You might also like

- Banking and Its TypesDocument5 pagesBanking and Its Typesविनीत जैनNo ratings yet

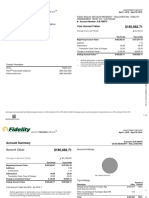

- Your Account Value:: Fidelity Rollover Ira David Moriarty - Rollover Ira - Fidelity Management Trust Co - CustodianDocument6 pagesYour Account Value:: Fidelity Rollover Ira David Moriarty - Rollover Ira - Fidelity Management Trust Co - CustodianMarcus GreenNo ratings yet

- Power of Attorney (Banking)Document2 pagesPower of Attorney (Banking)Legal Forms100% (3)

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- Cash Handling ManualDocument88 pagesCash Handling ManualSrishti Vasdev100% (1)

- 0 - Retail Banking Doc2Document8 pages0 - Retail Banking Doc2Niyati BagweNo ratings yet

- The Debt Forum PresentationsDocument72 pagesThe Debt Forum PresentationsrobcannonNo ratings yet

- Aids To TradeDocument24 pagesAids To TradeVivek Shaw86% (14)

- Busfin 7 Sources and Uses of Short Term and Long Term FundsDocument5 pagesBusfin 7 Sources and Uses of Short Term and Long Term FundsRenz Abad50% (2)

- Narrative Report (PNB)Document16 pagesNarrative Report (PNB)Rhea Hubo Fajardo93% (15)

- Market Leader Answer Keys 2Document21 pagesMarket Leader Answer Keys 2Ale GuzmÁn67% (6)

- New Non Banking Financial InstitutionsDocument18 pagesNew Non Banking Financial InstitutionsGarima SinghNo ratings yet

- Financial ServicesDocument40 pagesFinancial ServicesIsha Chandok100% (1)

- Banking Products and ServicesDocument15 pagesBanking Products and ServicesAbhayVarunKesharwaniNo ratings yet

- Financial Services SectorDocument12 pagesFinancial Services SectorDominic RomeroNo ratings yet

- The Role of Commercial BanksDocument29 pagesThe Role of Commercial BanksGeorge Cristinel RotaruNo ratings yet

- Advancing of Loans: Difference Between Bank Overdraft and Cash CreditDocument7 pagesAdvancing of Loans: Difference Between Bank Overdraft and Cash CreditpraharshithaNo ratings yet

- Chapter 01 Power PointDocument37 pagesChapter 01 Power PointmuluNo ratings yet

- By - Anish Nair - Bibekanand Mishra - Dewanshu Kumar - Pranav Nagar - Prateek GoyalDocument32 pagesBy - Anish Nair - Bibekanand Mishra - Dewanshu Kumar - Pranav Nagar - Prateek Goyalbibekmishra8107No ratings yet

- BankingDocument55 pagesBankingAnkit JajalNo ratings yet

- UNIT 1 Core Banking Vs Allied Banking Activities AKG-1Document21 pagesUNIT 1 Core Banking Vs Allied Banking Activities AKG-1A Walk To InfinityNo ratings yet

- Banking Law and PractiseDocument7 pagesBanking Law and PractiseZ the officerNo ratings yet

- Retail: Business LoanDocument6 pagesRetail: Business LoanVinayak ShetNo ratings yet

- Types of BanksDocument15 pagesTypes of BanksshubhamdevganNo ratings yet

- Role of Commercial Bank-1Document9 pagesRole of Commercial Bank-1TanzeemNo ratings yet

- Banking System in India: Sheetal ThomasDocument28 pagesBanking System in India: Sheetal Thomassheetalsmijo704No ratings yet

- Commercial BankDocument2 pagesCommercial BankFardin Ahmed MugdhoNo ratings yet

- Module 2 2020Document87 pagesModule 2 2020Hariprasad bhatNo ratings yet

- Financial ServicesDocument3 pagesFinancial ServicesakhilalakshmiNo ratings yet

- A Bank Is A Financial Intermediary That Accepts Deposits and Channels Those Deposits Into Lending ActivitiesDocument17 pagesA Bank Is A Financial Intermediary That Accepts Deposits and Channels Those Deposits Into Lending ActivitiesSuyog AmrutraoNo ratings yet

- Banking Regulations and Services: Dr.N.Ramesh KumarDocument82 pagesBanking Regulations and Services: Dr.N.Ramesh KumarrameshncmNo ratings yet

