You might also like

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- CMR (Money Market Instruments) 7 SemDocument12 pagesCMR (Money Market Instruments) 7 SemRicha NandyNo ratings yet

- Treasury ManagementDocument30 pagesTreasury ManagementAMAL CHRISTY GEORGENo ratings yet

- Macroeconomic (Saving and Investment)Document110 pagesMacroeconomic (Saving and Investment)Sheillie KirklandNo ratings yet

- Welcome To Our Presentation: Topic: Money Market in Viet NamDocument27 pagesWelcome To Our Presentation: Topic: Money Market in Viet NamThu ThuNo ratings yet

- Money MarketDocument8 pagesMoney MarketsalvandorNo ratings yet

- Mechanics of Futures and The Hedging Strategies Chapter 2&3: Geng NiuDocument71 pagesMechanics of Futures and The Hedging Strategies Chapter 2&3: Geng NiuegaNo ratings yet

- 11 CHPTDocument6 pages11 CHPTI IvaNo ratings yet

- Money Markets: For A Period Longer Than 1 Year, in Form of Both Debt & Equity)Document5 pagesMoney Markets: For A Period Longer Than 1 Year, in Form of Both Debt & Equity)api-19893912No ratings yet

- 16 Money Market InstrumentsDocument2 pages16 Money Market InstrumentsrickyakiNo ratings yet

- IFS BOOK MEPL Sem 3 CUDocument67 pagesIFS BOOK MEPL Sem 3 CUkohinoor5225No ratings yet

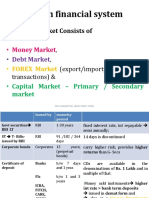

- Indian Financial System: Financial Market Consists ofDocument67 pagesIndian Financial System: Financial Market Consists ofTHILAGALAKSHMI M DNo ratings yet

- Vietnam Money Market: Íinstruments, Participants and Trading ProcessDocument34 pagesVietnam Money Market: Íinstruments, Participants and Trading ProcessNguyen Thi Phuong DungNo ratings yet

- PDF DocumentDocument21 pagesPDF DocumentJenny BalangueNo ratings yet

- Topic - Money Market Group Members: Kunal Gharat Deepak Gohil Pradeep Gore Meenakshi Jadhav Sandeep JaigudeDocument30 pagesTopic - Money Market Group Members: Kunal Gharat Deepak Gohil Pradeep Gore Meenakshi Jadhav Sandeep Jaigudek_vikNo ratings yet

- Security - Markets IMP H.LDocument43 pagesSecurity - Markets IMP H.Lparna dhandharaNo ratings yet

- Session 3 Uses of Bank FundsDocument22 pagesSession 3 Uses of Bank FundsPalash MondalNo ratings yet

- Financial Institutions and Markets 7Th Edition Hunt Solutions Manual Full Chapter PDFDocument31 pagesFinancial Institutions and Markets 7Th Edition Hunt Solutions Manual Full Chapter PDFhieudermotjm7w100% (11)

- Moneymarket 091101023117 Phpapp01Document27 pagesMoneymarket 091101023117 Phpapp01sweetu_bharatiNo ratings yet

- My Notes (Eurodollar Master Notes From The Eurodollar Futures Book, by BurghardtDocument59 pagesMy Notes (Eurodollar Master Notes From The Eurodollar Futures Book, by Burghardtlaozi222No ratings yet

- Types of Accounts, Bank Guarantee, LC, Line of CreditDocument44 pagesTypes of Accounts, Bank Guarantee, LC, Line of Creditkaren sunilNo ratings yet

- Unit 4 - Govt. BondsDocument14 pagesUnit 4 - Govt. Bondsshubh duttNo ratings yet

- Business Financial EnvironmentDocument198 pagesBusiness Financial EnvironmentAmitava MukherjeeNo ratings yet

- Bills Discounting, Factoring & ForfaitingDocument23 pagesBills Discounting, Factoring & ForfaitingVineet HaritNo ratings yet

- Lecture 02 PDFDocument1 pageLecture 02 PDFBharathNo ratings yet

- Money Market in IndiaDocument41 pagesMoney Market in IndiaTriumph collegeNo ratings yet

- Letter of CreditDocument14 pagesLetter of Creditswapnilnaik2001100% (1)

- DRIVATIVES Options Call & Put KKDocument134 pagesDRIVATIVES Options Call & Put KKAjay Raj ShuklaNo ratings yet

- Debt MarketDocument25 pagesDebt MarketSuraj DasNo ratings yet

- Money Market and Types of Money Market InstrumentsDocument6 pagesMoney Market and Types of Money Market InstrumentsWasimAkramNo ratings yet

- Module1-Investments & Risk & DerivativesDocument169 pagesModule1-Investments & Risk & DerivativesLMT indiaNo ratings yet

