You might also like

- The International Professional Practices Framework (Ippf)Document5 pagesThe International Professional Practices Framework (Ippf)Milovan Filimonović50% (2)

- Ippf 2017Document6 pagesIppf 2017Brylle TamañoNo ratings yet

- 02 - BaFa BaFa Simulation Instructions and DebriefingDocument9 pages02 - BaFa BaFa Simulation Instructions and DebriefingJ Lar100% (1)

- Evaluating Ethics Related Programmes and ActivitiesDocument36 pagesEvaluating Ethics Related Programmes and Activitiesgalal2720006810No ratings yet

- Module 5 - IA Process Engagement Planning and PerformingDocument67 pagesModule 5 - IA Process Engagement Planning and PerformingMichaelNo ratings yet

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- FAR660 Advanced Financial Accounting Reporting PhasesDocument3 pagesFAR660 Advanced Financial Accounting Reporting PhasesHanis ZahiraNo ratings yet

- MoU - LawPathDocument3 pagesMoU - LawPathBrandon_McEvoy562No ratings yet

- IPPF Guidance Can Be Divided IntoDocument42 pagesIPPF Guidance Can Be Divided IntoabdiweliNo ratings yet

- Week 6 Internal Audit Class on IPPF StandardsDocument53 pagesWeek 6 Internal Audit Class on IPPF StandardsHeidee SabidoNo ratings yet

- Internal Audit Charter Mandatory ElementsDocument136 pagesInternal Audit Charter Mandatory Elementsjudel ArielNo ratings yet

- CIA Part 1 Mission and Core PrinciplesDocument35 pagesCIA Part 1 Mission and Core PrinciplesAhmed AzaziNo ratings yet

- I. Governance and Internal Audit Strengthening Corporate Governance With Internal AuditDocument3 pagesI. Governance and Internal Audit Strengthening Corporate Governance With Internal AuditLEIGHANNE ZYRIL SANTOSNo ratings yet

- Lesson 5 - ISPPIA - Part 1 - Canvas 2020Document65 pagesLesson 5 - ISPPIA - Part 1 - Canvas 2020Janysse Calderon100% (1)

- The International Professional Practices Framework: Jean-Pierre Garitte, CIA, CCSA, CISA, CFEDocument47 pagesThe International Professional Practices Framework: Jean-Pierre Garitte, CIA, CCSA, CISA, CFEKaren Somcio100% (1)

- Red Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaDocument78 pagesRed Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaАндрей МиксоновNo ratings yet

- Internal Audit Process: IPPF Standards, Audit TypesDocument34 pagesInternal Audit Process: IPPF Standards, Audit TypesObert MarongedzaNo ratings yet

- Code of EthicsDocument35 pagesCode of EthicsarthanindiraNo ratings yet

- IPPFInternational Professional Practices FrameworkDocument18 pagesIPPFInternational Professional Practices FrameworkSumirah Maktar100% (1)

- Topic 4 - Internal AuditingDocument19 pagesTopic 4 - Internal AuditingSandile Henry DlaminiNo ratings yet

- Foundations of Internal Audit (IPPFDocument4 pagesFoundations of Internal Audit (IPPFS4M1Y4No ratings yet

- IIA, CobiT, and Professional Internal Audit Standards ExplainedDocument29 pagesIIA, CobiT, and Professional Internal Audit Standards Explainedlely2014100% (2)

- IG Code of Ethics 1 IntegrityDocument6 pagesIG Code of Ethics 1 IntegrityJohnson JongNo ratings yet

- Kerangka Baru Dan LamaDocument6 pagesKerangka Baru Dan LamaPutri WigrhaNo ratings yet

- EthicsDocument41 pagesEthicsMERINANo ratings yet

- Muh - Ferial Ferniawan/A031191156 The International Practices FrameworkDocument5 pagesMuh - Ferial Ferniawan/A031191156 The International Practices FrameworkFerial FerniawanNo ratings yet

- IG Code of Ethics 2 ObjectivityDocument7 pagesIG Code of Ethics 2 ObjectivityJohnson JongNo ratings yet

- Code of Ethics of Internal AuditingDocument3 pagesCode of Ethics of Internal AuditingHazel-Lynn MasangcayNo ratings yet

- IG Code of Ethics 2 Objectivity PDFDocument6 pagesIG Code of Ethics 2 Objectivity PDFnurseviantoNo ratings yet

- 2002 Organisational Independence CISADocument7 pages2002 Organisational Independence CISAdeeptimanneyNo ratings yet

- Internal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiaDocument86 pagesInternal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiacuixiNo ratings yet

- Nature of Modern Internal AuditingDocument15 pagesNature of Modern Internal Auditinganon_323651754No ratings yet

- IIA Code of EthicsDocument3 pagesIIA Code of EthicsachistepNo ratings yet

- Internal Auditing For StudentsDocument14 pagesInternal Auditing For StudentsAzrisah PanandiganNo ratings yet

