You might also like

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Mutual Funds in India: Structure, Performance and UndercurrentsFrom EverandMutual Funds in India: Structure, Performance and UndercurrentsNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1Document6 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JULY2020/FAR660/SET1auni fildzahNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

- Far570 SoalanDocument7 pagesFar570 SoalanNURUL NAZAHANNIE MOHAMAD NAJIBNo ratings yet

- FAR570 Jul 2020 Set 1 (Sesi 1) - QDocument4 pagesFAR570 Jul 2020 Set 1 (Sesi 1) - QNURUL NAZAHANNIE MOHAMAD NAJIBNo ratings yet

- Acc202 (Q) - Online Exam (Both Campus) (Mock Exam)Document8 pagesAcc202 (Q) - Online Exam (Both Campus) (Mock Exam)Rishiaendra CoolNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/FEB 2022/FAR570Document7 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/FEB 2022/FAR570NURUL NAZAHANNIE MOHAMAD NAJIBNo ratings yet

- 12.feb 2022Document8 pages12.feb 2022paan tiktokNo ratings yet

- Advanced Financial Accounting and Reporting ExamDocument8 pagesAdvanced Financial Accounting and Reporting ExamNg GraceNo ratings yet

- FAR570 - Q - August 2021Document7 pagesFAR570 - Q - August 2021NURUL NAZAHANNIE MOHAMAD NAJIBNo ratings yet

- Test 1 Maf653 April 2018 Latest-SolutionDocument9 pagesTest 1 Maf653 April 2018 Latest-SolutionFakhrul Haziq Md FarisNo ratings yet

- Universiti Teknologi Mara Common Test 1: Confidential 1 TEST1/NOV2017/FAR210Document4 pagesUniversiti Teknologi Mara Common Test 1: Confidential 1 TEST1/NOV2017/FAR210shahrinNo ratings yet

- Far160 - Dec 2019 - QDocument8 pagesFar160 - Dec 2019 - QNur ain Natasha ShaharudinNo ratings yet

- Al Financial Management May Jun 2017Document4 pagesAl Financial Management May Jun 2017Akash79No ratings yet

- 2019 - Dec 2019 - Fin645 - 541 - 651 - 630Document4 pages2019 - Dec 2019 - Fin645 - 541 - 651 - 630Allieya AlawiNo ratings yet

- AFAR1 Main Exam Q (Feb 2022)Document5 pagesAFAR1 Main Exam Q (Feb 2022)Alice LowNo ratings yet

- Test FAR 570 Feb 2021Document2 pagesTest FAR 570 Feb 2021Putri Naajihah 4GNo ratings yet

- MML 5202Document6 pagesMML 5202MAKUENI PIGSNo ratings yet

- Test 1 Maf653 Oct 2019 QnADocument8 pagesTest 1 Maf653 Oct 2019 QnAFakhrul Haziq Md FarisNo ratings yet

- Financial Accounting and Reporting I: Additional Practice QuestionsDocument34 pagesFinancial Accounting and Reporting I: Additional Practice Questionsalia khanNo ratings yet

- 71475exam57501 p6f 2Document37 pages71475exam57501 p6f 2Anagha ReddyNo ratings yet

- Paper 10 Financial ManagementDocument10 pagesPaper 10 Financial ManagementJoseph OsakoNo ratings yet

- FAR-2 Mock September 2021 FinalDocument8 pagesFAR-2 Mock September 2021 FinalMuhammad RahimNo ratings yet

- CT - Maf253 Q Aug2016Document6 pagesCT - Maf253 Q Aug2016Nur Anis AqilahNo ratings yet

- Universiti Teknologi Mara Common Test 1: Confidential 1 AC/OCT 2019/FAR160Document4 pagesUniversiti Teknologi Mara Common Test 1: Confidential 1 AC/OCT 2019/FAR160Nurul Syaza MusaNo ratings yet