- Câu 5-7,8 Global Financial ServicesDocument23 pagesCâu 5-7,8 Global Financial ServicesHà VũNo ratings yet

- Banking Allied ServicesDocument11 pagesBanking Allied ServicesSrinivasula Reddy P100% (5)

- Chapter One An Over View of BankingDocument10 pagesChapter One An Over View of BankingTajudin Abba RagooNo ratings yet

- Role of BankingDocument47 pagesRole of BankingMubashir QureshiNo ratings yet

- Chapter 3 & 4 Banking An Operations 2Document15 pagesChapter 3 & 4 Banking An Operations 2ManavAgarwalNo ratings yet

- Extra I - Retail Banking & Banking Arrangements PDFDocument15 pagesExtra I - Retail Banking & Banking Arrangements PDFrizzzNo ratings yet

- What Is BankDocument38 pagesWhat Is BankappyNo ratings yet

- Unit 6 Banking ComplianceDocument20 pagesUnit 6 Banking ComplianceChirag OstwalNo ratings yet

- What Is A Commercial BankDocument12 pagesWhat Is A Commercial BankDEEPUNo ratings yet

- Com BankDocument25 pagesCom BankAnonymous y3E7iaNo ratings yet

- Bank Interview Question For Business GraduateDocument7 pagesBank Interview Question For Business GraduateHumayun KabirNo ratings yet

- 307 NotesDocument6 pages307 NotesNeel ManushNo ratings yet

- Black BookDocument27 pagesBlack Bookmanwanimuki12No ratings yet

- Meaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofDocument32 pagesMeaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofPunya KrishnaNo ratings yet

- Retail BankingDocument14 pagesRetail BankingAkansha DasNo ratings yet

- BMF FullDocument48 pagesBMF FullPunya KrishnaNo ratings yet

- Unit III: Introduction To Financial InstitutionDocument11 pagesUnit III: Introduction To Financial Institutionshourya rastogiNo ratings yet

- Types of BankingDocument3 pagesTypes of BankingSunni ZaraNo ratings yet

- Banking FacilitiesDocument3 pagesBanking FacilitiesOsama AhmedNo ratings yet

- COMMERCIALDocument15 pagesCOMMERCIALBadbitchNo ratings yet

- Bank AS Financial Service Provider: Under The Guidance of "Institute For Finance, Banking and Insurance (IFBI) ")Document17 pagesBank AS Financial Service Provider: Under The Guidance of "Institute For Finance, Banking and Insurance (IFBI) ")Teja NadhNo ratings yet

- Chapter-2: Commercial BankDocument9 pagesChapter-2: Commercial Bankhasan alNo ratings yet

- Business Services Part 2Document11 pagesBusiness Services Part 2Santa GlenmarkNo ratings yet

- Bank of Maharashtra ProjectDocument67 pagesBank of Maharashtra ProjectDilip JainNo ratings yet

- Bank Operations and ManagementDocument4 pagesBank Operations and ManagementBibek Sh KhadgiNo ratings yet

- TejshreeDocument51 pagesTejshreeSmily ShaikhNo ratings yet

- Banking N Session-4 & 5Document49 pagesBanking N Session-4 & 5Vaibhav AggarwalNo ratings yet

- Research Paper On Banker As An Agent: Critical Study: Banking and Insurance LawDocument16 pagesResearch Paper On Banker As An Agent: Critical Study: Banking and Insurance LawGyanendra kumarNo ratings yet

- Pratik JadhavDocument64 pagesPratik JadhavSandip ChavanNo ratings yet

- Meaning of Banking: 1. Central BanksDocument6 pagesMeaning of Banking: 1. Central BanksMuskanNo ratings yet

- Banking Allied ServicesDocument30 pagesBanking Allied ServicesSrinivasula Reddy P50% (2)

- Financial InstitutionsDocument76 pagesFinancial InstitutionsGaurav Rathaur100% (1)

- Unit 2 DBDocument28 pagesUnit 2 DBDeepika. BabuNo ratings yet

- Lecture # 15: Role of Commercial BanksDocument46 pagesLecture # 15: Role of Commercial BanksMudassar NawazNo ratings yet

- Banks and Other Financial Intermediaries: By: John Paulo H. PobleteDocument12 pagesBanks and Other Financial Intermediaries: By: John Paulo H. PobleteMary Elleonice Franchette QuiambaoNo ratings yet