- Topic 2 Securities Markets and TransactionsDocument63 pagesTopic 2 Securities Markets and Transactionsqian liuNo ratings yet

- T10 Treasury Operations IDocument2 pagesT10 Treasury Operations Ikhongst-wb22No ratings yet

- BondmarketpptDocument28 pagesBondmarketpptMia LeslieNo ratings yet

- Unit 3 (3RD)Document42 pagesUnit 3 (3RD)Sonam ShahNo ratings yet

- Ch03 Money MarketDocument8 pagesCh03 Money MarketPaw VerdilloNo ratings yet

- 5 - Investment ManagementDocument14 pages5 - Investment ManagementTiến ĐứcNo ratings yet

- Securitizationfinal 091012114554 Phpapp02Document42 pagesSecuritizationfinal 091012114554 Phpapp02Anonymous H0SJWZE8No ratings yet

- STLT Finance 2 - Money & Bond MarketsDocument16 pagesSTLT Finance 2 - Money & Bond MarketsHanae ElNo ratings yet

- FMAI - Ch02 - Money MarketDocument81 pagesFMAI - Ch02 - Money Marketngoc duongNo ratings yet

- Securities Market: Dr. Rana Singh 9811828987Document52 pagesSecurities Market: Dr. Rana Singh 9811828987Abebe AdmasuNo ratings yet

- Money MarktDocument3 pagesMoney MarkttinkashNo ratings yet

- Investment Analysis & Portfolio Management: Unit 4: Introduction To Money MarketDocument16 pagesInvestment Analysis & Portfolio Management: Unit 4: Introduction To Money MarketSujeet KawdeNo ratings yet

- Lecture 02 PDFDocument1 pageLecture 02 PDFOuadia ElzNo ratings yet

- Money Market & Its InstrumentsDocument16 pagesMoney Market & Its InstrumentsmanoranjanpatraNo ratings yet

- Chapter 2 MONEY MARKETDocument14 pagesChapter 2 MONEY MARKETNur Dina AbsbNo ratings yet

- The Indian Money Market: Prime AcademyDocument5 pagesThe Indian Money Market: Prime AcademyHardik KharaNo ratings yet

- Money Market Accounts. Borrowers May Use Money From These Accounts To Invest inDocument13 pagesMoney Market Accounts. Borrowers May Use Money From These Accounts To Invest inОля ОляфкаNo ratings yet

- Chapter 13b Investing Surplus FundDocument28 pagesChapter 13b Investing Surplus FundIvy CheekNo ratings yet

- Financial Markets and InstitutionsDocument14 pagesFinancial Markets and InstitutionsAlayne100% (1)

- Debt Instruments Bank LoansDocument42 pagesDebt Instruments Bank Loansprakhar singh100% (4)

- Individual Assignment Fin358 - Putri Laila (2018211518) Ba1195dDocument10 pagesIndividual Assignment Fin358 - Putri Laila (2018211518) Ba1195dPutri LailaNo ratings yet

- Money Market vs. Capital Market: What Is Money Markets?Document4 pagesMoney Market vs. Capital Market: What Is Money Markets?Ash imoNo ratings yet

- FM, Class 3Document23 pagesFM, Class 3NITYA NAYARNo ratings yet

- Call Money PresentationDocument35 pagesCall Money PresentationRANJIT RAVINDRANNo ratings yet

- Essential Points To Solve Case StudiesDocument6 pagesEssential Points To Solve Case StudiesAaryan KarthikeyNo ratings yet

- Trends of C.P. MarketDocument14 pagesTrends of C.P. Marketmayankpoddar009No ratings yet

- Tarheel Consultancy Services: BangaloreDocument170 pagesTarheel Consultancy Services: BangaloreSumit SinghNo ratings yet

- Debt Markets: Government Bonds T-Bills State Government Bonds Call Money Markets Corporate DebtDocument33 pagesDebt Markets: Government Bonds T-Bills State Government Bonds Call Money Markets Corporate DebtSwati JainNo ratings yet

- Cfas Pre FinalDocument10 pagesCfas Pre Finalreagan blaireNo ratings yet

- Swapd and FRAsDocument53 pagesSwapd and FRAsSCCEGNo ratings yet

- Structured Products 2Document41 pagesStructured Products 2SCCEGNo ratings yet

- Structured Products 1Document23 pagesStructured Products 1SCCEGNo ratings yet

- Interest Rate Futures and OptionsDocument48 pagesInterest Rate Futures and OptionsSCCEGNo ratings yet

- ConvertiblesDocument28 pagesConvertiblesSCCEGNo ratings yet

- Thebook v11Document111 pagesThebook v11SCCEGNo ratings yet

- Basic Fixed Income MathematicsDocument44 pagesBasic Fixed Income MathematicsSCCEGNo ratings yet

