You might also like

- Supreme Court Eminent Domain Case 09-381 Denied Without OpinionFrom EverandSupreme Court Eminent Domain Case 09-381 Denied Without OpinionNo ratings yet

- UST Taxation Law - Hernando Case DigestsDocument47 pagesUST Taxation Law - Hernando Case DigestsLuis NovalNo ratings yet

- FDDA Requirements and Tax Assessment ValidityDocument2 pagesFDDA Requirements and Tax Assessment ValidityKaren Mae ServanNo ratings yet

- Commissioner of Internal Revenue Vs Philippine Daily InquirerDocument2 pagesCommissioner of Internal Revenue Vs Philippine Daily Inquireranon100% (1)

- CIR Vs Pineda DigestDocument1 pageCIR Vs Pineda DigestRoz Lourdiz CamachoNo ratings yet

- CIR vs. Standard Chartered Bank Prescription RulingDocument2 pagesCIR vs. Standard Chartered Bank Prescription RulingGladys Bustria Orlino0% (1)

- Case DigestDocument6 pagesCase DigestGabriel Jhick SaliwanNo ratings yet

- Asian Transmission Corp. vs. CIRDocument2 pagesAsian Transmission Corp. vs. CIRRhea Caguete50% (2)

- G.R. No. 230861 September 19, 2018 Asian Transmission Corporation V. Commissioner of Internal RevenueDocument2 pagesG.R. No. 230861 September 19, 2018 Asian Transmission Corporation V. Commissioner of Internal Revenuefallon caringtonNo ratings yet

- CIR v. Kudos Metal Corporation, G.R. No. 178087 Dated May 5, 2010.Document2 pagesCIR v. Kudos Metal Corporation, G.R. No. 178087 Dated May 5, 2010.brendamanganaanNo ratings yet

- G.R. No. 230443Document13 pagesG.R. No. 230443Ran Ngi100% (1)

- 2010-2015 Bar Tax Q&aDocument104 pages2010-2015 Bar Tax Q&aMicah Ruth PascuaNo ratings yet

- V:/F'Ftmaj: Upreme OurtDocument12 pagesV:/F'Ftmaj: Upreme OurtShiela BorjaNo ratings yet

- #45 - CIR vs. Next Mobile Inc.-Delos ReyesDocument2 pages#45 - CIR vs. Next Mobile Inc.-Delos ReyesMilesNo ratings yet

- CIR Vs Transitions Optical PhilippinesDocument2 pagesCIR Vs Transitions Optical PhilippinesJuls Rxs100% (1)

- Cir Vs Standard CharteredDocument1 pageCir Vs Standard CharteredJeng RoqueNo ratings yet

- CIR vs. La Flor Isabela 211289Document1 pageCIR vs. La Flor Isabela 211289magen100% (1)

- Quiz Week 2 No AnswerDocument10 pagesQuiz Week 2 No AnswerKatherine EderosasNo ratings yet

- CIR Vs La FlorDocument8 pagesCIR Vs La FlorJoshua Erik MadriaNo ratings yet

- CIR vs. Kudos Metal CorpDocument2 pagesCIR vs. Kudos Metal CorpEnav LucuddaNo ratings yet

- Cir VS La Flor PDFDocument3 pagesCir VS La Flor PDFGrazielNo ratings yet

- Asian Transmission Vs CIR - Case DigestDocument1 pageAsian Transmission Vs CIR - Case DigestKaren Mae ServanNo ratings yet

- CIR vs. La Flor dela IsabelaDocument10 pagesCIR vs. La Flor dela IsabelaJela KateNo ratings yet

- CTA Affirms Cancellation of Tax Assessments Due to PrescriptionDocument13 pagesCTA Affirms Cancellation of Tax Assessments Due to PrescriptionChristopher ArellanoNo ratings yet

- E-Library - Information At Your Fingertips: Printer FriendlyDocument11 pagesE-Library - Information At Your Fingertips: Printer Friendlyyan_saavedra_1No ratings yet

- 153.CIR Vs La FlorDocument9 pages153.CIR Vs La FlorClyde KitongNo ratings yet

- CIR V La Flor Dela IsabelaDocument9 pagesCIR V La Flor Dela Isabelasteth16No ratings yet

- Commissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., RespondentDocument9 pagesCommissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., Respondentkristel jane caldozaNo ratings yet

- Commissioner of Internal Revenue, Petitioner, V. La Flor Dela Isabela, Inc., Respondent. DecisionDocument7 pagesCommissioner of Internal Revenue, Petitioner, V. La Flor Dela Isabela, Inc., Respondent. DecisionFrancis Coronel Jr.No ratings yet

- Second Division: Petitioner vs. vs. RespondentDocument5 pagesSecond Division: Petitioner vs. vs. RespondentDenise GordonNo ratings yet

- CIR vs. La FlorDocument13 pagesCIR vs. La FlorKim RoqueNo ratings yet

- CIR vs. La FlorDocument13 pagesCIR vs. La FlorAngel VirayNo ratings yet

- S9upreme QI:ourt: L/epublic of Tbe !lbilippinegDocument14 pagesS9upreme QI:ourt: L/epublic of Tbe !lbilippinegKim RoqueNo ratings yet

- Cir Vs La Flor Re: Prescriptive Period FactsDocument3 pagesCir Vs La Flor Re: Prescriptive Period FactsGrazielNo ratings yet

- La Flor Dela Isabela v. CIRDocument8 pagesLa Flor Dela Isabela v. CIRCarla DomingoNo ratings yet

- CIR V Next MobileDocument5 pagesCIR V Next MobilecarolNo ratings yet

- CTA Ruling on Tax Assessments Against CorporationDocument17 pagesCTA Ruling on Tax Assessments Against CorporationLyn Jeen BinuaNo ratings yet

- Petitioner vs. vs. Respondent: Third DivisionDocument9 pagesPetitioner vs. vs. Respondent: Third DivisionEdmart VicedoNo ratings yet

- CIR vs. Petron, G. R. No. 185568 (2012)Document14 pagesCIR vs. Petron, G. R. No. 185568 (2012)Aaron James PuasoNo ratings yet

- CIR v. Jerry OcierDocument11 pagesCIR v. Jerry OcierJohn FerarenNo ratings yet

- Case Digest Atty CabaneiroDocument11 pagesCase Digest Atty CabaneiroChriselle Marie DabaoNo ratings yet

- CIR v. PDI Tax RulingDocument6 pagesCIR v. PDI Tax RulingFrancisCarloL.FlameñoNo ratings yet

- ATC tax case hinges on contributory fault estoppelDocument6 pagesATC tax case hinges on contributory fault estoppelLyn Jeen BinuaNo ratings yet

- CTA En Banc upholds taxpayer's petitionDocument10 pagesCTA En Banc upholds taxpayer's petitionKempetsNo ratings yet

- CTA Rules in Favor of Jewelry Firm in Tax CaseDocument8 pagesCTA Rules in Favor of Jewelry Firm in Tax CaseJavieNo ratings yet

- Petitioner Vs Vs Respondent: Second DivisionDocument10 pagesPetitioner Vs Vs Respondent: Second DivisionAriel MolinaNo ratings yet

- Petitioner RespondentsDocument11 pagesPetitioner RespondentsDanielle AndrinNo ratings yet

- CTA upholds cancellation of tax assessmentsDocument10 pagesCTA upholds cancellation of tax assessmentsPio Vincent BuencaminoNo ratings yet

- CTA upholds BIR assessment of expanded withholding tax for 1998Document16 pagesCTA upholds BIR assessment of expanded withholding tax for 1998henzencameroNo ratings yet

- Juson Vs COA BACDocument6 pagesJuson Vs COA BACSarah Jane BehigaNo ratings yet

- Cir v. Kudos MetalDocument8 pagesCir v. Kudos MetalDis CatNo ratings yet

- (G.R. No. 202105. April 28, 2021) La Flor Del Isabela Vs CIR HernandoDocument17 pages(G.R. No. 202105. April 28, 2021) La Flor Del Isabela Vs CIR HernandoChatNo ratings yet

- CA Affirms Award to Subcontractor But Modifies Interest and FeesDocument22 pagesCA Affirms Award to Subcontractor But Modifies Interest and FeesDaniel AbecinaNo ratings yet

- 22) ASIAN TRANSMISSION Vs CIR - J.BersaminDocument5 pages22) ASIAN TRANSMISSION Vs CIR - J.BersaminStalin LeningradNo ratings yet