- Banking Awarenesve - Indian Banking System Part-2Document4 pagesBanking Awarenesve - Indian Banking System Part-2samskruti speaksNo ratings yet

- BANKING SS-LIVE - GOVT OF INDIA SCHEMES-MCQsDocument4 pagesBANKING SS-LIVE - GOVT OF INDIA SCHEMES-MCQssamskruti speaksNo ratings yet

- Computer Awareness - Computer Awareness-1Document12 pagesComputer Awareness - Computer Awareness-1samskruti speaksNo ratings yet

- Advanced Program-Reasoning - Critical Reasoning Day-16Document6 pagesAdvanced Program-Reasoning - Critical Reasoning Day-16samskruti speaksNo ratings yet

- Chap001 (11 Files Merged) PDFDocument819 pagesChap001 (11 Files Merged) PDFcynthiaaa sNo ratings yet

- US Credit Cards - McKinsey & CompanyDocument9 pagesUS Credit Cards - McKinsey & Companystevtan01No ratings yet

- BUS 485 .. Business Research MethodsDocument49 pagesBUS 485 .. Business Research MethodsSYED WAFI0% (1)

- Tutorial 2 QuestionsDocument4 pagesTutorial 2 QuestionswarishaaNo ratings yet

- MERGER of Bank of Rajasthan With Icici BankDocument15 pagesMERGER of Bank of Rajasthan With Icici BankAkansha RastogiNo ratings yet

- Ruiz v. PeopleDocument12 pagesRuiz v. PeopleRMN Rommel DulaNo ratings yet

- Islamic Accounting History, Development and Prospects: Amela TrokicDocument6 pagesIslamic Accounting History, Development and Prospects: Amela TrokicAbu WidadNo ratings yet

- HR Practices in National Bank of PakistanDocument34 pagesHR Practices in National Bank of PakistanSohaib AkbarNo ratings yet

- Course Material 4 - Accounting For Disbursement and Related TransactionsDocument32 pagesCourse Material 4 - Accounting For Disbursement and Related TransactionsJayvee BernalNo ratings yet

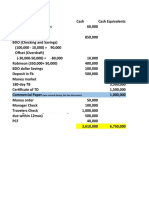

- Answer To Problems On Cash & Cash Equivalents - Reinforcement DiscussionDocument8 pagesAnswer To Problems On Cash & Cash Equivalents - Reinforcement DiscussionAnnie RapanutNo ratings yet

- Job Application Letter Bank TellerDocument8 pagesJob Application Letter Bank Tellerwyukqzfmd100% (1)

- 8th NSEDP 2016-2020Document204 pages8th NSEDP 2016-2020Bounna PhoumalavongNo ratings yet

- BCom Professional Sem 1 & 2 Syllabus As Per Govt NEP GRDocument16 pagesBCom Professional Sem 1 & 2 Syllabus As Per Govt NEP GRShivam YadavNo ratings yet

- Philippine Commercial International Bank v. GomezDocument5 pagesPhilippine Commercial International Bank v. GomezVic FrondaNo ratings yet

- GLCA DA MS Excel HBFC Project Modified-1Document3 pagesGLCA DA MS Excel HBFC Project Modified-1Subhan Ahmad KhanNo ratings yet

- About Citiphone: Citiphone Inbound Officer (Banking / Cards)Document3 pagesAbout Citiphone: Citiphone Inbound Officer (Banking / Cards)qqmernasreen71No ratings yet

- Presentation On Key Performance Indicators (KPI) and CAMEL Analysis of andDocument44 pagesPresentation On Key Performance Indicators (KPI) and CAMEL Analysis of andPravin MehtaNo ratings yet

- Bank Management SystemDocument37 pagesBank Management SystemSneha SrijayaNo ratings yet

- Credit Rating of Jamuna Bank Ltd.Document4 pagesCredit Rating of Jamuna Bank Ltd.arifNo ratings yet

- Gcash Uat Test ScriptDocument17 pagesGcash Uat Test ScriptPatricia Anne FigueroaNo ratings yet

- Retail Banking Dissertation TopicsDocument7 pagesRetail Banking Dissertation Topicsdiasponibar1981100% (1)

- Rti GT WS C01u04s10e01 01 VundDocument15 pagesRti GT WS C01u04s10e01 01 VundtommyNo ratings yet

- Foreign Exchange Operations of Jamuna BankDocument43 pagesForeign Exchange Operations of Jamuna BankHole StudioNo ratings yet