You might also like

- Studymate Solutions To CBSE Board Examination 2018-2019: Series: BVM/1Document19 pagesStudymate Solutions To CBSE Board Examination 2018-2019: Series: BVM/1SukhmnNo ratings yet

- Project Marketing TrimDocument17 pagesProject Marketing Trimmahnoorumer33% (3)

- 20 Sample Papers - Economics (Solved) PDFDocument227 pages20 Sample Papers - Economics (Solved) PDFSimha SimhaNo ratings yet

- Class XII Accountancy Project AnalysisDocument41 pagesClass XII Accountancy Project AnalysisIshika BothraNo ratings yet

- 06 Sample PaperDocument40 pages06 Sample Papergaming loverNo ratings yet

- Cash Flow Statement Sample QuestionsDocument2 pagesCash Flow Statement Sample QuestionsAyush ChauhanNo ratings yet

- Importance of Human Capital FormationDocument18 pagesImportance of Human Capital FormationSayma ShaikhNo ratings yet

- Nature and Significance of ManagementDocument25 pagesNature and Significance of ManagementAditi Mahale100% (4)

- CBSE Class 12 Enterprise Growth Strategies NotesDocument13 pagesCBSE Class 12 Enterprise Growth Strategies NotesAbheejit VijayNo ratings yet

- Accountancy Project Work - XIIDocument41 pagesAccountancy Project Work - XIIkawsarNo ratings yet

- 652oswaal Case-Based Questions Accountancy 12th (Issued by CBSE in April-2021)Document7 pages652oswaal Case-Based Questions Accountancy 12th (Issued by CBSE in April-2021)Nitesh kuraheNo ratings yet

- Senior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3Document26 pagesSenior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3bhaiyarakeshNo ratings yet

- ITC Report and Accounts 2023 184Document1 pageITC Report and Accounts 2023 184Nishith RanjanNo ratings yet

- Rural Development - Handwritten Notes - (Kautilya)Document14 pagesRural Development - Handwritten Notes - (Kautilya)akshat jainNo ratings yet

- Math Project WorkDocument10 pagesMath Project WorkBasanta K SahuNo ratings yet

- Ratio Analysis of Bharat Heavy Electricals Limited: Final DraftDocument34 pagesRatio Analysis of Bharat Heavy Electricals Limited: Final DraftVidushi Verma50% (2)

- Accountancy Project Class 12th-1Document48 pagesAccountancy Project Class 12th-1Arpit BothraNo ratings yet

- Jashobanti Project On Cost SheetDocument15 pagesJashobanti Project On Cost SheetBiplab Swain100% (1)

- Comparing Organisational Structure and Financial Performance of Amul and Karnataka Milk FederationDocument14 pagesComparing Organisational Structure and Financial Performance of Amul and Karnataka Milk FederationAryan SinghNo ratings yet

- Applied: Mathematics Project WorkDocument18 pagesApplied: Mathematics Project WorkAnusha GhoshNo ratings yet

- Economics Class 12 Project On DemonetisationDocument8 pagesEconomics Class 12 Project On DemonetisationHargun Virk25% (4)

- CBSE Project GuidelinesDocument51 pagesCBSE Project GuidelinesShruti Yadav0% (1)

- Chapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IDocument68 pagesChapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IVISHNUKUMAR S VNo ratings yet

- CBSE Previous Year Question Papers Class 12 AccountancyDocument222 pagesCBSE Previous Year Question Papers Class 12 AccountancySujal BhavsarNo ratings yet

- Maths Project On Venn DiagramDocument14 pagesMaths Project On Venn DiagramPragyi Mittal100% (2)

- Solution Class 12 - Accountancy Accountancy Section A: Lsss 1 / 19Document19 pagesSolution Class 12 - Accountancy Accountancy Section A: Lsss 1 / 19Mohamed IbrahimNo ratings yet

- Senior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3Document26 pagesSenior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3bhaiyarakeshNo ratings yet

- Business Notes +2Document8 pagesBusiness Notes +2sunitygoyal099100% (1)

- Applied Mathematics Project on Matrix Multiplication, Inverse Matrix, Demand and Supply Functions, and Probability Calculation Using MS ExcelDocument12 pagesApplied Mathematics Project on Matrix Multiplication, Inverse Matrix, Demand and Supply Functions, and Probability Calculation Using MS ExcelNamandeep SinghNo ratings yet

- 07 Sample PaperDocument42 pages07 Sample Papergaming loverNo ratings yet

- Padhle 11th - 3 - Collection of Data - Statistics - EconomicsDocument12 pagesPadhle 11th - 3 - Collection of Data - Statistics - EconomicsAafia100% (1)

- Business Studies Project On Principles of ManagementDocument36 pagesBusiness Studies Project On Principles of Managementanshuman prajapatiNo ratings yet

- Project On Finalization of Partnership FirmDocument38 pagesProject On Finalization of Partnership Firmvenkynaidu67% (3)