- CIR v. Kudos MetalDocument2 pagesCIR v. Kudos MetalZ FNo ratings yet

- Commissioner of Internal Revenue V PetronDocument15 pagesCommissioner of Internal Revenue V PetronMaya Angelique JajallaNo ratings yet

- 56 - CIR V PetronDocument11 pages56 - CIR V PetronRomy Ian LimNo ratings yet

- 96 - CIR v. Next Mobile - de LunaDocument2 pages96 - CIR v. Next Mobile - de LunaVon Lee De LunaNo ratings yet

- Set 2 CasesDocument167 pagesSet 2 CasesElaine TalubanNo ratings yet

- CTA upholds cancellation of tax assessmentsDocument27 pagesCTA upholds cancellation of tax assessmentsVictoria aytonaNo ratings yet

- Commissioner On Internal Revenue vs. CADocument5 pagesCommissioner On Internal Revenue vs. CAIelBarnacheaNo ratings yet

- February 22, 2017 G.R. No. 221590 Commissioner of Internal Revenue, Petitioner ASALUS CORPORATION, Respondent Decision Mendoza, J.Document6 pagesFebruary 22, 2017 G.R. No. 221590 Commissioner of Internal Revenue, Petitioner ASALUS CORPORATION, Respondent Decision Mendoza, J.lantern san juanNo ratings yet

- G.R. No. 231581Document7 pagesG.R. No. 231581Ran NgiNo ratings yet

- Constitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveDocument15 pagesConstitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveJULIA PoncianoNo ratings yet

- Manila Court Rules Against Double Taxation Claim in Nursery Care Corp CaseDocument9 pagesManila Court Rules Against Double Taxation Claim in Nursery Care Corp CaseRan NgiNo ratings yet

- G.R. No. L-10405Document6 pagesG.R. No. L-10405Ran NgiNo ratings yet

- Tax Refund Denied Due to Irrevocable Election to Carry Over Excess PaymentsDocument10 pagesTax Refund Denied Due to Irrevocable Election to Carry Over Excess PaymentsRan NgiNo ratings yet

- G.R. No. 96541Document6 pagesG.R. No. 96541Ran NgiNo ratings yet

- Shell and Petron Tax Credit Dispute with BIRDocument18 pagesShell and Petron Tax Credit Dispute with BIRRan NgiNo ratings yet

- G.R. No. 120880Document10 pagesG.R. No. 120880Ran NgiNo ratings yet

- G.R. No. 176278Document4 pagesG.R. No. 176278Ran NgiNo ratings yet

- G.R. No. 233556Document6 pagesG.R. No. 233556Ran NgiNo ratings yet

- G.R. No. L-1276Document3 pagesG.R. No. L-1276Ran NgiNo ratings yet

- G.R. No. 169143Document13 pagesG.R. No. 169143Ran NgiNo ratings yet

- G.R. No. 148560Document93 pagesG.R. No. 148560Ran NgiNo ratings yet

- Supreme Court upholds arbitration agreement for return of TV stationDocument4 pagesSupreme Court upholds arbitration agreement for return of TV stationRan NgiNo ratings yet

- PASEI VS Sec. DrilonDocument4 pagesPASEI VS Sec. DrilonRhea Lyn MalapadNo ratings yet

- G.R. No. 152259Document20 pagesG.R. No. 152259Ran NgiNo ratings yet

- G.R. No. 92163Document23 pagesG.R. No. 92163Ran NgiNo ratings yet

- G.R. No. 117577Document11 pagesG.R. No. 117577Ran NgiNo ratings yet

- G.R. No. 106719Document7 pagesG.R. No. 106719Ran NgiNo ratings yet

- Supreme Court Rules Promotion Schemes Not LotteriesDocument2 pagesSupreme Court Rules Promotion Schemes Not LotteriesRan NgiNo ratings yet

- Supreme Court Rules Promotion Schemes Not LotteriesDocument2 pagesSupreme Court Rules Promotion Schemes Not LotteriesRan NgiNo ratings yet

- G.R. No. 169143Document13 pagesG.R. No. 169143Ran NgiNo ratings yet

- Caltex Hooded Pump Contest Does Not Violate Postal LawDocument7 pagesCaltex Hooded Pump Contest Does Not Violate Postal LawRan NgiNo ratings yet