- 2021 2-11-146 CL2-Financial Accounting Reporting-Feb2021 EnglishDocument13 pages2021 2-11-146 CL2-Financial Accounting Reporting-Feb2021 Englishnoway snirfyNo ratings yet

- ACCO1115 - May 2017 - EXAMDocument9 pagesACCO1115 - May 2017 - EXAMSarah RanduNo ratings yet

- New Format Exam Q Maf620 - Dec 2014Document6 pagesNew Format Exam Q Maf620 - Dec 2014kkNo ratings yet

- Advanced Taxation: Progress Test 2Document6 pagesAdvanced Taxation: Progress Test 2Putera IzwanNo ratings yet

- Universiti Teknologi Mara Common Test 1: Confidential AC/AUG 2016/MAF253Document6 pagesUniversiti Teknologi Mara Common Test 1: Confidential AC/AUG 2016/MAF253Bonna Della TianamNo ratings yet

- Financial Management-1Document6 pagesFinancial Management-1chelseaNo ratings yet

- Ac Maf603 Dec16Document6 pagesAc Maf603 Dec16MOHAMMAD NOOR AIMAN AHMADNo ratings yet

- Maf201 Test 2 Jan 2023 QDocument5 pagesMaf201 Test 2 Jan 2023 Qediza adhaNo ratings yet

- 4 Financial ManagementDocument5 pages4 Financial ManagementBizness Zenius Hant100% (1)

- Test November 2022 - Test 1Document3 pagesTest November 2022 - Test 1nabilaNo ratings yet

- MAF603-QUESTION TEST 2 - Nov 2019Document3 pagesMAF603-QUESTION TEST 2 - Nov 2019fareen faridNo ratings yet

- TWO (2) Questions From SECTION B in The Answer Booklet Provided. All Question CarryDocument4 pagesTWO (2) Questions From SECTION B in The Answer Booklet Provided. All Question CarrynatlyhNo ratings yet

- Far570 Q Test December 2022Document4 pagesFar570 Q Test December 2022fareen faridNo ratings yet

- Faculty Accountancy 2022 Session 1 - Degree Far510Document13 pagesFaculty Accountancy 2022 Session 1 - Degree Far510Wahida AmalinNo ratings yet

- QPB - Dec - 20 Mock 1 Q FinalDocument9 pagesQPB - Dec - 20 Mock 1 Q FinalBernice Chan Wai WunNo ratings yet

- Grand Test 2 BFD CFAP 4 Dec 22 with Solution ST Academy (Sir Saud Tariq)Document14 pagesGrand Test 2 BFD CFAP 4 Dec 22 with Solution ST Academy (Sir Saud Tariq)aimanraees10No ratings yet

- Project Finance Question PaperDocument3 pagesProject Finance Question PaperBhavna0% (1)

- Jun'19 QDocument7 pagesJun'19 QVivek SaraogiNo ratings yet

- CPA 8 - Financial Management - Paper 8Document13 pagesCPA 8 - Financial Management - Paper 8justinorchidsNo ratings yet

- sFikv8tLO3DuTOB3I8bY--4762Document2 pagessFikv8tLO3DuTOB3I8bY--4762dipusharma4200No ratings yet

- Mock Questions PDFDocument6 pagesMock Questions PDFMadhuram SharmaNo ratings yet

- Faculty Accountancy 2021 Session 1 - Degree Maf603 2Document12 pagesFaculty Accountancy 2021 Session 1 - Degree Maf603 2Hadi DahalanNo ratings yet

- Universiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Document6 pagesUniversiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Bonna Della TianamNo ratings yet

- 44956mtpbosicai Final QP p2Document7 pages44956mtpbosicai Final QP p2Shubham SurekaNo ratings yet

- Acc406 - Q - Set 1 - Sesi 1 July 2020Document12 pagesAcc406 - Q - Set 1 - Sesi 1 July 2020NABILA NADHIRAH ROSLANNo ratings yet

