You might also like

- Unitedhealth Care Income Statement & Balance Sheet & PE RatioDocument8 pagesUnitedhealth Care Income Statement & Balance Sheet & PE RatioEhab elhashmyNo ratings yet

- Astral delivers 73% revenue growth, 332% PBT growth in Q1Document5 pagesAstral delivers 73% revenue growth, 332% PBT growth in Q1Namrata ShahNo ratings yet

- Q4 2020 Revenue PerformanceDocument11 pagesQ4 2020 Revenue PerformanceVoiture GermanNo ratings yet

- Markaz-GL On Financial ProjectionsDocument10 pagesMarkaz-GL On Financial ProjectionsSrikanth P School of Business and ManagementNo ratings yet

- Estimated Revenues, Profits and Expenditure For Next Three YearsDocument6 pagesEstimated Revenues, Profits and Expenditure For Next Three YearsRajeev Kumar GottumukkalaNo ratings yet

- TSE's 5 Year Projection Key Drivers SummaryDocument6 pagesTSE's 5 Year Projection Key Drivers SummaryMatthew SiagianNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- Exercise 01Document4 pagesExercise 01VISHAL PATILNo ratings yet

- Assignment 5 (APM Industries) by Anil Verma (EPGP-13D-010)Document3 pagesAssignment 5 (APM Industries) by Anil Verma (EPGP-13D-010)Anil VermaNo ratings yet

- The Discounted Free Cash Flow Model For A Complete BusinessDocument2 pagesThe Discounted Free Cash Flow Model For A Complete BusinessHẬU ĐỖ NGỌCNo ratings yet

- Business ValuationDocument2 pagesBusiness Valuationahmed HOSNYNo ratings yet

- The Discounted Free Cash Flow Model For A Complete BusinessDocument2 pagesThe Discounted Free Cash Flow Model For A Complete BusinessBacarrat BNo ratings yet

- Business ValuationDocument2 pagesBusiness Valuationjrcoronel100% (1)

- Puma R To L 2020 Master 3 PublishDocument8 pagesPuma R To L 2020 Master 3 PublishIulii IuliikkNo ratings yet

- Microsoft Investment AnalysisDocument4 pagesMicrosoft Investment AnalysisdkrauzaNo ratings yet

- AVIS CarsDocument10 pagesAVIS CarsSheikhFaizanUl-HaqueNo ratings yet

- FA AnalysisDocument22 pagesFA Analysisharendra choudharyNo ratings yet

- Operational Finance Case Study: The Cardbox CompanyDocument13 pagesOperational Finance Case Study: The Cardbox CompanyJuan Ramon Aguirre Rondinel50% (2)

- Erste Group Posts Net Profit of EUR 235.3 Million in Q1 2020Document4 pagesErste Group Posts Net Profit of EUR 235.3 Million in Q1 2020Neculai CristianNo ratings yet

- Atlas Exports Limited FinalDocument22 pagesAtlas Exports Limited FinalKinza AsimNo ratings yet

- VERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Document8 pagesVERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Touqeer HussainNo ratings yet

- Gildan Model BearDocument57 pagesGildan Model BearNaman PriyadarshiNo ratings yet

- Trend and Common Size AnalysisDocument4 pagesTrend and Common Size AnalysisZuhair RiazNo ratings yet

- E603 Jumbopresentation Sept23 GRDocument11 pagesE603 Jumbopresentation Sept23 GRpithikose2tou52No ratings yet

- Capital BudgetingDocument29 pagesCapital BudgetingRAHUL DUTTANo ratings yet

- LBC Express Holdings' Financial AnalysisDocument9 pagesLBC Express Holdings' Financial AnalysisJerry ManatadNo ratings yet

- GZ R&F’s FY20 core profit -52%yoy to Rmb4.3bnDocument2 pagesGZ R&F’s FY20 core profit -52%yoy to Rmb4.3bnneil5mNo ratings yet

- Financial Overview5Document8 pagesFinancial Overview5Nishad Al Hasan SagorNo ratings yet

- IKEA Case Analysis Examines Company's Financial PerformanceDocument7 pagesIKEA Case Analysis Examines Company's Financial PerformanceJonie Ann BangahonNo ratings yet

- Five Years' Financial Summary: REPORT 2015Document2 pagesFive Years' Financial Summary: REPORT 2015Rizwan ZisanNo ratings yet

