You might also like

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- You Exec - Brand Positioning Strategy CompleteDocument18 pagesYou Exec - Brand Positioning Strategy CompleteDianne DimoriNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Basic English Language SkillsDocument59 pagesBasic English Language SkillsShane HtetNo ratings yet

- Chapter 10 Solutions - EugeneDocument8 pagesChapter 10 Solutions - EugeneNabiha KhattakNo ratings yet

- The Cost of CapitalDocument45 pagesThe Cost of CapitalBabasab Patil (Karrisatte)No ratings yet

- Easy Problem Chapter 11Document5 pagesEasy Problem Chapter 11Natally LangfeldtNo ratings yet

- Mathcad - 1000 KL Tank1Document23 pagesMathcad - 1000 KL Tank1Zulfikar N JoelNo ratings yet

- Chap 7 Bodie 9eDocument13 pagesChap 7 Bodie 9eChristan LambertNo ratings yet

- WACC Summary SlidesDocument29 pagesWACC Summary SlidesclaeNo ratings yet

- Tugas 8 - C11 - Cost of CapitalDocument5 pagesTugas 8 - C11 - Cost of CapitalIqbal BaihaqiNo ratings yet

- Zorki - 4k ManualDocument22 pagesZorki - 4k ManualOtto HandNo ratings yet

- FM Assignment 3&4Document5 pagesFM Assignment 3&4kartika tamara maharani100% (1)

- Chapter 7 Portfolio TheoryDocument44 pagesChapter 7 Portfolio Theorysharktale2828100% (1)

- Tugas Accounting and Finance Bab 2 Setelah UtsDocument6 pagesTugas Accounting and Finance Bab 2 Setelah UtsbogitugasNo ratings yet

- Chapter 10 SolutionsDocument8 pagesChapter 10 Solutionsalice123h2150% (2)

- Solutions To End-Of-Chapter Problems 11Document6 pagesSolutions To End-Of-Chapter Problems 11weeeeeshNo ratings yet

- Ch09 - Cost of Capital 12112020 125813pmDocument13 pagesCh09 - Cost of Capital 12112020 125813pmMuhammad Umar BashirNo ratings yet

- Industrial Water Recycle/reuse: Jir I Jaromı R KlemesDocument8 pagesIndustrial Water Recycle/reuse: Jir I Jaromı R KlemesHenrique Martins TavaresNo ratings yet

- MAFIN AssignmentDocument2 pagesMAFIN AssignmentEms DelRosario100% (3)

- CITP SpecificationDocument21 pagesCITP SpecificationItay GalNo ratings yet

- Cost of CapitalDocument56 pagesCost of CapitalAndayani SalisNo ratings yet

- 5 - Cost of CapitalDocument6 pages5 - Cost of CapitaloryzanoviaNo ratings yet

- Extra Excise Final NewestDocument6 pagesExtra Excise Final NewestMinh ThiNo ratings yet

- Tugas Kelompok 3Document4 pagesTugas Kelompok 3Bought By UsNo ratings yet

- Long QuestionsDocument18 pagesLong Questionssaqlainra50% (2)

- HW4Document5 pagesHW4mosesNo ratings yet

- Corporate Finance Study Guide Spring 2013 Part 2Document20 pagesCorporate Finance Study Guide Spring 2013 Part 2Ehab M. Abdel HadyNo ratings yet

- S5 Risk Return Online VersionDocument20 pagesS5 Risk Return Online Versionconstruction omanNo ratings yet

- Chapter 12 - ET3Document6 pagesChapter 12 - ET3anthony.schzNo ratings yet

- Bu8201 Tutorial 7 Presentation - FinalDocument32 pagesBu8201 Tutorial 7 Presentation - FinalArvin LiangdyNo ratings yet

- Financial Management Revision Notes 2023-24Document163 pagesFinancial Management Revision Notes 2023-24Shermaine ChuaNo ratings yet

- Chap 10 SolutionsDocument6 pagesChap 10 SolutionsayeshadarlingNo ratings yet

- Chap 1 - Portfolio Risk and Return Part1Document91 pagesChap 1 - Portfolio Risk and Return Part1eya feguiriNo ratings yet