- 2019 AIC22A2 Test 1Document10 pages2019 AIC22A2 Test 1kdmd.wwNo ratings yet

- Question PaperDocument3 pagesQuestion PaperAmbrishNo ratings yet

- ISF 3106 Final Assessment Part B ApprovedDocument6 pagesISF 3106 Final Assessment Part B ApprovedRaihah Nabilah HashimNo ratings yet

- 2017 06 CPE-Full-Audit.-June-2017-QuestionsDocument10 pages2017 06 CPE-Full-Audit.-June-2017-Questionskellz accountingNo ratings yet

- SHACSBSC1103 PART II EDARANDocument4 pagesSHACSBSC1103 PART II EDARANCAROLINE ABRAHAMNo ratings yet

- NMIMS 2019 SeptemberDocument5 pagesNMIMS 2019 SeptemberRajni KumariNo ratings yet

- Far410 Test Oct 2018 - QuestionDocument4 pagesFar410 Test Oct 2018 - Question2022478048No ratings yet

- BBMF2093 24octDocument4 pagesBBMF2093 24octyvonneapj-wb22No ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Chap 1 - Tutorial SDocument11 pagesChap 1 - Tutorial SHanis ZahiraNo ratings yet

- FAR660 Advanced Financial Accounting Reporting PhasesDocument3 pagesFAR660 Advanced Financial Accounting Reporting PhasesHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 SolutionDocument7 pagesFar660 - Special Feb 2020 SolutionHanis ZahiraNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Chapter 1 BelkaouiDocument35 pagesChapter 1 BelkaouiHanis ZahiraNo ratings yet

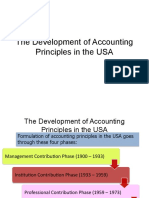

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

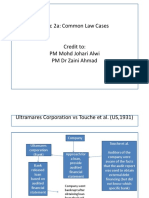

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- CHAPTER 7 - Internal Auditing ProcessDocument37 pagesCHAPTER 7 - Internal Auditing ProcessHana HaziqahNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- AUD679 Line of Defense Hierarchy of IADocument9 pagesAUD679 Line of Defense Hierarchy of IAHanis ZahiraNo ratings yet

- CHAPTER 9 Internal Audit ReportDocument32 pagesCHAPTER 9 Internal Audit ReportHanis ZahiraNo ratings yet

- CHAPTER 8 Investigation of FraudDocument45 pagesCHAPTER 8 Investigation of FraudHanis ZahiraNo ratings yet

- CHAPTER 4 International Professional Practice Framework IPPFDocument14 pagesCHAPTER 4 International Professional Practice Framework IPPFHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- TOPIC 6 - Implication of IT On IADocument38 pagesTOPIC 6 - Implication of IT On IAHanis ZahiraNo ratings yet

- CORPORATE GOVERNANCE MECHANISMSDocument19 pagesCORPORATE GOVERNANCE MECHANISMSHanis ZahiraNo ratings yet

- Understanding the Evolution and Roles of Internal AuditingDocument22 pagesUnderstanding the Evolution and Roles of Internal AuditingHanis ZahiraNo ratings yet

- Audit Programe For Statutory AuditDocument20 pagesAudit Programe For Statutory AuditTekumani Naveen KumarNo ratings yet

- Corporate Finance A Focused Approach 6th Edition Ehrhardt Test Bank 1Document34 pagesCorporate Finance A Focused Approach 6th Edition Ehrhardt Test Bank 1phyllis100% (30)

- Quiz 2 SwapDocument3 pagesQuiz 2 SwapJoel Christian MascariñaNo ratings yet

- Capital Markets Q&ADocument14 pagesCapital Markets Q&AMachinimaC0dNo ratings yet

- Extinguishment of ObligationsDocument10 pagesExtinguishment of ObligationsNimfa SabanalNo ratings yet

- A Credit Risk Model For AlbaniaDocument37 pagesA Credit Risk Model For AlbaniarunawayyyNo ratings yet

