You might also like

- Gale Researcher Guide for: Independence, Abolition, and Emancipation in BrazilFrom EverandGale Researcher Guide for: Independence, Abolition, and Emancipation in BrazilNo ratings yet

- Readings in Philippine History Evolution of Philippine TaxationDocument4 pagesReadings in Philippine History Evolution of Philippine TaxationAngel Joseph Tejada100% (1)

- Taxation in Spanish Philippines: Evolution of Philippine TaxationDocument16 pagesTaxation in Spanish Philippines: Evolution of Philippine TaxationC. I .ANo ratings yet

- Evolution of PH TaxationDocument45 pagesEvolution of PH TaxationShai Anne CortezNo ratings yet

- Philippine TaxationDocument8 pagesPhilippine TaxationglenswaberNo ratings yet

- HistoryDocument29 pagesHistorysheridaNo ratings yet

- Lesson 7 - Evolution of Philippine TaxationDocument8 pagesLesson 7 - Evolution of Philippine TaxationDe Lanxi FerrerNo ratings yet

- M4-Lesson 3 - REPORT ASSIGNINGDocument11 pagesM4-Lesson 3 - REPORT ASSIGNINGRizalyn SunquitNo ratings yet

- Evolution of The Philippine Taxation, Taxation in Spanish PhilippinesDocument12 pagesEvolution of The Philippine Taxation, Taxation in Spanish PhilippinesAnge Napalia100% (2)

- GEC 2 Week 12 Learning ModuleDocument9 pagesGEC 2 Week 12 Learning ModuleGritchen PontinoNo ratings yet

- Inbound 4798636164886756082Document3 pagesInbound 4798636164886756082Ivan RobleNo ratings yet

- Evolution of Philippine TaxationDocument4 pagesEvolution of Philippine Taxationyumi timtim50% (2)

- Evolution of Philippine Agrarian Reform and TaxationDocument25 pagesEvolution of Philippine Agrarian Reform and Taxationrailgun 17100% (5)

- 21 24 PDFDocument2 pages21 24 PDFRosebie Dlsrys IINo ratings yet

- W13-Module13 Social, Political, Economic and Cultural Issues in Philippine HistoryDocument9 pagesW13-Module13 Social, Political, Economic and Cultural Issues in Philippine HistoryDorson AdoraNo ratings yet

- 13 PDFDocument9 pages13 PDFJhona NinalgaNo ratings yet

- Yumol (Evolution and Spanish Taxation)Document3 pagesYumol (Evolution and Spanish Taxation)Jellian Eunice GerundioNo ratings yet

- Taxation FinalDocument16 pagesTaxation FinalGhetto Spider100% (1)

- MARIANO HERBOSA-WPS OfficeDocument7 pagesMARIANO HERBOSA-WPS OfficeMaturan, Ma. Kayesha Camille A.No ratings yet

- Monopoly of Goverment OfficialsDocument12 pagesMonopoly of Goverment OfficialsYuvia KeithleyreNo ratings yet

- Evolution of Philippine TaxationDocument62 pagesEvolution of Philippine TaxationSapphire Yabo100% (4)

- Module 2 Lesson 2.2Document9 pagesModule 2 Lesson 2.2Cherry Mae VlogNo ratings yet

- History of Taxation in The PhilippinesDocument4 pagesHistory of Taxation in The PhilippinesAngelica EstacionNo ratings yet

- Hist1 BC2 TIU M4 L9 PDFDocument1 pageHist1 BC2 TIU M4 L9 PDFOvelia KayuzakiNo ratings yet

- TAXATION BEGAN WITH FOREIGN CONQUESTDocument6 pagesTAXATION BEGAN WITH FOREIGN CONQUESTGonzales, Alethea I.No ratings yet

- Evolution of TaxationDocument52 pagesEvolution of Taxationrixzylicoqui.salcedoNo ratings yet

- analysisDocument5 pagesanalysis2301106378No ratings yet

- Phil. History Module 14Document10 pagesPhil. History Module 14Janice Florece ZantuaNo ratings yet

- Economic Policies of Spain 1Document2 pagesEconomic Policies of Spain 1Arjix HandyMan50% (2)

- Philippines Under Imperial SpainDocument2 pagesPhilippines Under Imperial SpainLynzXD100% (1)

- Readings in Philippine HistoryDocument2 pagesReadings in Philippine HistoryMika EllaNo ratings yet

- Developments Under Spanish OccupationDocument21 pagesDevelopments Under Spanish OccupationFreda Lyn Elicanal PenolboNo ratings yet

- The Evolution of Philippine TaxationDocument54 pagesThe Evolution of Philippine TaxationIson, Marc Ervin A.No ratings yet

- Taxation EvolutionDocument7 pagesTaxation EvolutionSherry Mhay BongcayaoNo ratings yet

- Taxation Spanish EraDocument2 pagesTaxation Spanish EramaryroseNo ratings yet

- Evolution of Philippine TaxationDocument11 pagesEvolution of Philippine TaxationJosh Lozada100% (4)

