You might also like

- Investigate Fraud ChapterDocument36 pagesInvestigate Fraud ChapterNURUL SYAZWANI BINTI MOHD ZAUZINo ratings yet

- Forensic Accounting: An IntroductionDocument43 pagesForensic Accounting: An Introductionkhalid1173100% (1)

- FCMAT LosGatosDocument118 pagesFCMAT LosGatosKesslerInternationalNo ratings yet

- Defining A Forensic AuditDocument21 pagesDefining A Forensic AuditDINGDINGWALANo ratings yet

- Fatf Guidance Politically Exposed Persons (Recommendations 12 and 22) .Document36 pagesFatf Guidance Politically Exposed Persons (Recommendations 12 and 22) .Tadeo Leandro FernándezNo ratings yet

- Audit Report Malawi PDFDocument52 pagesAudit Report Malawi PDFJohn Richard KasalikaNo ratings yet

- The Five Letter F Word: Fraud in The Hospitality Industry: Topics For DiscussionDocument21 pagesThe Five Letter F Word: Fraud in The Hospitality Industry: Topics For Discussionmohamed12345No ratings yet

- Profiles of The FraudsterDocument28 pagesProfiles of The FraudsterBackUp 02No ratings yet

- INT Inside Fraud Text 090909Document64 pagesINT Inside Fraud Text 090909carlosfigdir2605No ratings yet

- Managing The Business Risk of FraudDocument256 pagesManaging The Business Risk of FraudisyarayNo ratings yet

- IA's Role in Risk Management-DownloadDocument18 pagesIA's Role in Risk Management-DownloadVick JoadNo ratings yet

- Chap1-Overview of Computer Forensic TechnologyDocument23 pagesChap1-Overview of Computer Forensic TechnologyMA RKNo ratings yet

- SEA Investigations WOrkshop Session 4 - Gathering InformationDocument53 pagesSEA Investigations WOrkshop Session 4 - Gathering InformationInterActionNo ratings yet

- Helix Opensource User Manual PDFDocument202 pagesHelix Opensource User Manual PDFDave GordonNo ratings yet

- Dealing With White Collar CrimeDocument70 pagesDealing With White Collar CrimeAndrew FordredNo ratings yet

- Members Names OnlyDocument3 pagesMembers Names Onlyapi-250361062No ratings yet

- Artificial Intelligence With SasDocument141 pagesArtificial Intelligence With SasSulist SulistNo ratings yet

- List of Registered ProfessionalsDocument45 pagesList of Registered ProfessionalsMike MatshonaNo ratings yet

- Report 11 - Forensic Audit Report - Establishment PhaseDocument28 pagesReport 11 - Forensic Audit Report - Establishment PhaseRush OunzaNo ratings yet

- Chapter 17Document21 pagesChapter 17Talia AdaNo ratings yet

- Computer Fraud & AbuseDocument45 pagesComputer Fraud & AbuseBear CooporNo ratings yet

- ForensicDocument40 pagesForensicAnil Kumar ThakurNo ratings yet

- 2019 Internet Crime ReportDocument28 pages2019 Internet Crime ReportNewsChannel 9No ratings yet

- Forensic Audit Report RFP 1 On CBSL Bond ScamDocument179 pagesForensic Audit Report RFP 1 On CBSL Bond ScamRivira Media75% (4)

- Introduction Forensic Audit ReportingDocument16 pagesIntroduction Forensic Audit ReportingChristen CastilloNo ratings yet

- Occupational Fraud Detection and PreventionDocument33 pagesOccupational Fraud Detection and PreventionNicole SiaNo ratings yet

- INCS-712: Computer Forensics Cyber Forensics, Crime Scene AnalysisDocument50 pagesINCS-712: Computer Forensics Cyber Forensics, Crime Scene AnalysisdeepakNo ratings yet

- Investigative Auditing and Forensic Accounting - PresentationDocument69 pagesInvestigative Auditing and Forensic Accounting - PresentationIrfan JayaNo ratings yet

- Powerpoint On Fact FindingDocument14 pagesPowerpoint On Fact FindingMichelle MatiasNo ratings yet

- Introduction, Conceptual Framework of The Study & Research DesignDocument16 pagesIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺No ratings yet

- Fraud Control Jul08Document46 pagesFraud Control Jul08hmedlamineNo ratings yet

- Forensic BrochureDocument5 pagesForensic Brochuremsamala09No ratings yet

- Uncovering Fraud at DLF Towers Owners Welfare AssociationDocument24 pagesUncovering Fraud at DLF Towers Owners Welfare AssociationChartered AccountantNo ratings yet

- Overview & Approach Forensic Audit RLKDocument33 pagesOverview & Approach Forensic Audit RLKDINGDINGWALANo ratings yet

- CH 01Document16 pagesCH 01rajeshaisdu009No ratings yet

- A New Era in Phishing Research PaperDocument15 pagesA New Era in Phishing Research PaperRuchika RaiNo ratings yet

