You might also like

- Suggested Solution Far 660 Final Exam JUNE 2019Document6 pagesSuggested Solution Far 660 Final Exam JUNE 2019Nur ShahiraNo ratings yet

- Related PartiesDocument24 pagesRelated PartiesEsther PumihicNo ratings yet

- TAX 667 Topic 8 Tax Planning For CompanyDocument63 pagesTAX 667 Topic 8 Tax Planning For Companyzarif nezukoNo ratings yet

- InfosysDocument44 pagesInfosysSubhendu GhoshNo ratings yet

- Full ThesisDocument68 pagesFull ThesisVenkat SNo ratings yet

- Jyoti Kalra: Professional SynopsisDocument5 pagesJyoti Kalra: Professional SynopsisJyoti Sanjay KalraNo ratings yet

- MFRS 2, MFRS 119 Nestle V Ho HupDocument5 pagesMFRS 2, MFRS 119 Nestle V Ho HupNur ShahiraNo ratings yet

- IM For Financial Markets 1st Sem SY2020 21 Modules 1 To 8 Rev1Document62 pagesIM For Financial Markets 1st Sem SY2020 21 Modules 1 To 8 Rev1Sky LawrenceNo ratings yet

- Om Answer 1Document6 pagesOm Answer 1darshininambiarNo ratings yet

- Statistics Report..Document34 pagesStatistics Report..Tanvir Ahmed TariqueNo ratings yet

- DeloitteZA KingIV Bolder Than Ever CGG Nov2016Document20 pagesDeloitteZA KingIV Bolder Than Ever CGG Nov2016Philile NkwanyanaNo ratings yet

- GROUP 1 TAX INCENTIVES (HOTEL & TOURISM) EditedDocument20 pagesGROUP 1 TAX INCENTIVES (HOTEL & TOURISM) Editedmeera yusufNo ratings yet

- Thesesaastu 2019 261Document95 pagesThesesaastu 2019 261abraha gebruNo ratings yet

- Tata Motors Group Corporate Presentation 2022Document40 pagesTata Motors Group Corporate Presentation 2022Deepak PraiseNo ratings yet

- MBA LECTURE-lecture 1Document160 pagesMBA LECTURE-lecture 1takawira chirimeNo ratings yet

- EN 300 220 Test Report For 433MHzDocument45 pagesEN 300 220 Test Report For 433MHzEricNo ratings yet

- 487 Assignment 1 Rev.1Document32 pages487 Assignment 1 Rev.1Phan Thao Nguyen (FGW CT)No ratings yet

- Monthly Portfolio Oct 22Document583 pagesMonthly Portfolio Oct 22ribhu singhNo ratings yet

- Worksheet For Financial Acc. IDocument5 pagesWorksheet For Financial Acc. IFantay100% (1)

- Ch11 Roth3eDocument82 pagesCh11 Roth3etaghavi1347No ratings yet

- SM CompilerDocument249 pagesSM CompilerHimanshuNo ratings yet

- Msme FinanceDocument55 pagesMsme FinanceGauri MittalNo ratings yet

- The Ge/Mckinsey Matrix Offers A Strategic Approach To Show The Firm'S Performance To Help Prioritize Its' Investments Among Its Business UnitsDocument3 pagesThe Ge/Mckinsey Matrix Offers A Strategic Approach To Show The Firm'S Performance To Help Prioritize Its' Investments Among Its Business Unitsamanbansalgehu_33317No ratings yet

- OLC Chap 6Document11 pagesOLC Chap 6Isha SinghNo ratings yet

- 2 PDFDocument21 pages2 PDFHardikNo ratings yet

- Discuss The Concept of Entrepreneurship As Leadership, Risk Taking, Decision-Making and Business PlanningDocument3 pagesDiscuss The Concept of Entrepreneurship As Leadership, Risk Taking, Decision-Making and Business PlanningEuni ANo ratings yet

- Question 686785 1Document11 pagesQuestion 686785 1rishu53840% (1)

- CFA PM, AA, Econ, FI, Trading, Perf EvalDocument42 pagesCFA PM, AA, Econ, FI, Trading, Perf EvalKnightspageNo ratings yet

- SRS HospitalDocument8 pagesSRS HospitalAxidNo ratings yet

- Subject: Strategic Management: ON Analysis of Ncell and NTC Telecommunication CompaniesDocument13 pagesSubject: Strategic Management: ON Analysis of Ncell and NTC Telecommunication CompaniesKaemon BistaNo ratings yet

- Corporate Income TaxDocument24 pagesCorporate Income TaxRIRI RUMAIZHANo ratings yet

- Ifrs Study Material 2021Document17 pagesIfrs Study Material 2021Sagheer AhmedNo ratings yet

- GT Advanced Technologies Request To Void Apple AgreementsDocument15 pagesGT Advanced Technologies Request To Void Apple AgreementsMacRumorsNo ratings yet

- CMA CMA2 BookOnline SU4 OutlineDocument22 pagesCMA CMA2 BookOnline SU4 OutlineM AyazNo ratings yet