- Chapter 6 Taxation-In-The-PhilippinesDocument12 pagesChapter 6 Taxation-In-The-PhilippinesLarry BugaringNo ratings yet

- GERPH MODULE 4 Lesson 3Document10 pagesGERPH MODULE 4 Lesson 3mmenguito.k12044178No ratings yet

- Analysis Paper History TaxationDocument6 pagesAnalysis Paper History TaxationKai V LenciocoNo ratings yet

- Reflection On The Evolution of Philippine TaxationDocument1 pageReflection On The Evolution of Philippine TaxationMARY GRACE ABUYABOR100% (3)

- Philippine Taxation Under American PeriodDocument4 pagesPhilippine Taxation Under American PeriodRalph Jayson82% (28)

- Hist1 M4 L9 TaxationDocument9 pagesHist1 M4 L9 TaxationpehikNo ratings yet

- Evolution of Philippine Taxation from Spanish Colonial Era to PresentDocument40 pagesEvolution of Philippine Taxation from Spanish Colonial Era to PresentNessa BautistaNo ratings yet

- TAXATION UNDER SPANISH RULEDocument6 pagesTAXATION UNDER SPANISH RULERowell Carlos50% (2)

- Intro To Pol Gov Lesson 1Document7 pagesIntro To Pol Gov Lesson 1Marianne Josel ValladoresNo ratings yet

- Evolution of Taxation in The PhilippinesDocument10 pagesEvolution of Taxation in The PhilippinesCarlos Baul DavidNo ratings yet

- Historical Development of of Taxation Principles and Law in KenyaDocument17 pagesHistorical Development of of Taxation Principles and Law in KenyaJustus AmitoNo ratings yet

- 04 TSK Performance 1 (RPH)Document3 pages04 TSK Performance 1 (RPH)Ashley AquinoNo ratings yet

- Spanish Forced Labor in the Philippines Crippled Local IndustriesDocument3 pagesSpanish Forced Labor in the Philippines Crippled Local IndustriesannaNo ratings yet

- PHILGOV - The Philippines Under Spanish Rule 2Document4 pagesPHILGOV - The Philippines Under Spanish Rule 2sirshanelaongNo ratings yet

- Lesson 2 - THE 19TH CENTURY PHILIPPINES AS RIZAL'S CONTEXTDocument3 pagesLesson 2 - THE 19TH CENTURY PHILIPPINES AS RIZAL'S CONTEXTmarco ogsila verderaNo ratings yet

- Evolution of Philippine TaxationDocument36 pagesEvolution of Philippine Taxationrocel ordoyoNo ratings yet

- Beige Scrapbook Art and History Museum Presentation_20240313_201157_0000Document28 pagesBeige Scrapbook Art and History Museum Presentation_20240313_201157_0000Jamaicah TumaponNo ratings yet

- The Rise of the Chinese Mestizos in 19th Century PhilippinesDocument23 pagesThe Rise of the Chinese Mestizos in 19th Century Philippinesmaricrisandem100% (1)

- Spanish Colonial Economic Policies in the PhilippinesDocument2 pagesSpanish Colonial Economic Policies in the Philippinesrichard canlasNo ratings yet

- Saint Ferdinand College Module Explores 19th Century Philippine Economy, Society and Chinese MestizosDocument3 pagesSaint Ferdinand College Module Explores 19th Century Philippine Economy, Society and Chinese MestizosPrincess Joy HidalgoNo ratings yet

- AnaroseDocument4 pagesAnaroseJames AbuyogNo ratings yet

- The 19th Century Philippine Economy, Society, and The Chinese MestizosDocument14 pagesThe 19th Century Philippine Economy, Society, and The Chinese MestizosBryle Keith TamposNo ratings yet

- Taxation During Spanish ColonizationDocument44 pagesTaxation During Spanish Colonizationgladyl bermioNo ratings yet

- Evolution of Philippine Taxation from Spanish Colonial Era to PresentDocument40 pagesEvolution of Philippine Taxation from Spanish Colonial Era to PresentNessa BautistaNo ratings yet

- STS 101 Exam CoverageDocument3 pagesSTS 101 Exam CoverageNessa BautistaNo ratings yet

- Policies On Agrarian ReformDocument30 pagesPolicies On Agrarian ReformNessa BautistaNo ratings yet

- NSTPDocument18 pagesNSTPNessa BautistaNo ratings yet

- Policies On Agrarian Reform - HandoutDocument10 pagesPolicies On Agrarian Reform - HandoutNessa BautistaNo ratings yet

- Electromagnitic InductionDocument46 pagesElectromagnitic InductionNessa BautistaNo ratings yet

- Earths LayersDocument18 pagesEarths LayersNessa BautistaNo ratings yet

- Esp Gawain 5Document1 pageEsp Gawain 5Nessa BautistaNo ratings yet

- How Can I Overcome Discrimination?Document1 pageHow Can I Overcome Discrimination?Nessa BautistaNo ratings yet

- Math10 LM U1Document103 pagesMath10 LM U1Nylma Mae Barce100% (1)