- Divisional Performance Measures and Transfer Pricing NotesDocument83 pagesDivisional Performance Measures and Transfer Pricing NotesShreya PatelNo ratings yet

- Dwnload Full Corporate Financial Management 5th Edition Glen Arnold Test Bank PDFDocument35 pagesDwnload Full Corporate Financial Management 5th Edition Glen Arnold Test Bank PDFhofstadgypsyus100% (12)

- Financial Statement AnalysisDocument3 pagesFinancial Statement Analysiselsana philipNo ratings yet

- MF Cost of Capital - Practice QuestionsDocument4 pagesMF Cost of Capital - Practice QuestionsSaad UsmanNo ratings yet

- Symbiosis Entrance Test (SET) : Model Paper 2Document12 pagesSymbiosis Entrance Test (SET) : Model Paper 2Arushi sharmaNo ratings yet

- Riba and Interest - Fazlur RahmanDocument43 pagesRiba and Interest - Fazlur RahmanSyed Mateen Ahmed91% (11)

- Daqo New Energy CorpDocument154 pagesDaqo New Energy Corpdkdude007No ratings yet

- Ibf Case StudyDocument17 pagesIbf Case StudyAyesha HamidNo ratings yet

- Loan Receivable: If Origination Fees Are Received From The Borrower, Record It As Unearned Interest IncomeDocument1 pageLoan Receivable: If Origination Fees Are Received From The Borrower, Record It As Unearned Interest IncomeAiya LumbanNo ratings yet

- 2019 Studylink Parents Form PDFDocument11 pages2019 Studylink Parents Form PDFInuri KuruppuNo ratings yet

- Common Loan Application Form - EnglishDocument7 pagesCommon Loan Application Form - EnglishSwiftNo ratings yet

- HTL With Money ManagerDocument67 pagesHTL With Money Managerkishor.kokateNo ratings yet

- The Customer Satisfaction CITI BANK PROJECT REPORT MBA MARKETINGDocument38 pagesThe Customer Satisfaction CITI BANK PROJECT REPORT MBA MARKETINGHimanshu KothariNo ratings yet

- The Bond Market (Chapter 12)Document29 pagesThe Bond Market (Chapter 12)AlessandraFazioNo ratings yet

- Impacts of budget deficit on macroeconomics in PakistanDocument13 pagesImpacts of budget deficit on macroeconomics in PakistanshaziadurraniNo ratings yet

- What Is Market Stabilization SchemeDocument5 pagesWhat Is Market Stabilization Schemezaru1121100% (1)

- Final Terms-C RCFP17L1 PDFDocument113 pagesFinal Terms-C RCFP17L1 PDFkauravaNo ratings yet

- Part 3 Case Digest Eladla de Lima vs. Laguna Tayabas CoDocument13 pagesPart 3 Case Digest Eladla de Lima vs. Laguna Tayabas CoJay-r Mercado ValenciaNo ratings yet

- Oblicon Reviewer Summary The Law On Obligations and Contracts PDFDocument63 pagesOblicon Reviewer Summary The Law On Obligations and Contracts PDFCarmelou Gavril Garcia ClimacoNo ratings yet

- Financial Management DFN2013: Ex I P Ex I IpDocument7 pagesFinancial Management DFN2013: Ex I P Ex I IpSyafix Samuel LouisNo ratings yet

- CB Lecture Merged 13decDocument444 pagesCB Lecture Merged 13decShalini GuptaNo ratings yet

- Financial Management Text Book SummaryDocument44 pagesFinancial Management Text Book SummaryGuLam Hilal Abdullah AL-Balushi89% (9)

- Int'l B & F CH 8Document3 pagesInt'l B & F CH 8Escherika WilliamsNo ratings yet

- UNIT 5 - Module I 107: Unit Five On FinanceDocument0 pagesUNIT 5 - Module I 107: Unit Five On FinanceLuiza BoleaNo ratings yet