- SITXGLC001 - Written AssessmentDocument10 pagesSITXGLC001 - Written AssessmentRohan ShresthaNo ratings yet

- Mba (2019 Pattern) - 230212 - 181328Document171 pagesMba (2019 Pattern) - 230212 - 181328ManavNo ratings yet

- CFA - Ethics - R56-60 Version 1211Document182 pagesCFA - Ethics - R56-60 Version 1211Thanh NguyễnNo ratings yet

- Apollo TyresDocument330 pagesApollo TyresReTHINK INDIANo ratings yet

- Asbu Student Perception On The Role of Celebrity Endorsement in NigeriaDocument82 pagesAsbu Student Perception On The Role of Celebrity Endorsement in NigeriaDandy Kelvin100% (1)

- 7 Final Accounts of CompaniesDocument15 pages7 Final Accounts of CompaniesAakshi SharmaNo ratings yet

- Quiz KTTCDocument64 pagesQuiz KTTCChi NguyenNo ratings yet

- Final Sip Report at Tata Teleservices - (Consumer Behavior During Taking New Mobile Connections) By-Saurabh SinghDocument96 pagesFinal Sip Report at Tata Teleservices - (Consumer Behavior During Taking New Mobile Connections) By-Saurabh Singhsaurabh100% (4)

- Income Tax Must Do Questions by Vinit Mishra SirDocument109 pagesIncome Tax Must Do Questions by Vinit Mishra SirHenil DharodNo ratings yet

- 42 SayantanJana SIPDocument30 pages42 SayantanJana SIPShubham RakhundeNo ratings yet

- Capital Restructuring in Tata TeleservicesDocument14 pagesCapital Restructuring in Tata Teleservicesanant_parkarNo ratings yet

- Islamic Bonds: Learning ObjectivesDocument20 pagesIslamic Bonds: Learning ObjectivesAbdelnasir HaiderNo ratings yet

- Ipru Pension 10 Year X 2 LacDocument5 pagesIpru Pension 10 Year X 2 LacHK Option LearnNo ratings yet

- TUSHAR MANOHAR BHADANE ResumeDocument1 pageTUSHAR MANOHAR BHADANE ResumeKanchan ManhasNo ratings yet

- 01 Notes NPO WA For HasanDocument86 pages01 Notes NPO WA For HasanHassan MasoodNo ratings yet

- Step AnalysisDocument13 pagesStep AnalysisLow El LaNo ratings yet

- 2022 People's Proposed Budget Sustaining The Legacy of Real Change For The Future GenerationsDocument76 pages2022 People's Proposed Budget Sustaining The Legacy of Real Change For The Future GenerationsAnonymous dtceNuyIFINo ratings yet

- Partnership FormationDocument24 pagesPartnership FormationKC PaulinoNo ratings yet

- Unit 4 Accounting For LabourDocument18 pagesUnit 4 Accounting For LabourAayushi KothariNo ratings yet

- TOA DRILL 3 (Practical Accounting 2)Document14 pagesTOA DRILL 3 (Practical Accounting 2)ROMAR A. PIGANo ratings yet

- Proficiency in General Knowledge For P.G.C.E.T - Mba: A Lecture Given byDocument70 pagesProficiency in General Knowledge For P.G.C.E.T - Mba: A Lecture Given byPurushotham MPNo ratings yet

- HB 1379Document12 pagesHB 1379Jeremy TurleyNo ratings yet

- Evaluation of The Effect of Manpower Training and Development in Service OrganizationDocument101 pagesEvaluation of The Effect of Manpower Training and Development in Service OrganizationOlanrewaju AdeyanjuNo ratings yet

- Voltas LimitedDocument16 pagesVoltas LimitedvedaNo ratings yet

- Suggested Solution Far 660 Final Exam June 2017Document7 pagesSuggested Solution Far 660 Final Exam June 2017Nur ShahiraNo ratings yet

- Suggested Solution Far 660 - Special Feb 2018Document8 pagesSuggested Solution Far 660 - Special Feb 2018Nur ShahiraNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 QuestionDocument5 pagesFar660 - Special Feb 2020 QuestionHanis ZahiraNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1Document6 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1auni fildzahNo ratings yet

- Chap 1 - Tutorial QDocument3 pagesChap 1 - Tutorial QHanis ZahiraNo ratings yet

- Chap 1 - Tutorial SDocument11 pagesChap 1 - Tutorial SHanis ZahiraNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- Chapter 1 BelkaouiDocument35 pagesChapter 1 BelkaouiHanis ZahiraNo ratings yet

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

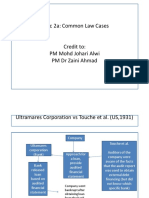

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- AUD679 Line of Defense Hierarchy of IADocument9 pagesAUD679 Line of Defense Hierarchy of IAHanis ZahiraNo ratings yet

- CHAPTER 9 Internal Audit ReportDocument32 pagesCHAPTER 9 Internal Audit ReportHanis ZahiraNo ratings yet

- CHAPTER 8 Investigation of FraudDocument45 pagesCHAPTER 8 Investigation of FraudHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- TOPIC 6 - Implication of IT On IADocument38 pagesTOPIC 6 - Implication of IT On IAHanis ZahiraNo ratings yet