- Kahoot! (Buy TP NOK150) : The Compound Interest Effect With Triple Digit Revenue Growth and +40% FCF Margin Is Massive!Document24 pagesKahoot! (Buy TP NOK150) : The Compound Interest Effect With Triple Digit Revenue Growth and +40% FCF Margin Is Massive!jainantoNo ratings yet

- Chocolat AnalysisDocument19 pagesChocolat Analysisankitamoney1No ratings yet

- Activity 3 123456789Document7 pagesActivity 3 123456789Jeramie Sarita SumaotNo ratings yet

- 4.1.1 - Dự Báo Dòng TiềnDocument5 pages4.1.1 - Dự Báo Dòng TiềnLê TiếnNo ratings yet

- 100 BaggerDocument12 pages100 BaggerRishab WahalNo ratings yet

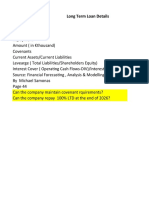

- Long Term Loan Details TermDocument67 pagesLong Term Loan Details TermPranjal GuptaNo ratings yet

- 8.+opex BeforeDocument45 pages8.+opex BeforeThe SturdyTubersNo ratings yet

- .+Energy+and+Other+gross+profit AfterDocument41 pages.+Energy+and+Other+gross+profit AfterAkash ChauhanNo ratings yet

- 6.+Energy+and+Other+revenue BeforeDocument37 pages6.+Energy+and+Other+revenue BeforeThe SturdyTubersNo ratings yet

- 6.+Energy+and+Other+Revenue AfterDocument37 pages6.+Energy+and+Other+Revenue AftervictoriaNo ratings yet

- 2.+average+of+price+models BeforeDocument23 pages2.+average+of+price+models BeforeMuskan AroraNo ratings yet

- EBS041122 enDocument4 pagesEBS041122 enNatalia MuresanNo ratings yet

- Ratio 2Document2 pagesRatio 2Mae ValenciaNo ratings yet

- Ratio 2Document2 pagesRatio 2Mae ValenciaNo ratings yet

- Financial Performance 2024Document4 pagesFinancial Performance 2024satyamjaunpur41No ratings yet

- Exhibit in ExcelDocument8 pagesExhibit in ExcelAdrian WyssNo ratings yet

- 246420231227 m 001Document16 pages246420231227 m 001danny122192No ratings yet

- UntitledDocument7 pagesUntitledberti albertiNo ratings yet

- Hero Motocorp DCF ValuationDocument66 pagesHero Motocorp DCF ValuationPrabhdeep DadyalNo ratings yet

- Investor Presentation (Company Update)Document24 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Alpine HorizontalDocument17 pagesAlpine HorizontalPraval SantarNo ratings yet

- LED ProjectDocument50 pagesLED Projectasm sauravNo ratings yet

- Horizontal and Vertical ActivityDocument4 pagesHorizontal and Vertical ActivityKarlla ManalastasNo ratings yet

- Team7 FMPhase2 Trent SENIORSDocument75 pagesTeam7 FMPhase2 Trent SENIORSNisarg Rupani100% (1)

- APECS Financial Modelling Test (Updated) - by Keng YangDocument16 pagesAPECS Financial Modelling Test (Updated) - by Keng YangDarren WongNo ratings yet

- Ratio Analysis-Overview Ratios:: CaveatsDocument18 pagesRatio Analysis-Overview Ratios:: CaveatsabguyNo ratings yet

- Suumary of Key Drivers 1.1Document6 pagesSuumary of Key Drivers 1.1Matthew SiagianNo ratings yet

- FINANCE COMPARISONDocument7 pagesFINANCE COMPARISONNienke OzingaNo ratings yet

- FinMan (Common-Size Analysis)Document4 pagesFinMan (Common-Size Analysis)Lorren Graze RamiroNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Beauty I - Individual-Assignment - Aneha200Document2 pagesBeauty I - Individual-Assignment - Aneha200Anes HNo ratings yet

- Literature Review - Group - 6-2Document11 pagesLiterature Review - Group - 6-2Anes HNo ratings yet

- E-scooter ANOVA, Correlation, Regression AnalysisDocument18 pagesE-scooter ANOVA, Correlation, Regression AnalysisAnes HNo ratings yet