- Tat ATO 2022Document3 pagesTat ATO 2022Tate chanNo ratings yet

- Eagle Localization MexicanRequirementsDocument36 pagesEagle Localization MexicanRequirementsAgnaldo GomesNo ratings yet

- 4.1accruals Prepayments Lecture Notes Student Versio4nDocument6 pages4.1accruals Prepayments Lecture Notes Student Versio4nDarshna KumariNo ratings yet

- Individual TaxpayersDocument3 pagesIndividual TaxpayersJoy Orena100% (2)

- TaxationDocument3 pagesTaxationMegumi HideyukiNo ratings yet

- CIR vs. Algue, Inc.Document2 pagesCIR vs. Algue, Inc.Leyard100% (1)

- Thematic Audit of GST Refunds SOP 28.06.22Document14 pagesThematic Audit of GST Refunds SOP 28.06.22Sujit Srikantan100% (1)

- فعالية السياسة المالية ودورها في تحقيق التوازن الاقتصاديDocument28 pagesفعالية السياسة المالية ودورها في تحقيق التوازن الاقتصاديwaliddelimi31No ratings yet

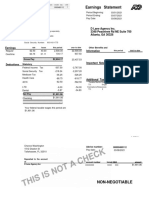

- Earnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Document1 pageEarnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Muhammad AdeelNo ratings yet

- Jonah Bey Notes IIDocument1 pageJonah Bey Notes IINoah Body96% (24)

- Payment of Bonus Form A B C and DDocument13 pagesPayment of Bonus Form A B C and DAmarjeet singhNo ratings yet

- IRFAN AHMAD S/O IKHLAQ AHMAD'S ELECTRICITY BILL FOR JULY 2021Document1 pageIRFAN AHMAD S/O IKHLAQ AHMAD'S ELECTRICITY BILL FOR JULY 2021ahsanNo ratings yet

- Midterm Exam Principles of Taxation and Income TaxationDocument6 pagesMidterm Exam Principles of Taxation and Income TaxationKitagawa, Misia Sophia Jan B.No ratings yet

- Flipkart Labels 26 Mar 2022 11 44Document1 pageFlipkart Labels 26 Mar 2022 11 44Yash ViraniNo ratings yet

- Introduction To Business TaxesDocument32 pagesIntroduction To Business TaxesGracelle Mae Oraller100% (2)

- Accounting Fundamentals II: Lesson 11 (Printer-Friendly Version)Document8 pagesAccounting Fundamentals II: Lesson 11 (Printer-Friendly Version)gretatamaraNo ratings yet

- Go 67 - GSTDocument4 pagesGo 67 - GSTPrabhakar PothunuriNo ratings yet

- TAX II OUTLINEupdated 2020cleanDocument14 pagesTAX II OUTLINEupdated 2020cleanAsia WyNo ratings yet

- Taxation-Final PreboardDocument12 pagesTaxation-Final PreboardPatrice De CastroNo ratings yet

- Problem Solutions - Taxation (Buckwold 2016-2017)Document142 pagesProblem Solutions - Taxation (Buckwold 2016-2017)Raquel Vandermeulen73% (11)

- Filling Up Forms AccuratelyDocument51 pagesFilling Up Forms AccuratelydanteNo ratings yet

- 0153 0166 TradeportDocument5 pages0153 0166 TradeportHARSHAL MITTALNo ratings yet

- Us Tax OrganizerDocument3 pagesUs Tax Organizerscribd9710No ratings yet

- Protest Letter Tax AssessmentDocument2 pagesProtest Letter Tax AssessmentConsciousness Vivid100% (1)

- GST List of PatchesDocument13 pagesGST List of PatchesdurairajNo ratings yet

- Solved Denim Corporation Declares A Nontaxable Dividend Payable in Rights ToDocument1 pageSolved Denim Corporation Declares A Nontaxable Dividend Payable in Rights ToAnbu jaromiaNo ratings yet

- Income Taxation Mamalateo NotesDocument19 pagesIncome Taxation Mamalateo Notesclandestine2684100% (1)

- Marilou B. Franco San Francisco, Agusan Del Sur: (In Philippine Pesos)Document6 pagesMarilou B. Franco San Francisco, Agusan Del Sur: (In Philippine Pesos)ATRIYO ENTERPRISESNo ratings yet

- Tax Invoice DetailsDocument1 pageTax Invoice DetailsKunaSudharshanNo ratings yet

- Create Act: Corporate Recovery & Tax Incentives For EnterprisesDocument6 pagesCreate Act: Corporate Recovery & Tax Incentives For EnterprisesDanica RamosNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Stiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills and MoreFrom EverandStiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills and MoreRating: 4.5 out of 5 stars4.5/5 (13)

- Tax Savvy for Small Business: A Complete Tax Strategy GuideFrom EverandTax Savvy for Small Business: A Complete Tax Strategy GuideRating: 5 out of 5 stars5/5 (1)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- Freight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesFrom EverandFreight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesRating: 5 out of 5 stars5/5 (1)