You might also like

- Statement 2022 01 21Document4 pagesStatement 2022 01 21Ali HassanNo ratings yet

- Ward School Bus Case AnalysisDocument11 pagesWard School Bus Case AnalysisJeswel RebatoNo ratings yet

- UA Case Study AnalysisDocument5 pagesUA Case Study AnalysisSarannyaRajendraNo ratings yet

- Amazon Company Mission and Vision StatementDocument20 pagesAmazon Company Mission and Vision StatementThe Caped CrusaderNo ratings yet

- Article To Read For New Product DevelopmentDocument18 pagesArticle To Read For New Product DevelopmentRaviteja GogineniNo ratings yet

- Mathematical Treasure Hunt Code CrackedDocument5 pagesMathematical Treasure Hunt Code CrackedChistan Junel DumoNo ratings yet

- Sun Zi Final AssignmentDocument9 pagesSun Zi Final Assignment摩羯座No ratings yet

- Admissionletter PDFDocument2 pagesAdmissionletter PDFVirginia HoffmanNo ratings yet

- Infobacktrack-NOM MSC BINsDocument7 pagesInfobacktrack-NOM MSC BINsmarcos DatilhoNo ratings yet

- Performance Evaluation of PNB and HDFC BankDocument58 pagesPerformance Evaluation of PNB and HDFC BankEkam Jot100% (1)

- September 2020 Call RecordDocument9 pagesSeptember 2020 Call RecordIshwarya RajeshNo ratings yet

- Internet Payment GatewayDocument25 pagesInternet Payment Gatewaymerahdelima100% (1)

- DR CRDocument8 pagesDR CRJocel LongosNo ratings yet

- Marketing FunctionsDocument4 pagesMarketing FunctionsUmar SulemanNo ratings yet

- Brief History and Services of 2GO Group IncDocument5 pagesBrief History and Services of 2GO Group IncJohn Patrick ReynosNo ratings yet

- Unit 2 AdvertisingDocument45 pagesUnit 2 AdvertisingWeekly Recorder100% (1)

- Disciplines and Ideas in The Social DLPDocument133 pagesDisciplines and Ideas in The Social DLPTrisTan Dolojan89% (36)

- Strategic Management For Government Agencies An Institutional Approach For Developing and Transition Economies Parts 63 386Document121 pagesStrategic Management For Government Agencies An Institutional Approach For Developing and Transition Economies Parts 63 386Abbas Al hemeryNo ratings yet

- All CCDocument66 pagesAll CCsukoymambo0% (1)

- HP Case StudyDocument4 pagesHP Case StudyJomarieVillanueva0% (1)

- China Merchant BankDocument4 pagesChina Merchant BankKevin McleanNo ratings yet

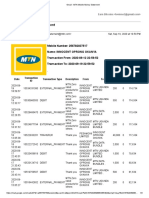

- Gmail - MTN Mobile Money Statement PDFDocument3 pagesGmail - MTN Mobile Money Statement PDFokanyaNo ratings yet

- Farm Tools GuideDocument18 pagesFarm Tools GuideZhymone Nelle Q. RiveraNo ratings yet

- Operations and Supply Chain Services PDFDocument7 pagesOperations and Supply Chain Services PDFSHAGUN SHRIVASTAVANo ratings yet

- An Online Mobile Shopping Application For Uchumi Supermarket in UgandaDocument9 pagesAn Online Mobile Shopping Application For Uchumi Supermarket in UgandaKIU PUBLICATION AND EXTENSIONNo ratings yet

- Organizational Design & Development in ICICI BankDocument13 pagesOrganizational Design & Development in ICICI Banksg2004slg100% (1)

- Chapter-1: Company - ProfileDocument54 pagesChapter-1: Company - ProfilePavan KumarNo ratings yet

- Sales Objectives For Marketing PlanningDocument7 pagesSales Objectives For Marketing PlanningAndrés SicaerosNo ratings yet

- Case Presentation and Analysis - Operations JollibeeDocument7 pagesCase Presentation and Analysis - Operations JollibeeDonnabie Pearl Pacaba-CantaNo ratings yet

- Iceland's aim to redistribute one million meals of surplus food by 2021/22Document13 pagesIceland's aim to redistribute one million meals of surplus food by 2021/22Javier Arles Lopez Astaiza100% (1)

- Paras Major Project BBA 6 Sem-2Document31 pagesParas Major Project BBA 6 Sem-2Abhinav KumarNo ratings yet

- ENVIRONMENT ANALYSIS Is The Study of The Organizational Environment To Pinpoint Environmental Factors That Can Significantly Influence Organizational OperationsDocument2 pagesENVIRONMENT ANALYSIS Is The Study of The Organizational Environment To Pinpoint Environmental Factors That Can Significantly Influence Organizational OperationsMohit BhardwajNo ratings yet

- Organizational Structure and Culture of FacebookDocument11 pagesOrganizational Structure and Culture of FacebookSaloni ParakhNo ratings yet

