You might also like

- Business Services Class 11 Notes Business Studies - 7114551Document8 pagesBusiness Services Class 11 Notes Business Studies - 7114551TanishqNo ratings yet

- CH 4Document10 pagesCH 4RaashiNo ratings yet

- Nature of Business Serv1cesDocument11 pagesNature of Business Serv1cesmadhavanramuduNo ratings yet

- CH 4Document5 pagesCH 4Ashvin GuptaNo ratings yet

- CH 4 Business ServicesDocument13 pagesCH 4 Business ServicesBaklol Babu JiNo ratings yet

- 11 Business Studies Notes Ch04 Business Services 02Document12 pages11 Business Studies Notes Ch04 Business Services 02Subodh SaxenaNo ratings yet

- Business Servicesnotes 2022Document15 pagesBusiness Servicesnotes 2022fearlessdevil25No ratings yet

- Important Functions of Bank: What Is A Bank?Document3 pagesImportant Functions of Bank: What Is A Bank?Samiksha PawarNo ratings yet

- Commercial BankingDocument12 pagesCommercial BankingwubeNo ratings yet

- Functions of BanksDocument3 pagesFunctions of BanksEbne FahadNo ratings yet

- CH 4 Business ServicesDocument11 pagesCH 4 Business Serviceskeshav sarafNo ratings yet

- Chapter 4 - Business ServicesDocument12 pagesChapter 4 - Business Servicestayalaryaman751No ratings yet

- CH-4 Business Services MLPDocument5 pagesCH-4 Business Services MLPֆաǟʍɛʋ ɢʊքƭǟNo ratings yet

- ch-1 SummryDocument3 pagesch-1 SummryGiven GivenNo ratings yet

- Banking Functions and RelationshipsDocument28 pagesBanking Functions and RelationshipsBi bi fathima Bi bi fathimaNo ratings yet

- Commercial Bank FunctionsDocument29 pagesCommercial Bank FunctionsMahesh RasalNo ratings yet

- 2-Notes On Banking Products & Services-Part 1Document16 pages2-Notes On Banking Products & Services-Part 1Kirti GiyamalaniNo ratings yet

- Commercial Banks' General Services & Agency FunctionsDocument10 pagesCommercial Banks' General Services & Agency FunctionsSharan YadavNo ratings yet

- Banking Functions and ServicesDocument7 pagesBanking Functions and ServicesMitali aroraNo ratings yet

- Chapter 5 EditedDocument10 pagesChapter 5 EditedSeid KassawNo ratings yet

- banking ecoDocument27 pagesbanking ecomayankgoylllNo ratings yet

- Banking Law and PracticeDocument25 pagesBanking Law and PracticePRASHANT REVANKARNo ratings yet

- Banking Theory Law & Practice GuideDocument22 pagesBanking Theory Law & Practice GuidePraveen CoolNo ratings yet

- Chapter - : Money and Banking: Best Higher Secondary SchoolDocument11 pagesChapter - : Money and Banking: Best Higher Secondary Schoolapi-232747878No ratings yet

- Management of Commercial BankDocument7 pagesManagement of Commercial BankSamridhi RakhejaNo ratings yet

- Banking LawDocument63 pagesBanking Lawpraveen ramanjaneyaluNo ratings yet

- (A.) Commercial Banks - FunctionsDocument3 pages(A.) Commercial Banks - FunctionsEPP-2004 HaneefaNo ratings yet

- Reading Advancing Functions of BankDocument2 pagesReading Advancing Functions of BankKim DungNo ratings yet

- Functions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsDocument3 pagesFunctions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsBalaji GajendranNo ratings yet

- Chapter Three Commercial Banking: 1 by SityDocument10 pagesChapter Three Commercial Banking: 1 by SitySeid KassawNo ratings yet

- Functions of Commercial BanksDocument19 pagesFunctions of Commercial BanksAravind Kumar G100% (1)

- Services Rendered by Banks.: Advancing of LoansDocument3 pagesServices Rendered by Banks.: Advancing of LoansKulgeet TanyaNo ratings yet

- I) Primary Functions:: A) Accepting DepositsDocument4 pagesI) Primary Functions:: A) Accepting DepositsJoshna SinghNo ratings yet

