100% found this document useful (3 votes)

892 views14 pagesOverview of Forensic Accounting Roles

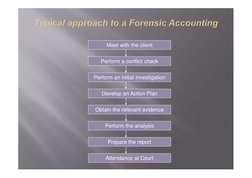

Forensic accounting involves using accounting, auditing, and investigative skills to conduct legal investigations. A forensic accountant analyzes financial evidence to help resolve disputes in a way that can be presented in a court of law. Common types of forensic accounting assignments include investigative accounting, litigation support, and analyzing fraud. The typical process involves meeting with the client, collecting evidence, analyzing finances, preparing a report, and potentially attending court to discuss the findings.

Uploaded by

Nabendu MajiCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

100% found this document useful (3 votes)

892 views14 pagesOverview of Forensic Accounting Roles

Forensic accounting involves using accounting, auditing, and investigative skills to conduct legal investigations. A forensic accountant analyzes financial evidence to help resolve disputes in a way that can be presented in a court of law. Common types of forensic accounting assignments include investigative accounting, litigation support, and analyzing fraud. The typical process involves meeting with the client, collecting evidence, analyzing finances, preparing a report, and potentially attending court to discuss the findings.

Uploaded by

Nabendu MajiCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

- What is Forensic Accounting?: Explains the integration of accounting, auditing, and investigative skills to define forensic accounting.

- Other Terminology: Discusses specialized investigations and audits within forensic accounting contexts.

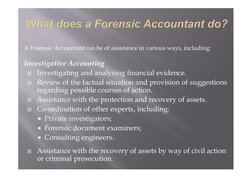

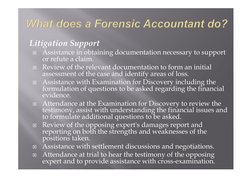

- What does a Forensic Accountant do?: Outlines the primary roles and responsibilities of a forensic accountant, emphasizing their analytical and summarization tasks.

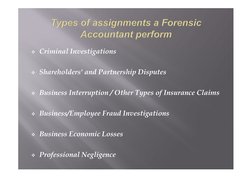

- Types of assignments a Forensic Accountant perform: Lists various tasks and assignments typically undertaken by forensic accountants.

- Typical approach to a Forensic Accounting: Describes the systematic methodology followed in forensic accounting engagements.

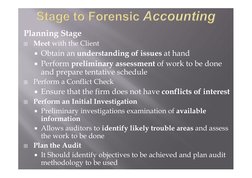

- Stage to Forensic Accounting: Details the planning and execution stages in forensic accounting procedures.

- Applications and Consequences: Examines real-world applications of forensic accounting, including a case study on fraud.