You might also like

- Sample Accounting Issues Memo 1 - Gross Vs NetDocument4 pagesSample Accounting Issues Memo 1 - Gross Vs NetAnkit MrCub Patel100% (1)

- Assignment Help Journal Ledger and MyodDocument9 pagesAssignment Help Journal Ledger and MyodrajeshNo ratings yet

- MIDTERM LESSON 1 Accounting EquationDocument2 pagesMIDTERM LESSON 1 Accounting EquationJomar Villena100% (3)

- FAC1502 Assignment 4 2023Document193 pagesFAC1502 Assignment 4 2023Haat My LaterNo ratings yet

- Exercise AC 518 2nd Sem 2016Document2 pagesExercise AC 518 2nd Sem 2016RALLISONNo ratings yet

- 7025afe Coursework 2 Assignment BriefDocument4 pages7025afe Coursework 2 Assignment Briefkartik0% (1)

- 8508Document10 pages8508Danyal ChaudharyNo ratings yet

- Comprehensive Accounting Cycle Review Problem Copy 2Document12 pagesComprehensive Accounting Cycle Review Problem Copy 2api-252183085No ratings yet

- Judge Dredd Rookie S Guide To The Justice DepartmentDocument68 pagesJudge Dredd Rookie S Guide To The Justice Departmentnicolasscribdscribd100% (4)

- F7 Revision Test Section A and B 1Document15 pagesF7 Revision Test Section A and B 1Farman ShaikhNo ratings yet

- Taxation Management and PlanningDocument10 pagesTaxation Management and PlanningJoel EdauNo ratings yet

- Unit 5 - Depreciation - Chat Session 8 (Spring 2020)Document5 pagesUnit 5 - Depreciation - Chat Session 8 (Spring 2020)RealGenius (Carl)No ratings yet

- Value Added Tax Lecture Summary 2020Document72 pagesValue Added Tax Lecture Summary 2020Tatenda RamsNo ratings yet

- Part A Answer ALL Questions.: Confidential AC/OCT 2009/FAR360 2Document4 pagesPart A Answer ALL Questions.: Confidential AC/OCT 2009/FAR360 2Syazliana KasimNo ratings yet

- Unit End Questions For All UnitsDocument6 pagesUnit End Questions For All Unitsvenkata sai gireesh pNo ratings yet

- Acounting For Legal Practice Dec 2016Document5 pagesAcounting For Legal Practice Dec 2016NkululekoNo ratings yet

- 15-Mca-Or-Accounting and Financial ManagementDocument4 pages15-Mca-Or-Accounting and Financial ManagementSRINIVASA RAO GANTANo ratings yet

- 5pm Assignment.Document7 pages5pm Assignment.bophelo jonganiNo ratings yet

- Problem 1 (Cost Classification) : Cost Description Cost ObjectDocument4 pagesProblem 1 (Cost Classification) : Cost Description Cost ObjectMARY JUSTINE PAQUIBOTNo ratings yet

- Malawi Taxation Exam QuestionsDocument15 pagesMalawi Taxation Exam QuestionsCean Mhango100% (1)

- FAC1502 Assignment 4 Semester 2 2023Document192 pagesFAC1502 Assignment 4 Semester 2 2023Haat My LaterNo ratings yet

- Commercial and Industrial ActivitiesDocument15 pagesCommercial and Industrial ActivitiesMR BeastNo ratings yet

- Problems: Problem 1-1Document4 pagesProblems: Problem 1-1Gwen Cornet Pugal Alimo-ot0% (1)

- Financial and Managerial Accounting 11th Edition Warren Solutions ManualDocument10 pagesFinancial and Managerial Accounting 11th Edition Warren Solutions Manualcharlesdrakejth100% (14)

- Impairment of Assets - 1Document18 pagesImpairment of Assets - 1techna8No ratings yet

- HW 1, FIN 604, Sadhana JoshiDocument40 pagesHW 1, FIN 604, Sadhana JoshiSadhana JoshiNo ratings yet

- BITS Pilani MBA Financial Accounting Mid-Semester TestDocument3 pagesBITS Pilani MBA Financial Accounting Mid-Semester Testritesh_aladdinNo ratings yet

- PT 1 Transaction AnalysisDocument3 pagesPT 1 Transaction AnalysisJanela Venice SantosNo ratings yet

- Read The Following Case Situation Carefully and Answer The Questions That FollowDocument7 pagesRead The Following Case Situation Carefully and Answer The Questions That FollowBhuwan PandeyNo ratings yet