- Collin Street Bakery - Group 3Document10 pagesCollin Street Bakery - Group 3akun keduaNo ratings yet

- 5 6318691500020466224-1Document5 pages5 6318691500020466224-1shuchim guptaNo ratings yet

- Report WritingDocument26 pagesReport WritingHamza BBANo ratings yet

- PWC Forensic Report On MCXDocument15 pagesPWC Forensic Report On MCXdiffsoftNo ratings yet

- Investigative Interviewing: A Practical Guide For Using The Peace ModelDocument18 pagesInvestigative Interviewing: A Practical Guide For Using The Peace ModelLeah Moyao-DonatoNo ratings yet

- Fi 10032020Document46 pagesFi 10032020CA. (Dr.) Rajkumar Satyanarayan AdukiaNo ratings yet

- Banking fraud study on causes and prevention measuresDocument60 pagesBanking fraud study on causes and prevention measuresAjay RajbharNo ratings yet

- ACC 420 The Fraud Triangle TheoryDocument2 pagesACC 420 The Fraud Triangle TheoryIfemide50% (2)

- Forensic Accounting Handout on Occupational FraudsDocument10 pagesForensic Accounting Handout on Occupational Fraudsfammakhan1No ratings yet

- Assignment Psy382 s08Document4 pagesAssignment Psy382 s08helmyeda0% (1)

- SWI Zondo Submission Gupta Enterprise TransnetDocument110 pagesSWI Zondo Submission Gupta Enterprise TransnetDylanNo ratings yet

- Ibm ReportDocument7 pagesIbm ReportleejolieNo ratings yet

- CAATS and Fraud - June 14Document85 pagesCAATS and Fraud - June 14Andrew WamaeNo ratings yet

- Developing A Fraud Risk Assessment - CPE - Printable PDF - Part1Document47 pagesDeveloping A Fraud Risk Assessment - CPE - Printable PDF - Part1nur_haryantoNo ratings yet

- Report On A Forensic Audit and Review of Guyana Forestry CommissionDocument70 pagesReport On A Forensic Audit and Review of Guyana Forestry CommissionGenevieve BelmakerNo ratings yet

- Fraud Theories PropertiesDocument17 pagesFraud Theories PropertiesJohn Adel100% (1)

- Investigating Misconduct - Prof MaimunahDocument28 pagesInvestigating Misconduct - Prof MaimunahAmrezaa IskandarNo ratings yet

- Forensic Accounting's Role in Fraud Detection and PreventionDocument42 pagesForensic Accounting's Role in Fraud Detection and PreventionangelNo ratings yet

- JK Manufacturing Is Considering A New Product and Is UnsureDocument1 pageJK Manufacturing Is Considering A New Product and Is UnsureAmit PandeyNo ratings yet

- The Technical ReportsDocument40 pagesThe Technical ReportsprettynaugthyNo ratings yet

- FA (Fraud Introduction)Document4 pagesFA (Fraud Introduction)Eizel NasolNo ratings yet

- Fraud Prevention, Detection & ControlDocument16 pagesFraud Prevention, Detection & ControlRavindra A. KamathNo ratings yet

- Management FraudsDocument21 pagesManagement Fraudsksmann88100% (7)

- Unpacking FraudDocument9 pagesUnpacking FraudKenneth MadikeksNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 SolutionDocument7 pagesFar660 - Special Feb 2020 SolutionHanis ZahiraNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1Document6 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1auni fildzahNo ratings yet

- Chap 1 - Tutorial SDocument11 pagesChap 1 - Tutorial SHanis ZahiraNo ratings yet

- FAR660 Advanced Financial Accounting Reporting PhasesDocument3 pagesFAR660 Advanced Financial Accounting Reporting PhasesHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 QuestionDocument5 pagesFar660 - Special Feb 2020 QuestionHanis ZahiraNo ratings yet

- Chapter 1 BelkaouiDocument35 pagesChapter 1 BelkaouiHanis ZahiraNo ratings yet

- CHAPTER 9 Internal Audit ReportDocument32 pagesCHAPTER 9 Internal Audit ReportHanis ZahiraNo ratings yet

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

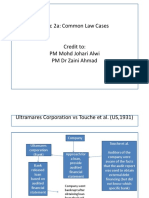

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

- AUD679 Line of Defense Hierarchy of IADocument9 pagesAUD679 Line of Defense Hierarchy of IAHanis ZahiraNo ratings yet

- CHAPTER 7 - Internal Auditing ProcessDocument37 pagesCHAPTER 7 - Internal Auditing ProcessHana HaziqahNo ratings yet

- TOPIC 6 - Implication of IT On IADocument38 pagesTOPIC 6 - Implication of IT On IAHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- CHAPTER 4 International Professional Practice Framework IPPFDocument14 pagesCHAPTER 4 International Professional Practice Framework IPPFHanis ZahiraNo ratings yet

- CORPORATE GOVERNANCE MECHANISMSDocument19 pagesCORPORATE GOVERNANCE MECHANISMSHanis ZahiraNo ratings yet