- Code of Ethics GuideDocument3 pagesCode of Ethics GuidenphiriNo ratings yet

- C C !" # $ C # " ! % ! ! C & # !#!'! & # (! C C C ! %) " ! " +,-! ". ! + - % - ! +/ - 0Document5 pagesC C !" # $ C # " ! % ! ! C & # !#!'! & # (! C C C ! %) " ! " +,-! ". ! + - % - ! +/ - 0Pitima PatNo ratings yet

- CIA P1 SI Foundations of Internal AuditingDocument102 pagesCIA P1 SI Foundations of Internal AuditingJayAr Dela RosaNo ratings yet

- Chapter 2 The Auditing ProfessionDocument56 pagesChapter 2 The Auditing ProfessionNigussie Berhanu100% (1)

- Chapter 5 Ethical Standards Social ResponsibilityDocument4 pagesChapter 5 Ethical Standards Social ResponsibilityVETERAN ARMY 2013No ratings yet

- Debi Roth - 2017 Standards and Guidance Update 1.17.2017Document42 pagesDebi Roth - 2017 Standards and Guidance Update 1.17.2017zeerakzahidNo ratings yet

- IIAS Lunch Talk Jan On New Standards 200117Document20 pagesIIAS Lunch Talk Jan On New Standards 200117Bedoui WassimNo ratings yet

- 2 - Internal Auditing StandardsDocument3 pages2 - Internal Auditing StandardsVarduhiNo ratings yet

- Topic 2Document5 pagesTopic 2Kesh NathenNo ratings yet

- TOPIC 3 - Ethics & Internal AuditorDocument29 pagesTOPIC 3 - Ethics & Internal AuditoradifhrzlNo ratings yet

- Auditing QMS IQA PresentationDocument128 pagesAuditing QMS IQA PresentationJeaneth Dela Pena Carnicer100% (1)

- Module 4 - Nature of WorkDocument43 pagesModule 4 - Nature of WorkMichaelNo ratings yet

- Presentation Internal Audit StandardsDocument98 pagesPresentation Internal Audit StandardsAbera100% (1)

- Sesi2 International Standards For The Professional Practice of InternalDocument26 pagesSesi2 International Standards For The Professional Practice of InternalAlfryda Nabila Permatasari AegyoNo ratings yet

- International Standards For The Professional Practice of Internal AuditingDocument30 pagesInternational Standards For The Professional Practice of Internal AuditingAbdullah HameedNo ratings yet

- Guidance for Internal Auditors (20Document4 pagesGuidance for Internal Auditors (20El BieNo ratings yet

- Institute of Internal AuditorsDocument5 pagesInstitute of Internal AuditorsDiego LeónNo ratings yet

- 2001 Audit Charter-CISADocument7 pages2001 Audit Charter-CISAdeeptimanneyNo ratings yet

- IG 2000 Managing The Internal Audit ActivityDocument5 pagesIG 2000 Managing The Internal Audit ActivitygdegirolamoNo ratings yet

- QAIP ExternalDocument4 pagesQAIP ExternalMaria Rona SilvestreNo ratings yet

- Manual 2Document30 pagesManual 2Gideon HilardeNo ratings yet

- Unit 2: The Auditing ProfessionDocument15 pagesUnit 2: The Auditing ProfessionYonasNo ratings yet

- 2203 Performance and SupervisionDocument11 pages2203 Performance and SupervisiondeeptimanneyNo ratings yet

- Welcomes You To ISO 19600:2014 Awareness Training ProgrammeDocument119 pagesWelcomes You To ISO 19600:2014 Awareness Training ProgrammeNada HajriNo ratings yet

- Control Environment Self-AssessmentDocument23 pagesControl Environment Self-AssessmentTolits MillabasNo ratings yet

- Mod1 ReviewerDocument5 pagesMod1 Reviewersara sibumaNo ratings yet

- Iso 9000 Family of Standards: With Extracts from Iso 9001 Audit Trail (First Edition)From EverandIso 9000 Family of Standards: With Extracts from Iso 9001 Audit Trail (First Edition)No ratings yet

- Exploding the Myths Surrounding ISO9000: A practical implementation guideFrom EverandExploding the Myths Surrounding ISO9000: A practical implementation guideNo ratings yet

- Far660 - Special Feb 2020 SolutionDocument7 pagesFar660 - Special Feb 2020 SolutionHanis ZahiraNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1Document6 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1auni fildzahNo ratings yet

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 QuestionDocument5 pagesFar660 - Special Feb 2020 QuestionHanis ZahiraNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- Chap 1 - Tutorial SDocument11 pagesChap 1 - Tutorial SHanis ZahiraNo ratings yet

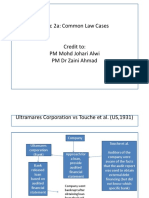

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

- Chapter 1 BelkaouiDocument35 pagesChapter 1 BelkaouiHanis ZahiraNo ratings yet

- CHAPTER 9 Internal Audit ReportDocument32 pagesCHAPTER 9 Internal Audit ReportHanis ZahiraNo ratings yet

- AUD679 Line of Defense Hierarchy of IADocument9 pagesAUD679 Line of Defense Hierarchy of IAHanis ZahiraNo ratings yet

