You might also like

- 9f1 - 20% Cash & 80% Bank FinancingDocument1 page9f1 - 20% Cash & 80% Bank FinancingArvin Amiel LiceraldeNo ratings yet

- August 20 - Notes PayableDocument4 pagesAugust 20 - Notes PayableRodolfo Jr. LasquiteNo ratings yet

- Annual Report 2022 en Final WebsiteDocument76 pagesAnnual Report 2022 en Final WebsiteSin SeutNo ratings yet

- Assignment 5.3 Note PayableDocument4 pagesAssignment 5.3 Note PayableJohn Williever GonzalezNo ratings yet

- Performance Analysis Performance Analysis: Q3 FY 2020 Q2 FY 2021Document37 pagesPerformance Analysis Performance Analysis: Q3 FY 2020 Q2 FY 2021Mahesh DhalNo ratings yet

- Shantanu FadmDocument12 pagesShantanu FadmHimanshuNo ratings yet

- FM Must Do List!! May - 2023 (1) - 230501 - 220727Document86 pagesFM Must Do List!! May - 2023 (1) - 230501 - 220727Regan DcunhaNo ratings yet

- Tugas AKM 2 Proportional MetodeDocument3 pagesTugas AKM 2 Proportional MetodeSheny WulandariNo ratings yet

- Morrison and Sainsburry RatioDocument5 pagesMorrison and Sainsburry RatioTariq KhanNo ratings yet

- Britannia 1Document40 pagesBritannia 1Dipesh GuptaNo ratings yet

- Fund Planning ScheduleDocument46 pagesFund Planning Schedulemonir_jokkyNo ratings yet

- AACONAPPS2 A433 - Audit of ReceivablesDocument23 pagesAACONAPPS2 A433 - Audit of ReceivablesDawson Dela CruzNo ratings yet

- Backus Valuation ExcelDocument28 pagesBackus Valuation ExcelAdrian MontoyaNo ratings yet

- NG Debt Press Release June 2023 1Document2 pagesNG Debt Press Release June 2023 1Ma. Theresa BerdanNo ratings yet

- Basic Rental Analysis WorksheetDocument8 pagesBasic Rental Analysis WorksheetGleb petukhovNo ratings yet

- Gonzalez, John Williever A. - Assignment 4.1 Investment in Debt SecuritiesDocument5 pagesGonzalez, John Williever A. - Assignment 4.1 Investment in Debt SecuritiesJohn Williever GonzalezNo ratings yet

- Ssi Securities Corporation 4Q2020 Earnings ReleaseDocument11 pagesSsi Securities Corporation 4Q2020 Earnings ReleaseHoàng HiệpNo ratings yet

- PresentationSSI - 2q2020-Earnings-ReleaseDocument10 pagesPresentationSSI - 2q2020-Earnings-ReleaseHoàng HiệpNo ratings yet

- New Microsoft Excel WorksheetDocument3 pagesNew Microsoft Excel WorksheetARIFNo ratings yet

- Quiz Box 2 - QuestionnairesDocument13 pagesQuiz Box 2 - QuestionnairesCamila Mae AlduezaNo ratings yet

- BRS Economic Update - SL Budget 2024Document22 pagesBRS Economic Update - SL Budget 2024Sudheera IndrajithNo ratings yet

- Contoh Gabungan Tugas A Kelas ZZZDocument189 pagesContoh Gabungan Tugas A Kelas ZZZMariaGeovana PingNo ratings yet

- Case Assignment 8 - Diamond Energy Resources PDFDocument3 pagesCase Assignment 8 - Diamond Energy Resources PDFAudrey Ang100% (1)

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- Case 1 Action STDD Batch 21 2022 JanDocument5 pagesCase 1 Action STDD Batch 21 2022 JanS TMNo ratings yet

- Bài tập về nhà - Trang tính1Document3 pagesBài tập về nhà - Trang tính1namhua54No ratings yet

- Problem 1: ComputationsDocument6 pagesProblem 1: ComputationsClarissa BorbonNo ratings yet

- Downgrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsDocument8 pagesDowngrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsJNo ratings yet

- Twice Incorporated: Percentage of Recov For USC W/o 35%Document4 pagesTwice Incorporated: Percentage of Recov For USC W/o 35%Paolo LocquiaoNo ratings yet

- SFH Rental AnalysisDocument6 pagesSFH Rental AnalysisA jNo ratings yet

- Province of Chubut 29.09.2020 VF2Document13 pagesProvince of Chubut 29.09.2020 VF2Nicolas GrossNo ratings yet