- Lecture 5Document25 pagesLecture 5tse maNo ratings yet

- 4 - Cost of CapitalDocument10 pages4 - Cost of Capitalramit_madan7372No ratings yet

- Tut5 - With MemoDocument6 pagesTut5 - With Memoapi-370823186% (7)

- Chapter Six Risk and ReturnDocument46 pagesChapter Six Risk and ReturnLetaNo ratings yet

- Chapter - 9: Solutions - To - End - of - Chapter - 9 - Problems - On - Estimating - Cost - of - CapitalDocument7 pagesChapter - 9: Solutions - To - End - of - Chapter - 9 - Problems - On - Estimating - Cost - of - CapitalMASPAKNo ratings yet

- Bkm9e Answers Chap007Document12 pagesBkm9e Answers Chap007AhmadYaseenNo ratings yet

- WaccDocument33 pagesWaccAnkitNo ratings yet

- Cost of Capital 2020Document29 pagesCost of Capital 2020Sai Swaroop MandalNo ratings yet

- Return and Risk On Two Assets PortfolioDocument24 pagesReturn and Risk On Two Assets PortfolioHarsh GuptaNo ratings yet

- Kewangan Korporat LatihanDocument4 pagesKewangan Korporat LatihanfahmiyyahNo ratings yet

- FormulasDocument7 pagesFormulaskasimgenelNo ratings yet

- ACFI5084 (0) Mock SolutionDocument12 pagesACFI5084 (0) Mock SolutionLaraib SalmanNo ratings yet

- Tugas Accounting Finance 4 - Kelompok 3Document5 pagesTugas Accounting Finance 4 - Kelompok 3safira larasNo ratings yet

- Cost of Capital Tut. MemoDocument2 pagesCost of Capital Tut. MemoSEKEETHA DE NOBREGANo ratings yet

- AnswerDocument13 pagesAnswerEhab M. Abdel HadyNo ratings yet

- Assignment 1 Kelompok 3Document15 pagesAssignment 1 Kelompok 3iyanNo ratings yet

- 2assetallocation (9) 1vmodr11cDocument61 pages2assetallocation (9) 1vmodr11cGabriel PodolskyNo ratings yet

- Finance NoteDocument19 pagesFinance NoteHui YiNo ratings yet

- The Cost of Capital: Answers To Seleected End-Of-Chapter QuestionsDocument9 pagesThe Cost of Capital: Answers To Seleected End-Of-Chapter QuestionsTalha JavedNo ratings yet

- Cost of CapitalDocument19 pagesCost of CapitalChintan KeniaNo ratings yet

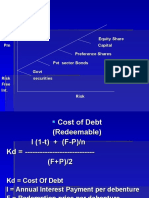

- Risk Equity Share PM Capital Preference Shares PVT Sector Bonds Govt Risk Securities Free Int. RiskDocument12 pagesRisk Equity Share PM Capital Preference Shares PVT Sector Bonds Govt Risk Securities Free Int. RiskrajjoNo ratings yet

- GCIF - Parte II IIIDocument94 pagesGCIF - Parte II IIIJose Pinto de AbreuNo ratings yet

- Fin 221 - WACC TutorialDocument18 pagesFin 221 - WACC TutorialPranav Pratap SinghNo ratings yet

- Financial Management ExercisesDocument11 pagesFinancial Management ExercisesDonat NabahunguNo ratings yet

- Chapter 7 Portfolio TheoryDocument41 pagesChapter 7 Portfolio TheoryRupesh DhindeNo ratings yet

- ch14 SolDocument16 pagesch14 SolAnsleyNo ratings yet

- Stocks AnalysisDocument9 pagesStocks AnalysisHoàng PhạmNo ratings yet

- CH 04Document12 pagesCH 04Mai NguyễnNo ratings yet

- CH 02Document48 pagesCH 02Harsh DhawanNo ratings yet

- WACCDocument36 pagesWACCBarakaNo ratings yet

- Valuation of SecuritiesDocument31 pagesValuation of Securitiesmansi sainiNo ratings yet

- Investment Conditions Druing Covid-19Document20 pagesInvestment Conditions Druing Covid-19zakaria kerboubNo ratings yet

- Pre FDocument1 pagePre Fzakaria kerboubNo ratings yet

- The Impact of UkraineDocument1 pageThe Impact of Ukrainezakaria kerboubNo ratings yet

