90% found this document useful (48 votes)

644K views5 pagesClass 11 Micro Economics Chapter 1 Notes PDF

This document provides an overview of microeconomics and macroeconomics. It defines the two fields, notes their importance and differences, and summarizes some key concepts.

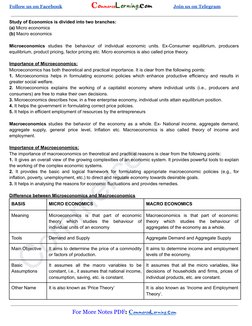

[1] Microeconomics studies individual economic decision-making units like consumers and producers, while macroeconomics looks at aggregates for the entire economy such as output, employment and inflation.

[2] Microeconomics helps form policies and explains market equilibrium, while macroeconomics provides tools to analyze complex economies and form policies for goals like low inflation.

[3] The production possibility frontier illustrates the key economic problem of scarcity and tradeoffs between allocating limited resources to different goods.

Uploaded by

JAINAB 'X B'Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

90% found this document useful (48 votes)

644K views5 pagesClass 11 Micro Economics Chapter 1 Notes PDF

This document provides an overview of microeconomics and macroeconomics. It defines the two fields, notes their importance and differences, and summarizes some key concepts.

[1] Microeconomics studies individual economic decision-making units like consumers and producers, while macroeconomics looks at aggregates for the entire economy such as output, employment and inflation.

[2] Microeconomics helps form policies and explains market equilibrium, while macroeconomics provides tools to analyze complex economies and form policies for goals like low inflation.

[3] The production possibility frontier illustrates the key economic problem of scarcity and tradeoffs between allocating limited resources to different goods.

Uploaded by

JAINAB 'X B'Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd