You might also like

- Law and Practice of International FinanceDocument9 pagesLaw and Practice of International FinanceCarlos Belando PastorNo ratings yet

- Chapter 10Document32 pagesChapter 10sdfklmjsdlklskfjdNo ratings yet

- Chap 013Document19 pagesChap 013Xeniya Morozova Kurmayeva100% (1)

- Dream Construction Profile 9.9Document8 pagesDream Construction Profile 9.9virNo ratings yet

- ADB - Organizational ChartDocument1 pageADB - Organizational Chartsern soon0% (1)

- Cap 13 Managing Nondeposit and Borrowed FundsDocument13 pagesCap 13 Managing Nondeposit and Borrowed FundsJared QuinnNo ratings yet

- Deposit Sources of FundsDocument6 pagesDeposit Sources of FundsSakib Chowdhury0% (1)

- When Deposits and Other Cash Flows Are InadequateDocument2 pagesWhen Deposits and Other Cash Flows Are InadequateSwaraj AnandNo ratings yet

- Money MarketsDocument11 pagesMoney MarketsRonah Abigail BejocNo ratings yet

- BBA2030493Document14 pagesBBA2030493Saad AhmedNo ratings yet

- Chapter 2 Tutorial AnswersDocument5 pagesChapter 2 Tutorial AnswersHeri LimNo ratings yet

- Saving Institution by Baqir Siddique: History of Saving CompanyDocument4 pagesSaving Institution by Baqir Siddique: History of Saving Companym.bqairNo ratings yet

- Bank BalancesheetDocument10 pagesBank BalancesheetwubeNo ratings yet

- Unit 3: Commercial Bank Sources of Funds: 1. Transaction DepositsDocument9 pagesUnit 3: Commercial Bank Sources of Funds: 1. Transaction Depositsመስቀል ኃይላችን ነውNo ratings yet

- Managing and Pricing Deposit Services: 2.1 Types PF DepositsDocument10 pagesManaging and Pricing Deposit Services: 2.1 Types PF Depositsadela simionovNo ratings yet

- Chapter 2Document28 pagesChapter 2mokeNo ratings yet

- Check Negotiable Instrument Check Promissory Note DrawerDocument7 pagesCheck Negotiable Instrument Check Promissory Note DrawerghnyerNo ratings yet

- Chapter 5 FIMDocument13 pagesChapter 5 FIMMintayto TebekaNo ratings yet

- Loan Scheme Vis-A-Vis Others": "Comparative Study of Sbi CarDocument69 pagesLoan Scheme Vis-A-Vis Others": "Comparative Study of Sbi CarStar0% (1)

- The Repo MarketDocument16 pagesThe Repo MarketmeetozaNo ratings yet

- Life Insurance: Financial Institution Savings MortgageDocument2 pagesLife Insurance: Financial Institution Savings MortgageAshrafulNo ratings yet

- Money Market FundDocument3 pagesMoney Market FundnegosyomailNo ratings yet

- Quiz 3 MidtermDocument4 pagesQuiz 3 MidtermAlicia Dawn A. OlimbaNo ratings yet

- Quiz 3 MidtermDocument4 pagesQuiz 3 MidtermAlicia Dawn A. OlimbaNo ratings yet

- Commercial BankingDocument76 pagesCommercial BankingchingNo ratings yet

- 1212051354772046banking Terminologies (Expected and Selected Terms)Document4 pages1212051354772046banking Terminologies (Expected and Selected Terms)Ashad R ReghuNo ratings yet

- BFS - U2Document44 pagesBFS - U2Abijith K SNo ratings yet

- Banking ArrangementsDocument3 pagesBanking ArrangementsJyoti LalwaniNo ratings yet

- FMR Tutorial 3Document3 pagesFMR Tutorial 3Sarah LeeNo ratings yet

- Types of Money Market InstrumentsDocument6 pagesTypes of Money Market Instrumentsrabia liaqatNo ratings yet

- 04 Uses of Fund PDFDocument7 pages04 Uses of Fund PDFSuraj SurajNo ratings yet

- Chapter 13 - Managing Nondeposit LiabilitiesDocument16 pagesChapter 13 - Managing Nondeposit LiabilitiesAhmed El KhateebNo ratings yet

- Lim Yew Joon B19080668 FMI Tutorial 4Document7 pagesLim Yew Joon B19080668 FMI Tutorial 4Jing HangNo ratings yet

- Sources of BorrowingsDocument5 pagesSources of BorrowingsAruna SriNo ratings yet

- Management of The ShortDocument13 pagesManagement of The ShortShivaraman ShankarNo ratings yet

- FIN 4324 Final Exam Study GuideDocument32 pagesFIN 4324 Final Exam Study GuideNicholas GiaquintoNo ratings yet

- Lecture 3 - Loans - AdvancesDocument16 pagesLecture 3 - Loans - AdvancesYvonneNo ratings yet

- Chapter 14 The Mortgage MarketsDocument5 pagesChapter 14 The Mortgage Marketslasha Kachkachishvili100% (1)

- Acc For Financial Institutions AssignmentDocument3 pagesAcc For Financial Institutions AssignmentDina AlfawalNo ratings yet

- Money Markets and Capital MarketsDocument4 pagesMoney Markets and Capital MarketsEmmanuelle RojasNo ratings yet

- Money Market - A BriefDocument6 pagesMoney Market - A BriefasfaarsafiNo ratings yet

- FIN204 AnswersDocument9 pagesFIN204 Answerssiddhant jainNo ratings yet

- Money Market Financial InstrumentsDocument5 pagesMoney Market Financial InstrumentsmaryaniNo ratings yet

- 1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemDocument8 pages1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemAyanda Yan'Dee DimphoNo ratings yet

- Background On Mortgages: Mortgage MarketsDocument7 pagesBackground On Mortgages: Mortgage MarketsPaw VerdilloNo ratings yet

- Financial Markets (Chapter 8)Document4 pagesFinancial Markets (Chapter 8)Kyla DayawonNo ratings yet

- Corporate BankingDocument6 pagesCorporate BankingDeven RanaNo ratings yet

- Is Shadow Banking Really BankingDocument16 pagesIs Shadow Banking Really BankingBlackSeaTimesNo ratings yet

- 3.foreign Loan SyndicationDocument19 pages3.foreign Loan SyndicationAPOLLO BISWASNo ratings yet

- CHAP - 04 - Managing and Pricing Non-Deposit LiabilitiesDocument52 pagesCHAP - 04 - Managing and Pricing Non-Deposit LiabilitiesTran Thanh NganNo ratings yet

- Repo Vs Reverse RepoDocument16 pagesRepo Vs Reverse Repogupta_rajesh_621791No ratings yet

- Chapter Three Interest Rate, Its Structure and How It's DeterminedDocument29 pagesChapter Three Interest Rate, Its Structure and How It's Determinednihal zidanNo ratings yet

- Interbank Lending MarketDocument7 pagesInterbank Lending Markettimothy454No ratings yet

- Finance GlossaryDocument10 pagesFinance GlossaryhumaidjafriNo ratings yet

- Lecture 3 - Loans & AdvancesDocument16 pagesLecture 3 - Loans & AdvancesEmmanuel MwapeNo ratings yet

- Bonds and Interest RateDocument31 pagesBonds and Interest Rateeiraj hashemiNo ratings yet

- Chapter 10-11-1Document18 pagesChapter 10-11-1fouad.mlwbdNo ratings yet

- Bbs Thesis 4 TH Year FinalDocument42 pagesBbs Thesis 4 TH Year FinalBINOD POUDEL100% (2)

- MortgageDocument88 pagesMortgagejhanu jhanuNo ratings yet

- Chap013 1Document5 pagesChap013 1linhkhanh2038No ratings yet

- Tutorial 1 QuestionsDocument8 pagesTutorial 1 QuestionsHuế HoàngNo ratings yet

- Business Math HandbookDocument48 pagesBusiness Math HandbookabeerNo ratings yet

- BankDocument25 pagesBankabeerNo ratings yet

- ARTS 1203 Terms&DefinitionsDocument2 pagesARTS 1203 Terms&DefinitionsabeerNo ratings yet

- BNFN 4309 - Topic 2 (Activity # 3) - AKDocument18 pagesBNFN 4309 - Topic 2 (Activity # 3) - AKabeerNo ratings yet

- BNFN 3303 - Activity # 1Document1 pageBNFN 3303 - Activity # 1abeerNo ratings yet

- Banks-Class Activities-ChDocument6 pagesBanks-Class Activities-ChabeerNo ratings yet

- Marketing Analsyis For Fish Farming BusinessDocument12 pagesMarketing Analsyis For Fish Farming BusinessNabeel AhmadNo ratings yet

