secured UnsecuredYahlianah LeeNo ratings yet

- INTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Document210 pagesINTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Shairine Aquino100% (2)

- Proof+of+Cash ProblemsDocument2 pagesProof+of+Cash ProblemshelaihjsNo ratings yet

- Proof of Cash ProblemsDocument2 pagesProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- Review - SFP To Interim ReportingDocument3 pagesReview - SFP To Interim ReportingAna Marie IllutNo ratings yet

- 4 Solution Exam Auditing 2Document5 pages4 Solution Exam Auditing 2Kristina KittyNo ratings yet

- Checking Account in BPIDocument2 pagesChecking Account in BPIelsana philipNo ratings yet

- FIA141 Term Test 1 Solution 2019 3Document9 pagesFIA141 Term Test 1 Solution 2019 3Nosipho MsimangoNo ratings yet

- Chapter Review Solutions: Chapter 5: The Double Entry SystemDocument7 pagesChapter Review Solutions: Chapter 5: The Double Entry SystemsriNo ratings yet

- Docile Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageDocile Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Bank Reconciliation QuestionsDocument14 pagesBank Reconciliation QuestionsangaNo ratings yet

- Quizbee Practice IntaccDocument21 pagesQuizbee Practice IntaccCharles Kevin MinaNo ratings yet

- AP - Quiz 01 (UCP)Document8 pagesAP - Quiz 01 (UCP)CrestinaNo ratings yet

- Statement of Financial PositionDocument2 pagesStatement of Financial PositionmoNo ratings yet

- FarDocument8 pagesFarnivea gumayagay71% (7)

- 2021 Prelim Exam Auditing Concepts and Applications 1Document15 pages2021 Prelim Exam Auditing Concepts and Applications 1moreNo ratings yet

- Full Credit Report - EXAMPLEDocument1 pageFull Credit Report - EXAMPLEChris PearsonNo ratings yet

- Hathway Internet Bill - 2022-2023Document1 pageHathway Internet Bill - 2022-2023shwetaawaleNo ratings yet

- Statement of Axis Account No:921010029361795 For The Period (From: 30-12-2022 To: 29-03-2023)Document2 pagesStatement of Axis Account No:921010029361795 For The Period (From: 30-12-2022 To: 29-03-2023)WONDERLAND CLEARANCENo ratings yet

- Receipts Awaiting Remittance ReportDocument6 pagesReceipts Awaiting Remittance ReportShakhir MohunNo ratings yet

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVara Prasad AvulaNo ratings yet

- Using Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFDocument21 pagesUsing Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFchompdumetoseei5100% (8)

- Danta Health Bank Statement 05.31.10Document4 pagesDanta Health Bank Statement 05.31.10Prasenjit Saha0% (1)

- Water CorporationDocument2 pagesWater CorporationAleksania NolanNo ratings yet

- Liberty Debit Card ReckonerDocument3 pagesLiberty Debit Card ReckonerJohn SonNo ratings yet

- As Accounting Sole Trader AccountsDocument17 pagesAs Accounting Sole Trader AccountsGill SabNo ratings yet

- GST Suvidha Kendra Service List 2019Document26 pagesGST Suvidha Kendra Service List 2019Jayant Kumar SwainNo ratings yet

- 2018 Lehi PrepDocument6 pages2018 Lehi PrepEmilyNo ratings yet

- BMO Preferred Rate Mastercard: Period Covered by This StatementDocument4 pagesBMO Preferred Rate Mastercard: Period Covered by This StatementBubba Johns100% (1)

- B25 - General Information and RegistrationDocument15 pagesB25 - General Information and RegistrationMayandra Fatima HadisupraptoNo ratings yet

- Scrip OnlineDocument1 pageScrip OnlineMarcia A Vidal MarchettiNo ratings yet

- Banking Law Pre University Question Paper LLBDocument4 pagesBanking Law Pre University Question Paper LLBKRISHNA VIDHUSHANo ratings yet

- Your Rewards Credit Card Statement: From Overseas Tel 44 1226 261 010Document3 pagesYour Rewards Credit Card Statement: From Overseas Tel 44 1226 261 010Shubham BhaumikNo ratings yet

- 1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashDocument7 pages1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashSheidee ValienteNo ratings yet

- Jiofiber Bill Summary: Total Payable 706.82Document1 pageJiofiber Bill Summary: Total Payable 706.82diksha sharmaNo ratings yet

- 11th Accounts Mock Paper-1Document2 pages11th Accounts Mock Paper-1Aliasgar ZaverNo ratings yet

- Septemeber ICCIDocument2 pagesSeptemeber ICCIShivendra KumarNo ratings yet

- Project Report UBLDocument37 pagesProject Report UBLTahir KhurshidNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsBeat KarbNo ratings yet

- TCF Free Checking: Linda Renee Nelson 214 Sycarmore ST GRAHAM MO 64455Document6 pagesTCF Free Checking: Linda Renee Nelson 214 Sycarmore ST GRAHAM MO 64455PatriciaNo ratings yet

- Assignment 4 - Credit Card Reconciliation - Angela CreagmileDocument6 pagesAssignment 4 - Credit Card Reconciliation - Angela Creagmileapi-471231467100% (1)

- Citibank ElenaDocument8 pagesCitibank ElenaAndre BarrazaNo ratings yet

- Vocabulary Ex11Document5 pagesVocabulary Ex11tayaNo ratings yet

- FORM Request For Death CertificateDocument2 pagesFORM Request For Death CertificateBeyza GemiciNo ratings yet

- Chapter 5 - Using CreditDocument48 pagesChapter 5 - Using CreditALEXIA TANG DAI XIANNo ratings yet

- Control of Cash and Credit: Cash Control - Cash Control Involves All The Transactions Which The Guest Makes inDocument14 pagesControl of Cash and Credit: Cash Control - Cash Control Involves All The Transactions Which The Guest Makes inAryan BishtNo ratings yet