- Assignment 2Document2 pagesAssignment 2Amna AbdallahNo ratings yet

- Davelouis LTD: Sales $24,750,000 $25,368,750 Costs and Expenses $8,910,000 $9,640,125 Tax (25%) $6,682,500 $7,230,094Document6 pagesDavelouis LTD: Sales $24,750,000 $25,368,750 Costs and Expenses $8,910,000 $9,640,125 Tax (25%) $6,682,500 $7,230,094Josué LeónNo ratings yet

- Solvency Position: 1. Debt-Equity RatioDocument5 pagesSolvency Position: 1. Debt-Equity RatioShilpiNo ratings yet

- City of Fort St. John - 2023-2027 Operating BudgetDocument30 pagesCity of Fort St. John - 2023-2027 Operating BudgetAlaskaHighwayNewsNo ratings yet

- Underwriting Report-Week Ending 03 September 2020Document12 pagesUnderwriting Report-Week Ending 03 September 2020Emmanuel MonzeNo ratings yet

- Exercises Module 3Document12 pagesExercises Module 3jpNo ratings yet

- Problem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Document4 pagesProblem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Merry Kriss RiveraNo ratings yet

- NG Debt Press Release December 2018 - Ed 2 PDFDocument2 pagesNG Debt Press Release December 2018 - Ed 2 PDFROXAN magalingNo ratings yet

- Accounting Final ProjectDocument15 pagesAccounting Final ProjectSam KhalilNo ratings yet

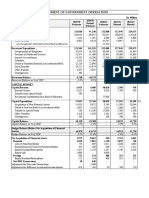

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Document2 pagesStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatNo ratings yet

- Paramount Textile PLC Ratio Analysis FinalDocument16 pagesParamount Textile PLC Ratio Analysis Finalraufun huda dipNo ratings yet

- Finanical SpreadsDocument11 pagesFinanical Spreadsnauman farooqNo ratings yet

- Calculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Document1 pageCalculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Prachi NavghareNo ratings yet

- Answer Key Final Exam IA 2Document4 pagesAnswer Key Final Exam IA 2Carlos arnaldo lavadoNo ratings yet

- Q42022 Results Press ReleaseDocument40 pagesQ42022 Results Press ReleaseAditya DeshpandeNo ratings yet

- Uol Group Fy2020 Results 26 FEBRUARY 2021Document33 pagesUol Group Fy2020 Results 26 FEBRUARY 2021Pat KwekNo ratings yet

- Practice - Problem Set - Week 4 SolutionsDocument3 pagesPractice - Problem Set - Week 4 SolutionsShravan DeshmukhNo ratings yet

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- DSCR CalculationDocument2 pagesDSCR CalculationusmanthesaviorNo ratings yet

- 2020 10 07 PH S Bdo PDFDocument7 pages2020 10 07 PH S Bdo PDFJNo ratings yet

- AmSpa Financials 150222Document59 pagesAmSpa Financials 150222Amelia SmithNo ratings yet

- CC 0742 - 2031 AnnuityDocument1 pageCC 0742 - 2031 AnnuityterrygohNo ratings yet

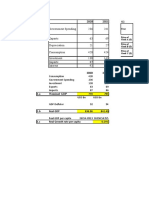

- Government Spending 236 241 Exports 63 69 Depreciation 21 27 Consumption 420 424 Investment 138 143 Imports 87 86 Interest 92 84Document2 pagesGovernment Spending 236 241 Exports 63 69 Depreciation 21 27 Consumption 420 424 Investment 138 143 Imports 87 86 Interest 92 84DivyaNo ratings yet

- Forward PE Rp34,524 Rp27,704 Simplified DCF Rp28,520 Rp26,180Document19 pagesForward PE Rp34,524 Rp27,704 Simplified DCF Rp28,520 Rp26,180Wahid Arief AuladyNo ratings yet

- Analysis of ProfitDocument14 pagesAnalysis of ProfitmahaNo ratings yet

- Forward PE Rp34,524 Rp27,704 Simplified DCF Rp28,520 Rp26,180Document19 pagesForward PE Rp34,524 Rp27,704 Simplified DCF Rp28,520 Rp26,180Wahid Arief AuladyNo ratings yet

- RMC No. 11-2024 - Annex A - Illustrations and Accounting EntriesDocument3 pagesRMC No. 11-2024 - Annex A - Illustrations and Accounting EntriesAnostasia NemusNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- L1tax Eoy Exam P2 - Solution Final-GridDocument18 pagesL1tax Eoy Exam P2 - Solution Final-GridStanleyNo ratings yet

- L1-P2 Dry-Run Script 3Document13 pagesL1-P2 Dry-Run Script 3StanleyNo ratings yet

- L1-P2 Dry-Run Script 2Document12 pagesL1-P2 Dry-Run Script 2StanleyNo ratings yet