- CHAPTER 8 Investigation of FraudDocument45 pagesCHAPTER 8 Investigation of FraudHanis ZahiraNo ratings yet

- CORPORATE GOVERNANCE MECHANISMSDocument19 pagesCORPORATE GOVERNANCE MECHANISMSHanis ZahiraNo ratings yet

- TOPIC 6 - Implication of IT On IADocument38 pagesTOPIC 6 - Implication of IT On IAHanis ZahiraNo ratings yet

- CHAPTER 7 - Internal Auditing ProcessDocument37 pagesCHAPTER 7 - Internal Auditing ProcessHana HaziqahNo ratings yet

- Understanding the Evolution and Roles of Internal AuditingDocument22 pagesUnderstanding the Evolution and Roles of Internal AuditingHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- FFA Membership, Ethics, Degrees, and Awards: ObjectivesDocument9 pagesFFA Membership, Ethics, Degrees, and Awards: ObjectivesSophia BrannemanNo ratings yet

- Constantino vs. Atty. SaludaresDocument2 pagesConstantino vs. Atty. Saludaressonya100% (3)

- Criminal Law 1 Assignment 10-15-2021Document4 pagesCriminal Law 1 Assignment 10-15-2021Santillan JeffreyNo ratings yet

- SAG - Hilot (Wellness Massage) NC II PDFDocument2 pagesSAG - Hilot (Wellness Massage) NC II PDFVicente SyNo ratings yet

- Taylor V JohnsonDocument2 pagesTaylor V JohnsonHelen HeNo ratings yet

- Ra 10022Document23 pagesRa 10022Kristin SotoNo ratings yet

- UK Home Office: Aud02Document6 pagesUK Home Office: Aud02UK_HomeOfficeNo ratings yet

- Team Formation: 3.1 Preparation For Forming A TeamDocument9 pagesTeam Formation: 3.1 Preparation For Forming A TeamTeddy BearNo ratings yet

- HR EnvironmentDocument39 pagesHR EnvironmentNihar KapdiNo ratings yet

- Mrs. Leema Rose MartinDocument2 pagesMrs. Leema Rose MartinSantiago MartinNo ratings yet

- Veterans Day ProclamationDocument1 pageVeterans Day ProclamationRamblingChiefNo ratings yet

- PTA (TGT) Contract 13012015 RamanDocument15 pagesPTA (TGT) Contract 13012015 Ramanसबका बापNo ratings yet

- Caso Fabiessi and Cam's DesignDocument1 pageCaso Fabiessi and Cam's DesignDiego PalominoNo ratings yet

- Short Essay 2Document6 pagesShort Essay 2Allan YuNo ratings yet

- 3 Ketu (South Node) Rahu (North Node) Life Learning in AstrologyDocument4 pages3 Ketu (South Node) Rahu (North Node) Life Learning in AstrologyRahulshah1984No ratings yet

- Bloom's TaxonomyDocument5 pagesBloom's TaxonomyjpernitoNo ratings yet

- Interview skills: Tips for acing your next job interviewDocument12 pagesInterview skills: Tips for acing your next job interviewBhavik YoganandiNo ratings yet

- Sermon by Rodney Tan Melaka Gospel Chapel Sunday 21/7/2019Document29 pagesSermon by Rodney Tan Melaka Gospel Chapel Sunday 21/7/2019Rodney TanNo ratings yet

- Relations of Political Science With Other Social SciencesDocument10 pagesRelations of Political Science With Other Social Sciencesehtisham50% (2)

- Datu Michael Abas Kida Vs SenateDocument23 pagesDatu Michael Abas Kida Vs SenatesamanthaNo ratings yet

- KABBUR PUBLICATIONS YouTube Channel Study Materials Romeo and Juliet SummaryDocument61 pagesKABBUR PUBLICATIONS YouTube Channel Study Materials Romeo and Juliet SummaryRamya. RNo ratings yet

- (Information Plus Reference Series) Nancy Dziedzic - World Poverty-Gale Cengage (2006)Document159 pages(Information Plus Reference Series) Nancy Dziedzic - World Poverty-Gale Cengage (2006)Riamon RojoNo ratings yet

- Lost Spring-Stories of Stolen ChildhoodDocument6 pagesLost Spring-Stories of Stolen ChildhoodDebotroyeeNo ratings yet

- Bandura 2001 Social Cognitive Theory An Agentic PerspectiveDocument27 pagesBandura 2001 Social Cognitive Theory An Agentic PerspectiveOscar Iván Negrete RodríguezNo ratings yet

- Natural Law Theory ApproachDocument35 pagesNatural Law Theory ApproachseventhwitchNo ratings yet

- Consti Chapter 1Document52 pagesConsti Chapter 1Leslie TanNo ratings yet

- Correlational Research Example FINALDocument124 pagesCorrelational Research Example FINALNerinel CoronadoNo ratings yet

- Moral MaturityDocument12 pagesMoral MaturityJerome FaylugaNo ratings yet