- Team Bacon - IALL PresentationDocument12 pagesTeam Bacon - IALL PresentationAnes HNo ratings yet

- Team Bacon - Exploration DocumentDocument21 pagesTeam Bacon - Exploration DocumentAnes HNo ratings yet

- Assignment On Ratio Analysis: Presented byDocument5 pagesAssignment On Ratio Analysis: Presented bybhaskkarNo ratings yet

- Financial Analyses On The Various Davao City-Based CompaniesDocument24 pagesFinancial Analyses On The Various Davao City-Based CompaniesmasterdrewsNo ratings yet

- Financial Performance Analysis of Selected Indian IT Companies by Using DuPont Model PDFDocument26 pagesFinancial Performance Analysis of Selected Indian IT Companies by Using DuPont Model PDFTapesh SharmaNo ratings yet

- Kraft Foods Strategic AnalysisDocument28 pagesKraft Foods Strategic AnalysisPat JewellNo ratings yet

- Walmart Financial Ratio Analysis 2002-2003Document1 pageWalmart Financial Ratio Analysis 2002-2003Pamela WilliamsNo ratings yet

- CH 2 Ratio ProblemsDocument21 pagesCH 2 Ratio ProblemsRohith100% (1)

- Final Version Group 4-Mid Course Group AssignmentDocument22 pagesFinal Version Group 4-Mid Course Group AssignmentDiane MoutranNo ratings yet

- Titman CH 04Document151 pagesTitman CH 04Yenyensmile0% (1)

- Report of InternshipDocument31 pagesReport of InternshipHarshit GuptaNo ratings yet

- FM - EcoDocument352 pagesFM - EcoKinjal Jain100% (1)

- Financial Statement Analysis 11th Edition Subramanyam Test BankDocument48 pagesFinancial Statement Analysis 11th Edition Subramanyam Test Bankgarrotewrongerzxxo100% (29)

- RatiosDocument12 pagesRatiosstuck00123No ratings yet

- Asian Paints and Nerolac InterpretationDocument4 pagesAsian Paints and Nerolac Interpretationfebin s mathewNo ratings yet

- FP&A Interview Q TechnicalDocument17 pagesFP&A Interview Q Technicalsonu malikNo ratings yet

- Chap 05 - Residual Earnings MethodDocument35 pagesChap 05 - Residual Earnings MethodhelloNo ratings yet

- Chap 7Document27 pagesChap 7Joanne Chau100% (1)

- What Drives Bank Profitability in SpainDocument26 pagesWhat Drives Bank Profitability in Spainwrecker_scorpionNo ratings yet

- Module 4 - Financial Ratios S23Document27 pagesModule 4 - Financial Ratios S23Prachi YadavNo ratings yet

- Assessing financial performance of AEON and PARKSONDocument27 pagesAssessing financial performance of AEON and PARKSONPK LNo ratings yet

- Key Financial RatiosDocument7 pagesKey Financial RatiosDeepankumar AthiyannanNo ratings yet

- Introduction to Corporate Finance ChaptersDocument195 pagesIntroduction to Corporate Finance ChaptersFahad KhalidNo ratings yet

- Financial Analysis of AldarDocument8 pagesFinancial Analysis of AldarMuhammad HammadNo ratings yet

- Delvi IJEETDocument4 pagesDelvi IJEETihda0farhatun0nisakNo ratings yet

- FM Chapter 3Document43 pagesFM Chapter 3mariam.khaled2003No ratings yet

- Cash FlowDocument49 pagesCash FlowJudi SaiedNo ratings yet

- KPI Kroger ReportDocument25 pagesKPI Kroger ReportAbdul Qayoom100% (1)

- Financial Ratio Analysis BreakdownDocument13 pagesFinancial Ratio Analysis BreakdownA.Rahman SalahNo ratings yet

- Assignment FinanceDocument25 pagesAssignment FinanceDerp DerpingtonNo ratings yet

- Part 2 FIRST Comprehensive Exam - Section A - Qs 03 Jun 2023Document30 pagesPart 2 FIRST Comprehensive Exam - Section A - Qs 03 Jun 2023rdjimenez.auNo ratings yet

- Performance Evaluation and Ratio Analysis On Pharmaceuticals Company BangladeshDocument45 pagesPerformance Evaluation and Ratio Analysis On Pharmaceuticals Company Bangladeshfaisal216071% (7)