- CV RahulDocument1 pageCV Rahulzakaria kerboubNo ratings yet

- Webster Smart Shopper PDFDocument36 pagesWebster Smart Shopper PDFPete SearsNo ratings yet

- Tadlak Elementary School Tle (Ict) 2 QTR Week 6Document3 pagesTadlak Elementary School Tle (Ict) 2 QTR Week 6Rowena Casonete Dela Torre100% (1)

- Preliminary Energy Audit Methodology Preliminary Energy Audit Is A Relatively Quick Exercise ToDocument1 pagePreliminary Energy Audit Methodology Preliminary Energy Audit Is A Relatively Quick Exercise Tojons ndruwNo ratings yet

- Designing For Self-Tracking of Emotion and ExperienceDocument11 pagesDesigning For Self-Tracking of Emotion and ExperienceDAVID GOMEZNo ratings yet

- Digitalization in The Financial StatementsDocument12 pagesDigitalization in The Financial Statementsrockylie717No ratings yet

- Reference Only: I Pus Pond StreetDocument132 pagesReference Only: I Pus Pond StreetJagdish ShindeNo ratings yet

- Guus Houttuin Alina Boiciuc: The SOCFIN Case From A Human Rights Perspective" (Document3 pagesGuus Houttuin Alina Boiciuc: The SOCFIN Case From A Human Rights Perspective" (FIDHNo ratings yet

- Scheme - I Sample Question Paper: Program Name: Diploma in Plastic EngineeringDocument4 pagesScheme - I Sample Question Paper: Program Name: Diploma in Plastic EngineeringAmit GhadeNo ratings yet

- Ps Course - Elee3260 - Uoit - Lec 2Document64 pagesPs Course - Elee3260 - Uoit - Lec 2ksajjNo ratings yet

- Ict351 4 Logical FormulasDocument32 pagesIct351 4 Logical FormulastheoskatokaNo ratings yet

- Audiolingual Method (Alm) : Elt MethodologyDocument11 pagesAudiolingual Method (Alm) : Elt Methodologyrm53No ratings yet

- Two Flavor OscillationDocument36 pagesTwo Flavor OscillationSheheryarZaheerNo ratings yet

- Power Macintosh 9600/200 and 9600/200MPDocument2 pagesPower Macintosh 9600/200 and 9600/200MPscriNo ratings yet

- ME ProgramDocument21 pagesME Programadyro12No ratings yet

- Adobe AnalyticsDocument17 pagesAdobe AnalyticsGourav ChakrabortyNo ratings yet

- 22kV Heat Shrink MV Transition Cable Joints For 3C PILC To 3 Single Core XLPE Cables Nexans GTM3.1Document2 pages22kV Heat Shrink MV Transition Cable Joints For 3C PILC To 3 Single Core XLPE Cables Nexans GTM3.1desai_sachin07No ratings yet

- HSE L141 - 2005 - Whole-Body VibrationDocument56 pagesHSE L141 - 2005 - Whole-Body VibrationKris WilochNo ratings yet

- Introduction To DeivativesDocument44 pagesIntroduction To Deivativesanirbanccim8493No ratings yet

- A Proposed Medium-Term Development Plan For Data Center College of The Philippines Laoag City CampusDocument3 pagesA Proposed Medium-Term Development Plan For Data Center College of The Philippines Laoag City Campussheng cruzNo ratings yet

- Characters Numerals Size Number of Pages: Amrlipi (Amarlipi)Document183 pagesCharacters Numerals Size Number of Pages: Amrlipi (Amarlipi)ggn11No ratings yet

- Electrochemical Frequency Modulation Software: TheoryDocument4 pagesElectrochemical Frequency Modulation Software: TheoryDuvan CoronadoNo ratings yet

- MCA Syllabus - 1st Sem PDFDocument32 pagesMCA Syllabus - 1st Sem PDFshatabdi mukherjeeNo ratings yet

- Stormbrixx - Fisa TehnicaDocument108 pagesStormbrixx - Fisa Tehnicamureseanu_deliaNo ratings yet

- Telephone Directory 2018Document6 pagesTelephone Directory 2018CLO GENSANNo ratings yet