- Supreme Court Rules on Illegal Arrest of LawyersDocument52 pagesSupreme Court Rules on Illegal Arrest of LawyersRan NgiNo ratings yet

- G.R. No. 117577Document11 pagesG.R. No. 117577Ran NgiNo ratings yet

- Caltex Hooded Pump Contest Does Not Violate Postal LawDocument7 pagesCaltex Hooded Pump Contest Does Not Violate Postal LawRan NgiNo ratings yet

- G.R. No. 224638Document8 pagesG.R. No. 224638Ran NgiNo ratings yet

- G.R. No. 106719Document7 pagesG.R. No. 106719Ran NgiNo ratings yet

- 15 010 International Tax Policy and Double Tax Treaties Final Web PDFDocument36 pages15 010 International Tax Policy and Double Tax Treaties Final Web PDFHanif ajalaahNo ratings yet

- Tax Exam Questions for International Taxation ClassDocument4 pagesTax Exam Questions for International Taxation ClassMichael ThaniagoNo ratings yet

- PFP Tutorial 8Document2 pagesPFP Tutorial 8stellaNo ratings yet

- Tax Accounting - DR Ahmed Sharaf - Lecture 1,2Document16 pagesTax Accounting - DR Ahmed Sharaf - Lecture 1,2Ahmed AdelNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S Chargesmozhi selvamNo ratings yet

- PDF Intermediate Accounting Volume 3 ValixDocument4 pagesPDF Intermediate Accounting Volume 3 ValixJosh Cruz CosNo ratings yet

- Zisanda Ncanywa Payslip - November - 2023Document1 pageZisanda Ncanywa Payslip - November - 2023Goitseona Koikoi IVNo ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Resolution Restoring Homestead Rebate and Senior Freeze ProgramsDocument2 pagesResolution Restoring Homestead Rebate and Senior Freeze Programsjmjr30No ratings yet

- Income Tax Act for AuditorsDocument83 pagesIncome Tax Act for AuditorsCrick CompactNo ratings yet

- Excitel Bill - August 2021 - WordDocument1 pageExcitel Bill - August 2021 - WordAshish batraNo ratings yet

- Rent invoice for borescope equipmentDocument2 pagesRent invoice for borescope equipmentRony YudaNo ratings yet

- I.7. Compensation and Set-OffDocument1 pageI.7. Compensation and Set-OffAdam Cuenca100% (1)

- ProformaDocument2 pagesProformaWORLD STARNo ratings yet

- China Banking Corporation vs. Commissioner of Internal RevenueDocument5 pagesChina Banking Corporation vs. Commissioner of Internal RevenueNash LedesmaNo ratings yet

- Gepco Online BillDocument2 pagesGepco Online BillUzair IslamNo ratings yet

- 432HW5 KeyDocument6 pages432HW5 KeyJs ParkNo ratings yet

- 02 Cp01 GBB 4 Annex ADocument7 pages02 Cp01 GBB 4 Annex AnothingmoreNo ratings yet

- 1827 PDFDocument3 pages1827 PDFhelloitskalaiNo ratings yet

- Vat Output Set A Tax 2 Class DiscussionDocument3 pagesVat Output Set A Tax 2 Class DiscussionPhilip CastroNo ratings yet

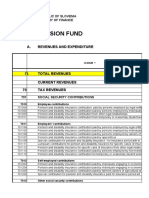

- Pension Fund 1992-2022Document9 pagesPension Fund 1992-2022DominikNo ratings yet

- M14 Taxation - Supplement For Jun and Dec 2022 SessionDocument32 pagesM14 Taxation - Supplement For Jun and Dec 2022 SessionBernice Chan Wai WunNo ratings yet

- Bir LectureDocument4 pagesBir LectureTomoko KatoNo ratings yet

- Hyderabad Electric Supply Company bill detailsDocument2 pagesHyderabad Electric Supply Company bill detailsaurang zaibNo ratings yet

- SSGC Duplicate Bill20210913 091247Document1 pageSSGC Duplicate Bill20210913 091247Aijaz AhmedNo ratings yet

- InvoiceDocument1 pageInvoiceManu Kannan G VNo ratings yet

- Enb FinalDocument11 pagesEnb Finalkevin kipkemoiNo ratings yet