- Accountancy Project Ratio AnalysisDocument21 pagesAccountancy Project Ratio AnalysisTanmay ChaitanyaNo ratings yet

- Worksheet For Issue of Share and DebentureDocument2 pagesWorksheet For Issue of Share and DebentureLaxmi Kant SahaniNo ratings yet

- +2 Commerce ProjectDocument17 pages+2 Commerce Projectvipoolgetia67% (3)

- Jashobanti Project On Final AccountsDocument17 pagesJashobanti Project On Final AccountsBiplab SwainNo ratings yet

- Balance Sheet of Jorex LimitedDocument1 pageBalance Sheet of Jorex LimitedShuchi Bhatia50% (2)

- Accounting Final AccountsDocument18 pagesAccounting Final AccountsAjay Sahoo100% (3)

- Project On Ratio and Cash Flow Analysis For Titan Industries PVTDocument15 pagesProject On Ratio and Cash Flow Analysis For Titan Industries PVTRita100% (3)

- 12th HSC Bookkeeping Project On A Report On Adjustments in Partnership Final AccountsDocument8 pages12th HSC Bookkeeping Project On A Report On Adjustments in Partnership Final AccountsKushal Khandelwal71% (7)

- Rajendra Higher Secondary School, Balangir Academic Session 2020-21Document19 pagesRajendra Higher Secondary School, Balangir Academic Session 2020-21aaaa100% (1)

- Yogesh Enterprises Accounts ProjectDocument23 pagesYogesh Enterprises Accounts ProjectVivek Pandey100% (1)

- Prospectus GCCDocument56 pagesProspectus GCCArup RoyNo ratings yet

- CamScanner Document ScansDocument104 pagesCamScanner Document ScansHatim Bohra0% (1)

- Accountancy: Mock PaperDocument24 pagesAccountancy: Mock PaperSuman Bala0% (1)

- BSE SENSEX: India's Benchmark Stock IndexDocument9 pagesBSE SENSEX: India's Benchmark Stock Indexinfinity GOD Gamers100% (2)

- Dissolution QuestionsDocument5 pagesDissolution Questionsstudyystuff7No ratings yet

- Mycbseguide: Class 12 - Business Studies Sample Paper 01Document12 pagesMycbseguide: Class 12 - Business Studies Sample Paper 01Siddhi JainNo ratings yet

- Accountancy Model Project - XiDocument19 pagesAccountancy Model Project - XiHana KabeerNo ratings yet

- 100 QUESTIONS AccountsDocument84 pages100 QUESTIONS AccountsShraddha Bansal100% (1)

- Accountancy ProjectDocument9 pagesAccountancy Projectdeepesh288100% (2)

- Assignment On Financial Statement Analysis Berger Paints: School of Management StudiesDocument26 pagesAssignment On Financial Statement Analysis Berger Paints: School of Management StudiesAlkesh Mishra50% (2)

- Analysis of Pupil Performance: AccountsDocument43 pagesAnalysis of Pupil Performance: AccountsT.K. MukhopadhyayNo ratings yet

- Chapter 1 - Nature and Significance of ManagementDocument6 pagesChapter 1 - Nature and Significance of ManagementSachin Rana0% (1)

- CBSE Accountancy 12th Term 2 CH 2Document4 pagesCBSE Accountancy 12th Term 2 CH 2Nirmal GuptaNo ratings yet

- Kvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Document11 pagesKvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Sanjay PanickerNo ratings yet

- BUSINESS STUDIES CLASS 12 CHAPTER 1 CASE STUDIESDocument7 pagesBUSINESS STUDIES CLASS 12 CHAPTER 1 CASE STUDIESManish Nagdev100% (2)

- Strictly Confidential: (For Internal and Restricted Use Only)Document27 pagesStrictly Confidential: (For Internal and Restricted Use Only)bhaiyarakeshNo ratings yet

- Worksheet Accounts Ut 1 RefrenceDocument10 pagesWorksheet Accounts Ut 1 Refrencemayankkochar216No ratings yet

- AdmissionDocument2 pagesAdmissionshubhamsundraniNo ratings yet

- bc8bc729-727a-4edb-ab45-c3b530d6ba97Document3 pagesbc8bc729-727a-4edb-ab45-c3b530d6ba97shubhamsundraniNo ratings yet

- D.A.V. Public School Practice Set 3 Accountancy TestDocument6 pagesD.A.V. Public School Practice Set 3 Accountancy TestshubhamsundraniNo ratings yet

- D.A.V. Public School Practice Test 5 Accountancy 12th Commerce QuestionsDocument2 pagesD.A.V. Public School Practice Test 5 Accountancy 12th Commerce QuestionsshubhamsundraniNo ratings yet

- Employment: Growth, Informalisation and Other IssuesDocument17 pagesEmployment: Growth, Informalisation and Other IssuesshubhamsundraniNo ratings yet