- Thebook v33Document120 pagesThebook v33SCCEG0% (1)

- Thebook v21Document225 pagesThebook v21SCCEGNo ratings yet

- Thebook v42Document373 pagesThebook v42SCCEGNo ratings yet

- 11th STD Economics English MediumDocument288 pages11th STD Economics English MediumSCCEGNo ratings yet

- DataCamp Curriculum Cheat SheetDocument11 pagesDataCamp Curriculum Cheat SheetSCCEGNo ratings yet

- SWOT Analysis Slides Powerpoint TemplateDocument20 pagesSWOT Analysis Slides Powerpoint TemplateiedaNo ratings yet

- IEOR E4718 Spring2015 SyllabusDocument10 pagesIEOR E4718 Spring2015 Syllabuscef4No ratings yet

- PACC Offshore Services IPO ProspectusDocument516 pagesPACC Offshore Services IPO ProspectusJame ColesNo ratings yet

- Strategic Mgmt-II QuestionsDocument14 pagesStrategic Mgmt-II Questionsbutwalservice75% (4)

- A Comparative Analysis of Pricing Strategies On SalesDocument11 pagesA Comparative Analysis of Pricing Strategies On SalesJrNo ratings yet

- Chapter 25: Step by Step Murabaha Financing: Bank ClientDocument3 pagesChapter 25: Step by Step Murabaha Financing: Bank ClientAlton JurahNo ratings yet

- Zero To Hero Program DetailsDocument28 pagesZero To Hero Program DetailsMohammad FarooqNo ratings yet

- Future GroupDocument7 pagesFuture GroupAbhay Pratap SinghNo ratings yet

- Khaled Mahmud: Myopia & MalpracticeDocument30 pagesKhaled Mahmud: Myopia & MalpracticeM. G. MostofaNo ratings yet

- Uber Service AuditDocument12 pagesUber Service AuditAdeelNo ratings yet

- CHAPTER 10 - Inventory ManagementDocument15 pagesCHAPTER 10 - Inventory ManagementAaminah BeathNo ratings yet

- Order To Cash: Current Process of Widget IncDocument13 pagesOrder To Cash: Current Process of Widget IncGowri J BabuNo ratings yet

- Salesforce 50 Pro Sales Tips For 2020Document59 pagesSalesforce 50 Pro Sales Tips For 2020Marc MetzNo ratings yet

- Minggu 8 - MonopoliDocument80 pagesMinggu 8 - MonopoliDevina GabriellaNo ratings yet

- Samsung GalaxyDocument1 pageSamsung Galaxykumar gaurav100% (2)

- 12.1 International Trade and Protectionism Answer KeyDocument6 pages12.1 International Trade and Protectionism Answer KeyPhat M.No ratings yet

- Bond Duration - Dynamic ChartDocument3 pagesBond Duration - Dynamic Chartapi-3763138No ratings yet

- Warrant Buffet: Investment StrategyDocument16 pagesWarrant Buffet: Investment StrategyYassir SlaouiNo ratings yet

- 2010 Macro FRQDocument8 pages2010 Macro FRQKripansh GroverNo ratings yet

- Abba Ali Habib EquityDocument2 pagesAbba Ali Habib Equityali ahmadNo ratings yet

- Indian Institute of Management, Sambalpur 2022-2023: Written Analysis and Communication ProjectDocument15 pagesIndian Institute of Management, Sambalpur 2022-2023: Written Analysis and Communication ProjectGANESH BALAJI.N 1715111100% (1)

- PSG - Tutorial 10 - Point and Figure ChartsDocument19 pagesPSG - Tutorial 10 - Point and Figure ChartsBikash Bhanu RoyNo ratings yet

- NinftyDocument16 pagesNinftysonalliNo ratings yet

- AssignmentDocument11 pagesAssignmentMuhammad MuazzamNo ratings yet

- About One Drop PerfumesDocument2 pagesAbout One Drop PerfumesBiey RabiatulNo ratings yet

- Slot Trading: The New Proposal of The European CommissionDocument4 pagesSlot Trading: The New Proposal of The European CommissionGiulia Mauri, Partner - KadrantNo ratings yet

- Business ValuationDocument13 pagesBusiness ValuationFedryan Adhie S100% (1)

- Factors Affecting Promotion Mix - Top 10 Factors Affecting Promotion MixDocument49 pagesFactors Affecting Promotion Mix - Top 10 Factors Affecting Promotion MixJoyjit SanyalNo ratings yet

- Auto Trend ForecasterDocument15 pagesAuto Trend ForecasterherbakNo ratings yet

- E Commerce Application Based On Farming ProductsDocument4 pagesE Commerce Application Based On Farming ProductsEditor IJTSRDNo ratings yet