- Daily Life Psychology QuizzesDocument9 pagesDaily Life Psychology QuizzesIzhan KadirNo ratings yet

- Blue Ocean StrategyDocument2 pagesBlue Ocean StrategyNilesh BidriNo ratings yet

- Apple's Strengths (Internal Strategic Factors)Document3 pagesApple's Strengths (Internal Strategic Factors)Thalia ThaliaNo ratings yet

- Krispy Kreme Case StudyDocument4 pagesKrispy Kreme Case StudyBilal RajaNo ratings yet

- Home Depot faces competitive challengesDocument17 pagesHome Depot faces competitive challengesusergarciaNo ratings yet

- Essential Definition of Supply Chain ManagementDocument24 pagesEssential Definition of Supply Chain ManagementSyed Muhammad TalibNo ratings yet

- VISTA LAND AND LIFESCAPES INC FinalDocument9 pagesVISTA LAND AND LIFESCAPES INC Finalmarie crisNo ratings yet

- Solved Your Client Meade Technical Solutions Proposes To Merge With DealyDocument1 pageSolved Your Client Meade Technical Solutions Proposes To Merge With DealyAnbu jaromia100% (1)

- Reviewer in EntrepreneurshipDocument14 pagesReviewer in EntrepreneurshipNicole Andrea FajardoNo ratings yet

- Organizational Culture's Impact on Job SatisfactionDocument8 pagesOrganizational Culture's Impact on Job SatisfactionArifur Rahman HeraNo ratings yet

- Case Study Nivea For MenDocument15 pagesCase Study Nivea For Mensiti_syahirahNo ratings yet

- Financial Management Chapter 1&2Document5 pagesFinancial Management Chapter 1&2Shella TivesNo ratings yet

- Margin Call Ntegrated Case StudyDocument15 pagesMargin Call Ntegrated Case Studyamnakhai0% (1)

- Marketing Strategy of TakedaDocument11 pagesMarketing Strategy of TakedaRushin ShahNo ratings yet

- Human Resources PolicyDocument31 pagesHuman Resources PolicyNeha SharmaNo ratings yet

- PowerpointDocument31 pagesPowerpointEdilberto PantaleonNo ratings yet

- Problems and Opportunities of Dragon Fruit Production in The PhilippinesDocument17 pagesProblems and Opportunities of Dragon Fruit Production in The PhilippinesJan Michael VecillesNo ratings yet

- BE Coca ColaDocument28 pagesBE Coca ColaAnish NairNo ratings yet

- Applicant Writen SubmissionDocument38 pagesApplicant Writen SubmissionGidius KatoNo ratings yet

- Distribution Channels and Supply Chain Unit 5Document29 pagesDistribution Channels and Supply Chain Unit 5NANDANI AGARWALNo ratings yet

- Rle Ncma217 PrelimDocument16 pagesRle Ncma217 PrelimRochelle RagoNo ratings yet

- Artificial Intelligence As Enabler in The Marketing Process: A Research AgendaDocument10 pagesArtificial Intelligence As Enabler in The Marketing Process: A Research Agendashashwat shuklaNo ratings yet

- SwotDocument4 pagesSwotromitguptaNo ratings yet

- Proposed Hubbard County Ordinance For The Licensing of THC/Cannabinoid ProductsDocument8 pagesProposed Hubbard County Ordinance For The Licensing of THC/Cannabinoid ProductsinforumdocsNo ratings yet

- Sunrise BankDocument3 pagesSunrise BankVinod JoshiNo ratings yet

- Maximizing Profits Through Efficient Inventory ManagementDocument17 pagesMaximizing Profits Through Efficient Inventory ManagementMonica Lorevella NegreNo ratings yet

- BCG Space Tow SCPMDocument5 pagesBCG Space Tow SCPMDanica Rizzie TolentinoNo ratings yet

- Federal Acknowledgment FindingDocument9 pagesFederal Acknowledgment FindingWXMINo ratings yet

- A Passion That Became A BrandDocument1 pageA Passion That Became A BrandGiang ĐinhNo ratings yet

- Presentation On Business Plan: Creamy Lake Ice Cream ParlorDocument26 pagesPresentation On Business Plan: Creamy Lake Ice Cream ParlorEthila Palit100% (1)

- Pest, SWOT Analysis, Five ModelsDocument11 pagesPest, SWOT Analysis, Five ModelsLouisse Valeria100% (1)

- Strategic Management A Competitive Advantage Approach, Concepts Ebook David, Fred R, David, Forest R. Kindle StoDocument1 pageStrategic Management A Competitive Advantage Approach, Concepts Ebook David, Fred R, David, Forest R. Kindle StoManoj MadduriNo ratings yet

- Burger KingDocument6 pagesBurger KingCaro GrNo ratings yet

- Business Analytics Canvas On Water Management in BengaluruDocument11 pagesBusiness Analytics Canvas On Water Management in BengaluruJyothish JbNo ratings yet