- Tools of Financial Statement AnalysisDocument164 pagesTools of Financial Statement AnalysisshubhamsundraniNo ratings yet

- BST Case Study CH 1Document3 pagesBST Case Study CH 1Manan Kakkar0% (1)

- Contract of Sale: Franklin Lopez Accounting Education Department Rmmc-MiDocument14 pagesContract of Sale: Franklin Lopez Accounting Education Department Rmmc-MiRazel Tercino100% (2)

- Chapter 12 LiabilitiesDocument5 pagesChapter 12 LiabilitiesAngelica Joy ManaoisNo ratings yet

- Aa - Maple Leaf Cement Factory LTDDocument16 pagesAa - Maple Leaf Cement Factory LTDMubasharNo ratings yet

- UCC IRS Private BankingDocument54 pagesUCC IRS Private BankingScribdTranslationsNo ratings yet

- AdjustmentDocument5 pagesAdjustmentBeta TesterNo ratings yet

- BEP323SN Company Performance1Document12 pagesBEP323SN Company Performance1Ann RedNo ratings yet

- Personal Monthly Budget1Document3 pagesPersonal Monthly Budget1Olivia OctoficeNo ratings yet

- Obligations and Contracts - Domingo AnswersDocument3 pagesObligations and Contracts - Domingo AnswersKristan EstebanNo ratings yet

- MIBG - Malaysian Bank Bonds - 230430Document16 pagesMIBG - Malaysian Bank Bonds - 230430Guan JooNo ratings yet

- Statement of Account: Downloaded OnDocument1 pageStatement of Account: Downloaded OnPritom NasirNo ratings yet

- PMD1D April 15 PDFDocument4 pagesPMD1D April 15 PDFselva priyadharshiniNo ratings yet

- Closing and Worksheet: 20.1 Closing Entries For Revenue AccountsDocument8 pagesClosing and Worksheet: 20.1 Closing Entries For Revenue AccountsZaheer Swati100% (1)

- Accounting Paper 1 Dec 2015Document11 pagesAccounting Paper 1 Dec 2015Sudhan NairNo ratings yet

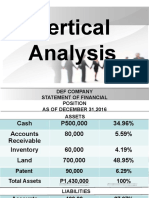

- Vertical analysis of DEF Company's financial statementsDocument8 pagesVertical analysis of DEF Company's financial statementsHannah Mae BautistaNo ratings yet

- Department of Business AdministrationDocument9 pagesDepartment of Business AdministrationKannan NagaNo ratings yet

- Different Loans/Financing Schemes for Rooftop Solar ProjectsDocument4 pagesDifferent Loans/Financing Schemes for Rooftop Solar ProjectsnaveenkumargmrNo ratings yet

- Pledge Real Mortgage Chattel Mortgage AntichresisDocument12 pagesPledge Real Mortgage Chattel Mortgage AntichresisKATHERINEMARIE DIMAUNAHANNo ratings yet

- 201.12 - 2 - Insolvency Act-1997Document3 pages201.12 - 2 - Insolvency Act-1997Biplob K. SannyasiNo ratings yet

- Assignment For FOA - The Trial BalanceDocument2 pagesAssignment For FOA - The Trial Balancekimona webleyNo ratings yet

- Ordinary Annuity ModuleDocument27 pagesOrdinary Annuity ModuleVincent Andrei Dela CruzNo ratings yet

- Laws 1013 - CODE 626 Midterm Quiz ReviewDocument3 pagesLaws 1013 - CODE 626 Midterm Quiz ReviewJinky ValdezNo ratings yet

- MPU 3482 Personal Finance Management Individual Assignment 1Document9 pagesMPU 3482 Personal Finance Management Individual Assignment 1PoogensNo ratings yet

- NCB CREDIT CARD STATEMENT DETAILSDocument2 pagesNCB CREDIT CARD STATEMENT DETAILSRomarioNo ratings yet

- Module 4 BASIC CONSOLIDATION PROCEDURESDocument21 pagesModule 4 BASIC CONSOLIDATION PROCEDURESJuliana ChengNo ratings yet

- Lirag Textile Mills Inc V SSS DigestDocument1 pageLirag Textile Mills Inc V SSS DigestG S100% (1)

- Intermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueDocument8 pagesIntermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueAndrei FajardoNo ratings yet

- m2.2f Diy MCQ Answer KeyDocument6 pagesm2.2f Diy MCQ Answer KeyaapNo ratings yet

- MBA 670 Exam 1Document14 pagesMBA 670 Exam 1Lauren LoshNo ratings yet

- Mathematics SBA For CSECDocument14 pagesMathematics SBA For CSECShivan McdonaldNo ratings yet

- Final Accounts Adjustments in Table FormDocument10 pagesFinal Accounts Adjustments in Table FormRahul JadhavNo ratings yet