- M.B.A (2016 Pattern )Document141 pagesM.B.A (2016 Pattern )Amol AwateNo ratings yet

- Advanced Corporate AccountingDocument6 pagesAdvanced Corporate Accountingamensinkai3133No ratings yet

- Financial analysis and accounting assignmentsDocument2 pagesFinancial analysis and accounting assignmentsHu. A. Hussein'sNo ratings yet

- ilovepdf_mergedDocument21 pagesilovepdf_mergedsakschamcNo ratings yet

- Finance Past PaperDocument6 pagesFinance Past PaperNikki ZhuNo ratings yet

- Final AccountsDocument27 pagesFinal AccountsNafis Siddiqui100% (1)

- Tutorial MGS 405 2022-2023Document6 pagesTutorial MGS 405 2022-2023FOBASSO FRANC JUNIORNo ratings yet

- Degree - Swe - Acc - Resit Session - Marking GuideDocument2 pagesDegree - Swe - Acc - Resit Session - Marking GuideDidier ChautyNo ratings yet

- Full Syllabus Test 1 q1672987668Document11 pagesFull Syllabus Test 1 q1672987668Sachin SHNo ratings yet

- Baw - IDocument5 pagesBaw - Iyoniakia2124No ratings yet

- Commerce Innovations in Accounting Paper 4.5 A: (Accounting and Finance)Document3 pagesCommerce Innovations in Accounting Paper 4.5 A: (Accounting and Finance)Sanaullah M SultanpurNo ratings yet

- FAB Assignment 2020-2021 - UpdatedDocument7 pagesFAB Assignment 2020-2021 - UpdatedMuhammad Hamza AminNo ratings yet

- TMA-02 Fall 2021-2022 Semester IDocument9 pagesTMA-02 Fall 2021-2022 Semester IMahdy TabbaraNo ratings yet

- Rv101 July 2021 Exam QuestionDocument11 pagesRv101 July 2021 Exam Questionandilecebolenkosi4No ratings yet

- IFRS 15 Revenue - Out-Of-Class practice-ENDocument9 pagesIFRS 15 Revenue - Out-Of-Class practice-ENDAN NGUYEN THENo ratings yet

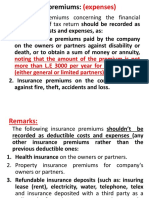

- Insurance Premiums Concerning The Financial (Fiscal) Year of Tax ReturnDocument30 pagesInsurance Premiums Concerning The Financial (Fiscal) Year of Tax ReturnBeshoyIsaacSaadNo ratings yet

- The Feature of P &L AccountDocument14 pagesThe Feature of P &L Accountchand1234567893No ratings yet

- AfB1 Tutorial Questions For Week 3Document3 pagesAfB1 Tutorial Questions For Week 3zhaok0610No ratings yet

- AFA IP.l II QuestionDec 2019Document4 pagesAFA IP.l II QuestionDec 2019HossainNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document19 pagesFundamentals of Accountancy, Business and Management 1Shiellai Mae Polintang0% (1)

- Accounting CycleDocument6 pagesAccounting CycleElla Acosta0% (1)

- Tax Question Bank 2020Document37 pagesTax Question Bank 2020Tawanda Tatenda HerbertNo ratings yet

- Business Transactions of A Service BusinessDocument17 pagesBusiness Transactions of A Service Businessmarissa casareno almuete50% (2)

- CFAB Accounting Chapter 9. Accruals and PrepaymentsDocument33 pagesCFAB Accounting Chapter 9. Accruals and PrepaymentsVânAnh NguyễnNo ratings yet

- Assignment 1Document13 pagesAssignment 1Elin EkströmNo ratings yet

- Universiti Teknologi Mara Final Examination: Confidential AC/APR 2007/FAR100/FAR110/ FAC100Document11 pagesUniversiti Teknologi Mara Final Examination: Confidential AC/APR 2007/FAR100/FAR110/ FAC100kaitokid77No ratings yet

- Financial Management AssignmentDocument53 pagesFinancial Management Assignmentmuleta100% (1)

- Assignment Accounting 2023Document8 pagesAssignment Accounting 2023teddy100% (1)

- Chart of Accounts PolicyDocument13 pagesChart of Accounts PolicyMazhar Ali JoyoNo ratings yet

- Recording Business TransactionsDocument8 pagesRecording Business TransactionsIan BelmonteNo ratings yet