- Functions of Commercial BanksDocument4 pagesFunctions of Commercial BanksRajashree MuktiarNo ratings yet

- April 23 2021 12B, C, D, E, F, GChapter14BANKS NotesDocument16 pagesApril 23 2021 12B, C, D, E, F, GChapter14BANKS NotesStephine BochuNo ratings yet

- BankingDocument19 pagesBankingTipu SultanNo ratings yet

- Commercial BankingDocument4 pagesCommercial Bankingsn nNo ratings yet

- Customers and Account HoldersDocument23 pagesCustomers and Account HoldersMAHESH VNo ratings yet

- Structure of Banking in IndiaDocument22 pagesStructure of Banking in IndiaTushar Kumar 1140No ratings yet

- Lession 3 OperationsDocument13 pagesLession 3 Operationssusma susmaNo ratings yet

- Special Accounts For Banking Firm - M.com (BM) II Sem. - DR - Rajeshri DesaiDocument5 pagesSpecial Accounts For Banking Firm - M.com (BM) II Sem. - DR - Rajeshri DesaiOMARA BMF-2024100% (1)

- Chap 1. Banking System in IndiaDocument24 pagesChap 1. Banking System in IndiaShankha MaitiNo ratings yet

- Functions of Banks I Primary and SecondaryDocument6 pagesFunctions of Banks I Primary and SecondaryAmace Placement KanchipuramNo ratings yet

- FMM Acct For Business Ch2Document9 pagesFMM Acct For Business Ch2swati_chindarkar17No ratings yet

- Private Sector BanksDocument3 pagesPrivate Sector BanksBalaji GajendranNo ratings yet

- E BankingDocument65 pagesE Bankingzeeshan shaikh100% (1)

- Function of Commercial BankDocument7 pagesFunction of Commercial BankEmranul Islam ShovonNo ratings yet

- Banking Services IntroductionDocument45 pagesBanking Services IntroductionRaghu BMNo ratings yet

- Banks: Deposits AccountsDocument11 pagesBanks: Deposits AccountsMukesh AroraNo ratings yet

- They Do Not Provide, Long-Term CreditDocument5 pagesThey Do Not Provide, Long-Term CreditalemayehuNo ratings yet

- What Is BankDocument19 pagesWhat Is BankSunayana BasuNo ratings yet

- FUNCTIONS OF COMMERCIAL BANKSDocument16 pagesFUNCTIONS OF COMMERCIAL BANKSJayant MishraNo ratings yet

- 5banking Law - NotesDocument80 pages5banking Law - NotesSalman MSDNo ratings yet

- Banking Pricnciples and Practices Lecture Notes ch3Document17 pagesBanking Pricnciples and Practices Lecture Notes ch3ejigu nigussieNo ratings yet

- A. Primary Functions of BanksDocument15 pagesA. Primary Functions of Bankshansdeep479No ratings yet

- Banking - ch-3333Document13 pagesBanking - ch-3333FantayNo ratings yet

- Commercial Banks Chapter 1 SlidesDocument30 pagesCommercial Banks Chapter 1 SlidesFatima AckermanNo ratings yet

- Assign3 Fin323Document3 pagesAssign3 Fin323mark_torreonNo ratings yet

- Chapter 13 BankingDocument5 pagesChapter 13 BankingdragongskdbsNo ratings yet

- BANK UnlockedDocument6 pagesBANK UnlockedRaghav Sharma100% (1)

- On Opening Bank AccountDocument15 pagesOn Opening Bank AccountSaroj Patil79% (14)

- Understanding Customer Investment Preferences in PuneDocument36 pagesUnderstanding Customer Investment Preferences in PuneRubina MansooriNo ratings yet

- Indian Investment TrendsDocument49 pagesIndian Investment TrendsRamesh AgarwalNo ratings yet

- Project ReportDocument28 pagesProject Reportsilkroute143No ratings yet

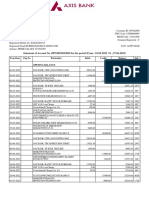

- Statement of Account No:917010065595820 For The Period (From: 01-11-2018 To: 20-06-2019)Document3 pagesStatement of Account No:917010065595820 For The Period (From: 01-11-2018 To: 20-06-2019)Rakesh BabuNo ratings yet