- Case Study of CitigroupDocument4 pagesCase Study of CitigroupMohil NaikNo ratings yet

- Top US Banks and Financial CompaniesDocument25 pagesTop US Banks and Financial CompaniesAsif679No ratings yet

- Options For Research - You Pick Either Option A or B. Work IndividuallyDocument2 pagesOptions For Research - You Pick Either Option A or B. Work IndividuallyCherry Ann JustinianoNo ratings yet

- HUMSS - Disciplines and Ideas in Applied Social Sciences CGVVVVDocument7 pagesHUMSS - Disciplines and Ideas in Applied Social Sciences CGVVVVPaul Edward MacombNo ratings yet

- "Id, Ego, Superego": Freud Lesson Plan Nicole Giovagnoli HPS 3003, Fall 2012 Dr. Robert Hatch 18 November 2012Document4 pages"Id, Ego, Superego": Freud Lesson Plan Nicole Giovagnoli HPS 3003, Fall 2012 Dr. Robert Hatch 18 November 2012Cherry Ann JustinianoNo ratings yet

- Instructional Plan: 1. Objectives Knowledge Skills Attitude Values 2. Content 3. Learning Resources ProcedureDocument1 pageInstructional Plan: 1. Objectives Knowledge Skills Attitude Values 2. Content 3. Learning Resources ProcedureCherry Ann JustinianoNo ratings yet

- Registration Form - Federation of Philippine American Chamber of Commerce (FPACC) Bi-National Conference, Los Angeles, CADocument1 pageRegistration Form - Federation of Philippine American Chamber of Commerce (FPACC) Bi-National Conference, Los Angeles, CALorna DietzNo ratings yet

- ICICI Bank HPCL Coral Credit Card Membership GuideDocument17 pagesICICI Bank HPCL Coral Credit Card Membership Guidepalleti253No ratings yet

- Car & Motorcycle: Manheim Account Buyer FeesDocument7 pagesCar & Motorcycle: Manheim Account Buyer FeesJames PatchettNo ratings yet

- Rs. 39,200/-Rs. 39,200/ - Rs. 39,200Document1 pageRs. 39,200/-Rs. 39,200/ - Rs. 39,200Real ManNo ratings yet

- Payment InstructionsDocument3 pagesPayment InstructionsNour shawaNo ratings yet

- Miss Washington Identity Theft Chargin DocsDocument5 pagesMiss Washington Identity Theft Chargin DocsMatt DriscollNo ratings yet

- Price Modules GSMDocument75 pagesPrice Modules GSMbob6215No ratings yet

- Job Satisfaction at NABIL BankDocument22 pagesJob Satisfaction at NABIL BankDevKumar MahatoNo ratings yet

- Pakistan Formaldehyde Market Outlook 2020: AbstractsDocument6 pagesPakistan Formaldehyde Market Outlook 2020: AbstractsimtiazNo ratings yet

- Bank statement history overviewDocument5 pagesBank statement history overviewDenis ZuzNo ratings yet

- Summary Sales Report Kks p2Document1 pageSummary Sales Report Kks p2hrcitraseleragroupNo ratings yet

- Mauritius Commercial Bank Corporates RatesDocument6 pagesMauritius Commercial Bank Corporates RatesGilbert KoopoosamychettyNo ratings yet

- Yazz Frequently Asked Questions: What Is A YAZZ Card?Document6 pagesYazz Frequently Asked Questions: What Is A YAZZ Card?Krizna VargasNo ratings yet

- Chapter 9.docpart 1 FinalDocument15 pagesChapter 9.docpart 1 FinalRabie HarounNo ratings yet

- AgentCalcs Software Order Form - Jensen HughesDocument2 pagesAgentCalcs Software Order Form - Jensen HughesPaulo MaresNo ratings yet

- What Is CurrencyDocument9 pagesWhat Is CurrencyTabish KhanNo ratings yet

- Certificado Servicios Médicos de Emergencia Internacional (10112022)Document4 pagesCertificado Servicios Médicos de Emergencia Internacional (10112022)TeNo ratings yet

- E PaymentDocument42 pagesE PaymentSachin Aggarwal0% (1)

- Current Affairs Weekly PDF - October 2020 1st Week (1-8) by AffairsCloudDocument22 pagesCurrent Affairs Weekly PDF - October 2020 1st Week (1-8) by AffairsCloudMahesh BabuNo ratings yet

- Scarb Fun GuideDocument118 pagesScarb Fun GuideSangeethaNo ratings yet

- Loyalist College Program Availability List For JAN - 2023 Intake 240522Document6 pagesLoyalist College Program Availability List For JAN - 2023 Intake 240522Jayrajsinh ParmarNo ratings yet

- SCB Tariff 2021Document15 pagesSCB Tariff 2021Fuaad DodooNo ratings yet