- Management AccountingDocument5 pagesManagement AccountingHamdan SheikhNo ratings yet

- Business Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationFrom EverandBusiness Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationNo ratings yet

- KHFM Hospitality and Facility Management Services Limited: Postal Ballot NoticeDocument2 pagesKHFM Hospitality and Facility Management Services Limited: Postal Ballot NoticeCSNo ratings yet

- Business Communication & Ethics (HS-304) : Maheen Tufail DahrajDocument13 pagesBusiness Communication & Ethics (HS-304) : Maheen Tufail DahrajFaizan ShaikhNo ratings yet

- New Jerusalem, The Bride, The Elect Lady Even ZionDocument2 pagesNew Jerusalem, The Bride, The Elect Lady Even ZionSonofManNo ratings yet

- Sri Lankan Bank Account ComparisonDocument9 pagesSri Lankan Bank Account ComparisonThusitha DalpathaduNo ratings yet

- Court rules man acted in self-defense by resisting land encroachmentDocument2 pagesCourt rules man acted in self-defense by resisting land encroachmentjuan dela cruz100% (2)

- CA Reverses IPO Ruling on McDonald's Opposition to "MacJoyDocument5 pagesCA Reverses IPO Ruling on McDonald's Opposition to "MacJoyMis DeeNo ratings yet

- Electromagnetic Compatibility: Unit-2: CablingDocument27 pagesElectromagnetic Compatibility: Unit-2: CablingShiva Prasad MNo ratings yet

- Overtaking and Passing A Vehicle, and Turning at IntersectionsDocument3 pagesOvertaking and Passing A Vehicle, and Turning at IntersectionsJett Brondial RaymundoNo ratings yet

- Hidayatullah National Law University, Naya Raipur (Chhattisgarh)Document7 pagesHidayatullah National Law University, Naya Raipur (Chhattisgarh)acdeNo ratings yet

- Hudson Law of Finance 2e 2013 Syndicated Loans ch.33Document16 pagesHudson Law of Finance 2e 2013 Syndicated Loans ch.33tracy.jiang0908No ratings yet

- MPPB 2010 1Document60 pagesMPPB 2010 1caaeteNo ratings yet

- Manufacturer's Warranty and Limitation of ClaimsDocument2 pagesManufacturer's Warranty and Limitation of ClaimsBrandon TrocNo ratings yet

- Project Costing & BillingDocument11 pagesProject Costing & BillingHari Prasad AngalakuditiNo ratings yet

- People v. CasidoDocument5 pagesPeople v. CasidojoshmagiNo ratings yet

- Busorg1 DigestDocument5 pagesBusorg1 DigestOwie JoeyNo ratings yet

- Anganwadi Worker Application FormDocument2 pagesAnganwadi Worker Application FormBabina SarminNo ratings yet

- Legend:: Panel Board Diagram A E1Document1 pageLegend:: Panel Board Diagram A E1Anonymous 8Ec6v2No ratings yet

- 214 Temic v. TemicDocument3 pages214 Temic v. TemicRabelais MedinaNo ratings yet

- Hospital Controlled Drug ProceduresDocument3 pagesHospital Controlled Drug ProceduresvaniyaNo ratings yet

- Consumer EducationDocument23 pagesConsumer EducationSid Jain100% (1)

- Report in Philo 1Document2 pagesReport in Philo 1XXXXXNo ratings yet

- Notes For Week 2Document3 pagesNotes For Week 2algokar999No ratings yet

- Angara vs. ComelecDocument3 pagesAngara vs. ComelecJonathan LarozaNo ratings yet

- Cordero Vs CabralDocument11 pagesCordero Vs CabralPatrick RamosNo ratings yet

- Marbella-Bobis V BobisDocument2 pagesMarbella-Bobis V BobisJohn Basil ManuelNo ratings yet

- What Type of Government Does Germany HaveDocument2 pagesWhat Type of Government Does Germany HaveBryan PalmaNo ratings yet

- LufthansaDocument18 pagesLufthansakritiangraNo ratings yet

- Social, Economic and Political Thought Notes Part III (ADAM SMITH, DAVID RICARDO, KARL MARX, MAX WEBER, EMILE DURKHEIM)Document3 pagesSocial, Economic and Political Thought Notes Part III (ADAM SMITH, DAVID RICARDO, KARL MARX, MAX WEBER, EMILE DURKHEIM)simplyhueNo ratings yet