- A Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectDocument16 pagesA Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectFelix ChristoferNo ratings yet

- Table of Contents and Chapters of a Research Report on Mutual FundsDocument82 pagesTable of Contents and Chapters of a Research Report on Mutual Fundssaurabh dixitNo ratings yet

- April 2020Document706 pagesApril 2020Saran BaskarNo ratings yet

- 2020 A STUDY ON RECRUITMENT AND SELECTION PROCESS Research Report HRDocument63 pages2020 A STUDY ON RECRUITMENT AND SELECTION PROCESS Research Report HRanjali sikhaNo ratings yet

- Report - RBB Itahari (Yogendra Pd. Dahal)Document47 pagesReport - RBB Itahari (Yogendra Pd. Dahal)Dil Prasad RimalNo ratings yet

- Personal Financial Planning Case Study for Ahmad in 2013-2046Document50 pagesPersonal Financial Planning Case Study for Ahmad in 2013-2046Jahid Hasan100% (5)

- Functions of Commercial BanksDocument14 pagesFunctions of Commercial Banksroobhini100% (6)

- Business Studies Class 11 Project On BankingDocument10 pagesBusiness Studies Class 11 Project On BankingSubham Jaiswal100% (2)

- Kotak Mahindra Bank's NRI Banking Services ReportDocument42 pagesKotak Mahindra Bank's NRI Banking Services ReportSiddhi Mehta100% (2)

- A Study On Investors Perception Towards Investment in Stock MarketDocument75 pagesA Study On Investors Perception Towards Investment in Stock Marketjanice vaz100% (5)

- R&D BRAC Bank PDFDocument51 pagesR&D BRAC Bank PDFsohanfaisalNo ratings yet

- On Your Date of Joining, You Are Compulsorily Required ToDocument3 pagesOn Your Date of Joining, You Are Compulsorily Required Tokanna1808No ratings yet

- Types of Bank Accounts and Home Budget ProjectDocument22 pagesTypes of Bank Accounts and Home Budget ProjectShivani.S GowdaNo ratings yet

- Best Mutual Fund For SIPDocument129 pagesBest Mutual Fund For SIPRishi KumarNo ratings yet

- Aviva I LifeDocument13 pagesAviva I LifeSatyendra KumarNo ratings yet

- Banking History and ConceptsDocument29 pagesBanking History and ConceptsKARAN TRIPATHINo ratings yet

- CBE Training ManualDocument114 pagesCBE Training ManualAlex Workina86% (7)

- Analysis of Indian Stock Market and Comparision of Stock BroakersDocument56 pagesAnalysis of Indian Stock Market and Comparision of Stock BroakersmadhuNo ratings yet

- Bank of Khyber Pakistan Internship Report by Jalal KhanDocument73 pagesBank of Khyber Pakistan Internship Report by Jalal KhanJalal Khan50% (2)

- Banking Fundamentals: Types, Definitions and OriginsDocument209 pagesBanking Fundamentals: Types, Definitions and OriginsSasi Devi RamakrishnanNo ratings yet

- Internship Report ON "Foreign Exchange System of Rupali Bank Limited"Document37 pagesInternship Report ON "Foreign Exchange System of Rupali Bank Limited"Shakhauat HossainNo ratings yet

- Open Term Deposit AccountsDocument12 pagesOpen Term Deposit AccountsRaj Bahadur SinghNo ratings yet

- STUDY OF WORKING PROCESS AND INVESTMENT OPTIONS AT BAJAJ FINSERV LTDDocument29 pagesSTUDY OF WORKING PROCESS AND INVESTMENT OPTIONS AT BAJAJ FINSERV LTDshubham moonNo ratings yet

- Osmania University HYDERABAD - 500 007: Course For The Academic Year 2010-2011. The Inspection Committee Will BeDocument6 pagesOsmania University HYDERABAD - 500 007: Course For The Academic Year 2010-2011. The Inspection Committee Will BepinkpompNo ratings yet