- L1 P2 Dry-Run Script 1Document12 pagesL1 P2 Dry-Run Script 1StanleyNo ratings yet

- Flowchart FinanceDocument1 pageFlowchart FinanceMark Anthony OrasaNo ratings yet

- Akuntansi Keuangan 2 - Semester 4Document13 pagesAkuntansi Keuangan 2 - Semester 4Andrew AlamsyahNo ratings yet

- List of Top UAE CompaniesDocument8 pagesList of Top UAE CompaniesTauheedalHasan58% (19)

- Medical Office Manager Resume SamplesDocument8 pagesMedical Office Manager Resume Samplesxdkankjbf100% (2)

- Micro Perspective Semi Finals - The Mice IndustryDocument22 pagesMicro Perspective Semi Finals - The Mice IndustrySole HiuNo ratings yet

- Supply Chain Management PDFDocument78 pagesSupply Chain Management PDFSahil GargNo ratings yet

- BP 1111 To BP 1135 Road Work NIT PDFDocument124 pagesBP 1111 To BP 1135 Road Work NIT PDFRamesh HadiyaNo ratings yet

- 2-Minutes Noodle S: Presented By: - Meghna P - Goldy Hirawat - Manish Negi - Ashis Kyal - Deepak Rai - Poonam MishraDocument16 pages2-Minutes Noodle S: Presented By: - Meghna P - Goldy Hirawat - Manish Negi - Ashis Kyal - Deepak Rai - Poonam MishraShubham SinghNo ratings yet

- SHOPPING (EP1-week 1)Document11 pagesSHOPPING (EP1-week 1)Athirah Fadzil100% (1)

- Hierarchy of MetricsDocument5 pagesHierarchy of MetricsRam PowruNo ratings yet

- 3.2 Ma Elec 1Document34 pages3.2 Ma Elec 1rubilyn bukingNo ratings yet

- Case Study - Freight Calculation - Full Container LoadDocument2 pagesCase Study - Freight Calculation - Full Container LoadVaishali KiranNo ratings yet

- NTCC On Interior DesigningDocument20 pagesNTCC On Interior DesigningMohitAgarwalNo ratings yet

- Training Analysis: Kavitha JaganathanDocument5 pagesTraining Analysis: Kavitha JaganathanKavi KavithaNo ratings yet

- Cross-Functional CompetenciesDocument2 pagesCross-Functional Competenciesasdkhn khnNo ratings yet

- Tugas 3 - Teori Pengambilan Keputusan - Yusriani Syam - A021181033Document5 pagesTugas 3 - Teori Pengambilan Keputusan - Yusriani Syam - A021181033Yusriani SyamNo ratings yet

- Citibank Case Study Group1Document11 pagesCitibank Case Study Group1Deepaksayu100% (1)

- ABC, Transfer, DifferentialDocument3 pagesABC, Transfer, DifferentialLeoreyn Faye MedinaNo ratings yet

- Reading Test. DiagnosticDocument32 pagesReading Test. DiagnostichectorNo ratings yet

- Project Brief-Establishment or Construction of ToDocument2 pagesProject Brief-Establishment or Construction of ToJomidy MidtanggalNo ratings yet

- Service Quality Delivery and Its Impact On Customer Satisfaction in The Bank Services in Tanzania: The Case of Moshi Uchumi Commercial BankDocument90 pagesService Quality Delivery and Its Impact On Customer Satisfaction in The Bank Services in Tanzania: The Case of Moshi Uchumi Commercial Bankkitderoger_391648570No ratings yet

- Marlboro BrandingDocument11 pagesMarlboro BrandingSURYA TEJA DASARINo ratings yet

- CA FINAL IDT QUESTION BANK FOR MAYNOV 2021 Atul AgarwalDocument463 pagesCA FINAL IDT QUESTION BANK FOR MAYNOV 2021 Atul AgarwalRonita DuttaNo ratings yet

- Tata InventoryDocument16 pagesTata InventoryHemza BrikaNo ratings yet

- Legacy Letter - Goap ShareDocument3 pagesLegacy Letter - Goap Sharebunny4dare1No ratings yet

- Industry Analysis: Restaurant Industry Restaurant IndustryDocument8 pagesIndustry Analysis: Restaurant Industry Restaurant Industryafsana0% (1)

- Peter DruckerDocument12 pagesPeter DruckerNicholas FeatherstonNo ratings yet

- Managers - We Are Katti With You - DarpanDocument2 pagesManagers - We Are Katti With You - DarpanDarpan ChoudharyNo ratings yet

- Far Problems With SolutionsDocument8 pagesFar Problems With Solutionspatricia abbygail parbaNo ratings yet