You might also like

- Rate of Interest (% P.a.)Document2 pagesRate of Interest (% P.a.)MeeNo ratings yet

- Deposit Confirmation/Renewal AdviceDocument1 pageDeposit Confirmation/Renewal AdviceTuhin ChakrabortyNo ratings yet

- HDFC YsDocument2 pagesHDFC YsAkshat ShahNo ratings yet

- Deposit Confirmation/Renewal AdviceDocument1 pageDeposit Confirmation/Renewal AdviceShivam SinghNo ratings yet

- Policy Protection PlanDocument36 pagesPolicy Protection Plankrishna_1238No ratings yet

- Ganga Prasad's 8.5% Fixed Deposit Maturing in Sep 2014Document1 pageGanga Prasad's 8.5% Fixed Deposit Maturing in Sep 2014dpk0No ratings yet

- Acknowledgement Slip: Fixed DepositDocument1 pageAcknowledgement Slip: Fixed DepositAneesh BangiaNo ratings yet

- Customer Name: Customer Number Debit Account Number: Scheme: Mode of Operation Maturity InstructionDocument1 pageCustomer Name: Customer Number Debit Account Number: Scheme: Mode of Operation Maturity InstructionSurya Goud0% (1)

- TERM DEPOSIT ADVICEDocument1 pageTERM DEPOSIT ADVICEamirunnbegamNo ratings yet

- Statement Analysis and Investment SummaryDocument3 pagesStatement Analysis and Investment SummaryanuradhaNo ratings yet

- Tax Certificate - of Anjali Lalwani PDFDocument2 pagesTax Certificate - of Anjali Lalwani PDFBasant GakhrejaNo ratings yet

- D JavaApps EMAIL-SERVERv1 (1) .1 Temp 111116095854219Document2 pagesD JavaApps EMAIL-SERVERv1 (1) .1 Temp 111116095854219amardeepjassal85No ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceBalajiNo ratings yet

- Renewal Advice: OfferDocument2 pagesRenewal Advice: Offermaakabhawan26No ratings yet

- Hishu FD PDFDocument1 pageHishu FD PDFFresher NoobNo ratings yet

- Sample Bank StatementDocument9 pagesSample Bank Statementemma adeoyeNo ratings yet

- 4 PDFDocument4 pages4 PDFsatish sharmaNo ratings yet

- Acctstmt HDFC MFDocument1 pageAcctstmt HDFC MFthindmanmohanNo ratings yet

- Sbi AnalyticalDocument21 pagesSbi AnalyticalGurjeevNo ratings yet

- Account activity and balance from 10 Apr to 22 AprDocument2 pagesAccount activity and balance from 10 Apr to 22 AprSRIDHAR allhari0% (1)

- Indian Bank PDFDocument1 pageIndian Bank PDFpiyush jainNo ratings yet

- IDfC FD CertificateDocument3 pagesIDfC FD Certificatenisha bhardwaj100% (1)

- Gmail - PSG PDFDocument1 pageGmail - PSG PDFJehangir Allam100% (2)

- Ca ReportDocument3 pagesCa Reportvijay kumar100% (1)

- 40k Elss Mutual FundDocument1 page40k Elss Mutual FundSachin Khamitkar100% (1)

- 558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaDocument2 pages558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaPankaj GuptaNo ratings yet

- House No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiaDocument1 pageHouse No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiamanishaNo ratings yet

- Lotus savings bank account statement from Feb 2022 to Aug 2022Document13 pagesLotus savings bank account statement from Feb 2022 to Aug 2022Sunkara ThanmayeesaisowmyaNo ratings yet

- Provisional Certificate0230Document1 pageProvisional Certificate0230Neduri KalyanNo ratings yet

- IDBI Bank Statement TitleDocument4 pagesIDBI Bank Statement TitleRaghu Veer100% (1)

- Certificate of Net Wealth and Annual IncomeDocument4 pagesCertificate of Net Wealth and Annual IncomeSimran MehraNo ratings yet

- Bank DetailsDocument11 pagesBank DetailsANANDA MAITYNo ratings yet

- CUBDepositOpeningReceipt 500707170039434Document1 pageCUBDepositOpeningReceipt 500707170039434Ganesh GaneNo ratings yet

- RTPS Nec 2023 3581289Document1 pageRTPS Nec 2023 3581289Mahammad HachanNo ratings yet

- Examination Form Online Payment Receipt: SignatureDocument2 pagesExamination Form Online Payment Receipt: SignaturePranabesh RoyNo ratings yet

- Rent Agreement FormatDocument4 pagesRent Agreement FormatShakti NareshNo ratings yet