- CHAPTER 4 International Professional Practice Framework IPPFDocument14 pagesCHAPTER 4 International Professional Practice Framework IPPFHanis ZahiraNo ratings yet

- CHAPTER 7 - Internal Auditing ProcessDocument37 pagesCHAPTER 7 - Internal Auditing ProcessHana HaziqahNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- 02 Chapter 2 - Corporate Governance MechanismDocument19 pages02 Chapter 2 - Corporate Governance MechanismHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 1 Overview of Internal Auditing FazDocument22 pagesCHAPTER 1 Overview of Internal Auditing FazHanis ZahiraNo ratings yet

- Bassoon (FAGOT) : See AlsoDocument36 pagesBassoon (FAGOT) : See Alsocarlos tarancón0% (1)

- DeadlocksDocument41 pagesDeadlocksSanjal DesaiNo ratings yet

- 3E Hand Over NotesDocument3 pages3E Hand Over NotesAshutosh MaiidNo ratings yet

- Debate Brochure PDFDocument2 pagesDebate Brochure PDFShehzada FarhaanNo ratings yet

- Midterm ReviewerDocument20 pagesMidterm ReviewerJonnafe IgnacioNo ratings yet

- Immobilization of Rhodococcus Rhodochrous BX2 (An AcetonitriledegradingDocument7 pagesImmobilization of Rhodococcus Rhodochrous BX2 (An AcetonitriledegradingSahar IrankhahNo ratings yet

- The Perception of Luxury Cars MA Thesis 25 03Document60 pagesThe Perception of Luxury Cars MA Thesis 25 03Quaxi1954No ratings yet

- Literature Review - Part Time Job Among StudentDocument3 pagesLiterature Review - Part Time Job Among StudentMarria65% (20)

- Kursus Jabatan Kejuruteraan Mekanikal Sesi Jun 2014Document12 pagesKursus Jabatan Kejuruteraan Mekanikal Sesi Jun 2014ihsanyusoffNo ratings yet

- Pot-Roasted Beef BrisketDocument4 pagesPot-Roasted Beef Brisketmarcelo nubileNo ratings yet

- Jy992d66901 CDocument6 pagesJy992d66901 CMaitry ShahNo ratings yet

- Democracy or Aristocracy?: Yasir MasoodDocument4 pagesDemocracy or Aristocracy?: Yasir MasoodAjmal KhanNo ratings yet

- Circuit Construction: Assignment 3Document45 pagesCircuit Construction: Assignment 3ali morisyNo ratings yet

- The Other Twelve Part 1Document5 pagesThe Other Twelve Part 1vv380100% (2)

- Rosewood Case AnalysisDocument5 pagesRosewood Case AnalysisJayant KushwahaNo ratings yet

- Off Grid Solar Hybrid Inverter Operate Without Battery: HY VMII SeriesDocument1 pageOff Grid Solar Hybrid Inverter Operate Without Battery: HY VMII SeriesFadi Ramadan100% (1)

- Operation and Maintenance Manual Compressor Models: P105WJD, P130DWJD, P160DWJD, P175DWJDDocument70 pagesOperation and Maintenance Manual Compressor Models: P105WJD, P130DWJD, P160DWJD, P175DWJDManuel ParreñoNo ratings yet

- Iso Iec 25030 2007 eDocument44 pagesIso Iec 25030 2007 eAngélica100% (1)

- The Ethics of Peacebuilding PDFDocument201 pagesThe Ethics of Peacebuilding PDFTomas Kvedaras100% (2)

- Chapter 4 Signal Flow GraphDocument34 pagesChapter 4 Signal Flow GraphAbhishek PattanaikNo ratings yet

- Sousa2019 PDFDocument38 pagesSousa2019 PDFWilly PurbaNo ratings yet

- Shoshana Bulka PragmaticaDocument17 pagesShoshana Bulka PragmaticaJessica JonesNo ratings yet

- Half Yearly Examination, 2017-18: MathematicsDocument7 pagesHalf Yearly Examination, 2017-18: MathematicsSusanket DuttaNo ratings yet

- Icc Esr-2302 Kb3 ConcreteDocument11 pagesIcc Esr-2302 Kb3 ConcretexpertsteelNo ratings yet

- An Introduction To Routine and Special StainingDocument13 pagesAn Introduction To Routine and Special StainingBadiu ElenaNo ratings yet

- Pizza Restaurant PowerPoint TemplatesDocument49 pagesPizza Restaurant PowerPoint TemplatesAindrila BeraNo ratings yet

- 1 AlarmvalveDocument9 pages1 AlarmvalveAnandNo ratings yet

- LP Pe 3Q - ShaynevillafuerteDocument3 pagesLP Pe 3Q - ShaynevillafuerteMa. Shayne Rose VillafuerteNo ratings yet

- HPSC HCS Exam 2021: Important DatesDocument6 pagesHPSC HCS Exam 2021: Important DatesTejaswi SaxenaNo ratings yet

- Chapter 9Document28 pagesChapter 9Aniket BatraNo ratings yet