- Content Overview and OnboardingDocument29 pagesContent Overview and OnboardingMaria AngelNo ratings yet

- 2.2 - Decades of Research On Foreign Subsidiary Divestment, What Do We Really Know About Its AntecedentsDocument18 pages2.2 - Decades of Research On Foreign Subsidiary Divestment, What Do We Really Know About Its AntecedentsNabila HanaraniaNo ratings yet

- Module 10 PAS 33Document4 pagesModule 10 PAS 33Jan JanNo ratings yet

- D001403520 Rev A TCD For iCT Upgardes CN9ADocument71 pagesD001403520 Rev A TCD For iCT Upgardes CN9ASrini Vasan L RNo ratings yet

- Advanced Manufacturing Tutorial AnswersDocument12 pagesAdvanced Manufacturing Tutorial Answerswilfred chipanguraNo ratings yet

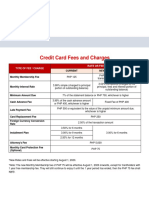

- Credit Card Fees and Charges: Type of Fee / Charge Rate or FeeDocument1 pageCredit Card Fees and Charges: Type of Fee / Charge Rate or FeeKram Yer EtentepmocNo ratings yet

- Consumer Reactions To Sustainable PackagingDocument10 pagesConsumer Reactions To Sustainable Packagingxi si xingNo ratings yet

- GST Accounting Entries in Tally - Sales and PurchasesDocument39 pagesGST Accounting Entries in Tally - Sales and PurchasesNeelu100% (1)

- Money-Time Relationships and EquivalenceDocument22 pagesMoney-Time Relationships and EquivalenceKorinaVargas0% (1)

- Case Analysis AvonDocument4 pagesCase Analysis AvonRaj Paroha83% (6)

- ME76 Comprehensive Guidelines For The Graduating StudentsDocument8 pagesME76 Comprehensive Guidelines For The Graduating StudentsDanielle Angela TaccadNo ratings yet

- Transition RailsDocument2 pagesTransition RailsteedNo ratings yet

- Name: - Date: - Grade Level & SectionDocument11 pagesName: - Date: - Grade Level & SectionCynthia Santos100% (1)

- Intermediate Accounting 2 (Notes Payable) - Problem 2Document3 pagesIntermediate Accounting 2 (Notes Payable) - Problem 2DM MontefalcoNo ratings yet

- Recruitment Case StudyDocument12 pagesRecruitment Case Studyarchangelkhel100% (1)

- Rockwell Deep Freezer InvoiceDocument2 pagesRockwell Deep Freezer InvoiceKuldeep KushwahaNo ratings yet

- IESBA English 2021 IESBA Handbook WebDocument342 pagesIESBA English 2021 IESBA Handbook WebSabina GartaulaNo ratings yet

- Iron CastingsDocument49 pagesIron Castingsmathias alfred jeschke lopezNo ratings yet

- Lean, Sustainability and The Triple Bottom Line Performance - A Systems Perspective-Based Empirical ExaminationDocument21 pagesLean, Sustainability and The Triple Bottom Line Performance - A Systems Perspective-Based Empirical ExaminationAhmed HassanNo ratings yet

- Break-Even Level of Output BUSINESS STUDIES IGCSEDocument3 pagesBreak-Even Level of Output BUSINESS STUDIES IGCSEHriday KotechaNo ratings yet

- MGT-513 Corporate Law Course ContentDocument4 pagesMGT-513 Corporate Law Course Contentsheraz akramNo ratings yet

- Welfare ProvisionsDocument28 pagesWelfare ProvisionsMalik Khuram ShazadNo ratings yet

- 2 - Dilemma in Hiring PDFDocument5 pages2 - Dilemma in Hiring PDFmanik singhNo ratings yet

- CH 15Document56 pagesCH 15Quỳnh Anh Bùi ThịNo ratings yet

- HR Analytics LTPCHR S 3 1 0 4 60: After Completion of The Course, The Students Will Be Able ToDocument2 pagesHR Analytics LTPCHR S 3 1 0 4 60: After Completion of The Course, The Students Will Be Able ToMurugan MNo ratings yet

- Company Land OwnershipDocument4 pagesCompany Land Ownershipmartin ottoNo ratings yet

- SAP Modul PM - 01 Maintenance Overview & SAP NavigationDocument23 pagesSAP Modul PM - 01 Maintenance Overview & SAP NavigationkevinkepedNo ratings yet