- Duplicate: 1 of Page No: File No: / 1 / 2Document2 pagesDuplicate: 1 of Page No: File No: / 1 / 2Anand AdkarNo ratings yet

- Muthoot Finance Loan Sanction LetterDocument30 pagesMuthoot Finance Loan Sanction LetterTHE PHILOSOPHER MADDYNo ratings yet

- Joining LetterDocument5 pagesJoining LetterPawan RawatNo ratings yet

- PDFDocument22 pagesPDFAnonymous ccPU4fNo ratings yet

- Account statement for Siddharth ExportsDocument9 pagesAccount statement for Siddharth Exportssourav84No ratings yet

- Madhu Balance Certificate PDFDocument1 pageMadhu Balance Certificate PDFpavan kumar teppalaNo ratings yet

- Gorakhnath Construction Company: SALARY SLIP (01-Oct-2019)Document2 pagesGorakhnath Construction Company: SALARY SLIP (01-Oct-2019)pardeep sanwalNo ratings yet

- Loan AgreementDocument20 pagesLoan AgreementRANJIT BISWAL (Ranjit)No ratings yet

- E-Fixed Deposit Account ReceiptDocument1 pageE-Fixed Deposit Account ReceiptEsther DregoNo ratings yet

- Loan StatementDocument3 pagesLoan StatementNityananda SahuNo ratings yet

- HDFC Bank StatementDocument4 pagesHDFC Bank StatementAsmin Sultana AhmedNo ratings yet

- Statement of Account: L246G SBI Gold Fund - Regular Plan - Growth NAV As On 14/10/2015: 8.8804Document4 pagesStatement of Account: L246G SBI Gold Fund - Regular Plan - Growth NAV As On 14/10/2015: 8.8804hari sharmaNo ratings yet

- Tax Certificate - 008927742 - 131310Document2 pagesTax Certificate - 008927742 - 131310Vignesh MahadevanNo ratings yet

- Zerodha Broking Limited: Transaction With Holding StatementDocument1 pageZerodha Broking Limited: Transaction With Holding StatementChandradeep Reddy TeegalaNo ratings yet

- FormDocument2 pagesFormBhargav VekariaNo ratings yet

- B 88 Tulsi Bunglows Radhanpur Road Mahesana Mahesana - 384002 Gujarat, IndiaDocument2 pagesB 88 Tulsi Bunglows Radhanpur Road Mahesana Mahesana - 384002 Gujarat, IndiaJigs PatelNo ratings yet

- Renewal Premium Receipt: Policy Number Date & Time AmountDocument1 pageRenewal Premium Receipt: Policy Number Date & Time AmountGokuNo ratings yet

- Policy Doc PDFDocument4 pagesPolicy Doc PDFGajen SinghNo ratings yet

- Investor Service Centre Contact DetailsDocument3 pagesInvestor Service Centre Contact Detailsmaakabhawan26No ratings yet

- Account Statement: Non-TransferableDocument2 pagesAccount Statement: Non-Transferablemaakabhawan26No ratings yet

- Eby Net Worth PDFDocument2 pagesEby Net Worth PDFkarthikram karthiNo ratings yet

- Sbi Fix Deposit Slip PDFDocument1 pageSbi Fix Deposit Slip PDFAbdullah siddikiNo ratings yet

- Acctstmt DDocument4 pagesAcctstmt Dmaakabhawan26No ratings yet

- Deposit Confirmation/Renewal AdviceDocument2 pagesDeposit Confirmation/Renewal AdvicethisissandeepsudNo ratings yet

- HP2122FOREX664Document1 pageHP2122FOREX664Kunda MalleshNo ratings yet

- HP2122FOREX664Document1 pageHP2122FOREX664Kunda MalleshNo ratings yet

- Rent ReceiptsDocument4 pagesRent ReceiptsKunda MalleshNo ratings yet

- Rent ReceiptDocument3 pagesRent ReceiptKunda MalleshNo ratings yet

- J C Investments Profit & Loss A/c Apr 2021-Mar 2022Document1 pageJ C Investments Profit & Loss A/c Apr 2021-Mar 2022Kunda MalleshNo ratings yet

- Hporg20222161339456928096200hp 2022121506511671087082Document2 pagesHporg20222161339456928096200hp 2022121506511671087082Kunda MalleshNo ratings yet

- FSI Sep2018Document19 pagesFSI Sep2018Kunda MalleshNo ratings yet

- Hporg20207241550211972528985hp 2022121613471671198437Document2 pagesHporg20207241550211972528985hp 2022121613471671198437Kunda MalleshNo ratings yet

- Teamviewer 1988209925Document1 pageTeamviewer 1988209925Kunda MalleshNo ratings yet