- Understanding the Evolution and Roles of Internal AuditingDocument22 pagesUnderstanding the Evolution and Roles of Internal AuditingHanis ZahiraNo ratings yet

- LCSO Booking Report: May 11, 2021Document3 pagesLCSO Booking Report: May 11, 2021WCTV Digital TeamNo ratings yet

- Red-Headed LeagueDocument25 pagesRed-Headed LeagueНаташа ПритолюкNo ratings yet

- RPC Felonies Defined and ClassifiedDocument7 pagesRPC Felonies Defined and ClassifiedFRANCHETTE FERNANDEZ SIMENENo ratings yet

- Blood and RosesDocument167 pagesBlood and RosesBemnet TayeNo ratings yet

- Alvin Comerciante Y Gonzales vs. People of The PhilippinesDocument2 pagesAlvin Comerciante Y Gonzales vs. People of The PhilippinesKaren Joy Masapol100% (1)

- Some Observations Re The JFK AssassinationDocument26 pagesSome Observations Re The JFK AssassinationWm. Thomas Sherman100% (1)

- Natividad Vs CA, 1 SCRA 280-1Document2 pagesNatividad Vs CA, 1 SCRA 280-1Divina Gracia Hinlo0% (1)

- Brief History of Self DefenseDocument2 pagesBrief History of Self DefenseReajenNo ratings yet

- Hull University Teaching Hospitals NHS Trust Clinical AttachmentDocument2 pagesHull University Teaching Hospitals NHS Trust Clinical AttachmentAyesha EhsanNo ratings yet

- Motion For ConsolidationDocument3 pagesMotion For ConsolidationflorNo ratings yet

- Apple Watch RobberyDocument22 pagesApple Watch RobberyGMG EditorialNo ratings yet

- CR WritDocument36 pagesCR WritdeepakNo ratings yet

- 6 Biggest Historical MysteriesDocument8 pages6 Biggest Historical Mysteriescarina enacheNo ratings yet

- Kent Stermon Memo Florida AttorneyDocument13 pagesKent Stermon Memo Florida AttorneyRaheem KassamNo ratings yet

- Cdi 3 Module - Rape InvestigationDocument53 pagesCdi 3 Module - Rape InvestigationKuya KhyNo ratings yet

- People Vs Rodriguez (135 SCRA 485) DigestDocument1 pagePeople Vs Rodriguez (135 SCRA 485) DigestMhay Khaeyl Badajos AndohuYhan100% (2)

- Sabang vs. People Defense of Relative Justification ExaminedDocument2 pagesSabang vs. People Defense of Relative Justification ExaminedM. CoCoNo ratings yet

- Upsurge of Money Ritual Among Youths in Nigeria and National SecurityDocument7 pagesUpsurge of Money Ritual Among Youths in Nigeria and National SecurityEditor IJTSRD100% (1)

- Expert DetectivesDocument12 pagesExpert DetectivesMANAV DHAKATE , 7DNo ratings yet

- Ready - For B2 TBDocument31 pagesReady - For B2 TBkarel petrNo ratings yet

- Worksheet 1 (Murder) : Rance V Mid-Downs Health Authority (1991) 1 All E.R. 801, 817Document17 pagesWorksheet 1 (Murder) : Rance V Mid-Downs Health Authority (1991) 1 All E.R. 801, 817Tevin PinnockNo ratings yet

- Cybercrime Law Philippines ThesisDocument5 pagesCybercrime Law Philippines ThesisKayla Smith100% (2)

- DOJ Inaction Allowed International Child Sex Trafficking Ring to FlourishDocument5 pagesDOJ Inaction Allowed International Child Sex Trafficking Ring to FlourishYLND100% (1)

- Martial Law False Claims FactsDocument2 pagesMartial Law False Claims FactsKing Aldus ConstantinoNo ratings yet

- Crime Module 6-22-2020Document60 pagesCrime Module 6-22-2020Shela Lapeña EscalonaNo ratings yet

- Philippine Police Restructuring PlanDocument21 pagesPhilippine Police Restructuring PlanAntique Ppo100% (1)

- Shriniwas Pandit Dharamadhikari and Ors Vs State Os800219COM770240Document2 pagesShriniwas Pandit Dharamadhikari and Ors Vs State Os800219COM770240Shyam APA JurisNo ratings yet

- People vs. Caruncho, JR., 127 SCRA 16, January 23, 1984Document55 pagesPeople vs. Caruncho, JR., 127 SCRA 16, January 23, 1984marvin ninoNo ratings yet

- Chapter 1: Understanding Self Defense Lessons 1 & 2: 1. A. B. C. D. E. F. G. 2. A. B. CDocument3 pagesChapter 1: Understanding Self Defense Lessons 1 & 2: 1. A. B. C. D. E. F. G. 2. A. B. CCherrie Pearl PokingNo ratings yet

- International Common Law Court of Justice - Crimes Against HumanityDocument18 pagesInternational Common Law Court of Justice - Crimes Against Humanitylio MwaniaNo ratings yet