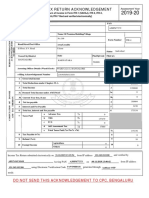

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruKunda MalleshNo ratings yet

- Crm Services India Payslip July 2022Document1 pageCrm Services India Payslip July 2022Parveen SainiNo ratings yet

- What Is A Profit and Loss (P&L) Statement - InvestopediaDocument16 pagesWhat Is A Profit and Loss (P&L) Statement - InvestopediaFrancisco Del PuertoNo ratings yet

- Lesson 7 Complementary Investment Studies and Break Even AnalysisDocument25 pagesLesson 7 Complementary Investment Studies and Break Even Analysisfathima camangianNo ratings yet

- Terrm Project On Hindustan UnileverDocument28 pagesTerrm Project On Hindustan UnileverAmar Stunts ManNo ratings yet

- Complete Financial Statements With SCF Direcdt MethodDocument23 pagesComplete Financial Statements With SCF Direcdt MethodJuja FlorentinoNo ratings yet

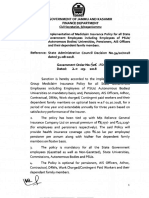

- GO 406-FD of 2018 Dated 20.09.2018 Mediclaim InsuranceDocument6 pagesGO 406-FD of 2018 Dated 20.09.2018 Mediclaim InsuranceRAGHVENDRA PRATAP SINGHNo ratings yet

- Chart of AccountsDocument3 pagesChart of AccountsJaceNo ratings yet

- Reading Test Part 4Document2 pagesReading Test Part 4lorenaNo ratings yet

- Working Lecture 7Document17 pagesWorking Lecture 7Sara KarenNo ratings yet

- AR 19 Mar 2013Document346 pagesAR 19 Mar 2013dewi wahyuNo ratings yet

- Finding Operating and Free Cash FlowsDocument5 pagesFinding Operating and Free Cash FlowsM.TalhaNo ratings yet

- Absorption Costing Vs Variable CostingDocument2 pagesAbsorption Costing Vs Variable Costingneway gobachew100% (1)

- Capital Budgeting: Dr. Sadhna BagchiDocument28 pagesCapital Budgeting: Dr. Sadhna Bagchiarcha agrawalNo ratings yet

- ICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andDocument6 pagesICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andArpit GuptaNo ratings yet

- Guide to Registering Your Business with the BIRDocument2 pagesGuide to Registering Your Business with the BIRPaulNo ratings yet

- Manufacturing Accounts PowerpointDocument12 pagesManufacturing Accounts PowerpointRaynardo KnightNo ratings yet

- Pnoc Renewables Corporation Notes To Financial Statements: A. Geothermal ProjectsDocument23 pagesPnoc Renewables Corporation Notes To Financial Statements: A. Geothermal ProjectsLolita CalaycayNo ratings yet

- IBM Annual Report 2014Document17 pagesIBM Annual Report 2014Max meNo ratings yet

- Manthan Aug NewDocument1 pageManthan Aug NewManthan ShahNo ratings yet

- OPTION TRADING STRATEGIES For Volatile Markets: Learn From The Traders Not TrainersDocument4 pagesOPTION TRADING STRATEGIES For Volatile Markets: Learn From The Traders Not Trainersvivekghadi0% (1)

- Football Field MYOR-2Document27 pagesFootball Field MYOR-2Nusan TravellerNo ratings yet

- Basic BookkeepingDocument80 pagesBasic BookkeepingCharity CotejoNo ratings yet

- Afar 2 Module CH 9 & 10Document16 pagesAfar 2 Module CH 9 & 10Elaiza LozanoNo ratings yet

- Accounts DecemberDocument28 pagesAccounts DecemberSudhan NairNo ratings yet

- MBA-513-Educational ToyDocument18 pagesMBA-513-Educational ToyRajuNo ratings yet

- Demonetization Essay PDF - Essay On Demonetization PDF IndiaDocument4 pagesDemonetization Essay PDF - Essay On Demonetization PDF IndiaKr Ish Na0% (1)

- 3 Solution Q.5Document4 pages3 Solution Q.5Aayush AgrawalNo ratings yet

- IRS EIN Notice BreakdownDocument2 pagesIRS EIN Notice BreakdownDoo Soo KimNo ratings yet

- ACC501 01 FINAL Fall20082-1Document15 pagesACC501 01 FINAL Fall20082-1Fun NNo ratings yet

- BCG Matrix Analysis of Chanakya National Law University ProjectDocument31 pagesBCG Matrix Analysis of Chanakya National Law University ProjectHarshit GuptaNo ratings yet