You might also like

- Guidebook for Demand Aggregation: Way Forward for Rooftop Solar in IndiaFrom EverandGuidebook for Demand Aggregation: Way Forward for Rooftop Solar in IndiaNo ratings yet

- Show Cause NoticeDocument8 pagesShow Cause NoticeinfoNo ratings yet

- B WDocument7 pagesB Washish malhotraNo ratings yet

- Sri Shabari AisDocument12 pagesSri Shabari AisKATTA VENKATA KRISHNAIAHNo ratings yet

- Santosh AisDocument1 pageSantosh Aisjaigovind boobNo ratings yet

- Ec Electrodes Ipin202207140011Document5 pagesEc Electrodes Ipin202207140011Abhinav KalitaNo ratings yet

- AAACK7632B-2013-14 Form 26AASDocument7 pagesAAACK7632B-2013-14 Form 26AASRama Prasad PadhyNo ratings yet

- Ahwpl0214g 2023Document5 pagesAhwpl0214g 2023cagopalofficebackupNo ratings yet

- GeM Bidding 5499500Document10 pagesGeM Bidding 5499500Rajib BasakNo ratings yet

- Amypp6165b 2023Document4 pagesAmypp6165b 2023sandeep kumarNo ratings yet

- Agnpc9838k 2023Document4 pagesAgnpc9838k 2023Warrior GamerNo ratings yet

- Cospk1931c 2023Document4 pagesCospk1931c 2023Komal KapseNo ratings yet

- Gem Shoes ErDocument7 pagesGem Shoes ErBhumi ShahNo ratings yet

- Ms Color N Style PVT LTD Lf-22!23!342Document3 pagesMs Color N Style PVT LTD Lf-22!23!342krishnaNo ratings yet

- GeM Bidding 3302800Document10 pagesGeM Bidding 3302800Rahul RawatNo ratings yet

- Hyderabad Report March-2022-17052022Document1 pageHyderabad Report March-2022-17052022Yakshit JainNo ratings yet

- Account Portfolio Summary From 01-APR-2016 To 31-MAR-2017: Page 1 of 3 3158700 / 24Document9 pagesAccount Portfolio Summary From 01-APR-2016 To 31-MAR-2017: Page 1 of 3 3158700 / 24Bimal Kumar MohataNo ratings yet

- PT Geoservices LTD.: FROM 01/08/2022 TO 31/08/2022Document6 pagesPT Geoservices LTD.: FROM 01/08/2022 TO 31/08/2022heruNo ratings yet

- 15-30 DaysDocument3 pages15-30 Daysdivya padmanabanNo ratings yet

- Summary of Note On Payments: Greenko DNDDocument9 pagesSummary of Note On Payments: Greenko DNDAishwarya VarmaNo ratings yet

- 2.HSE Report PPEM Apr 2023Document8 pages2.HSE Report PPEM Apr 2023Khaty JahNo ratings yet

- GeM Bidding 4493242Document7 pagesGeM Bidding 4493242sisstudioblrNo ratings yet

- SURYA Gujarat - Unified Single Window Rooftop PV Portal - Web 1Document1 pageSURYA Gujarat - Unified Single Window Rooftop PV Portal - Web 1Anonymous HvihZxGNNo ratings yet

- Old PO-80211001100555Document3 pagesOld PO-80211001100555ManojNo ratings yet

- Kt&Gi-hq - BMM - 003-02-22 - PK Trial Consumer - Bana Pop Expand Amo - Rp. 46813000 - ApprovedDocument9 pagesKt&Gi-hq - BMM - 003-02-22 - PK Trial Consumer - Bana Pop Expand Amo - Rp. 46813000 - ApprovedkppamojakartawestNo ratings yet

- Aaecc2134l 2023 PDFDocument4 pagesAaecc2134l 2023 PDFVineet KhuranaNo ratings yet

- Copy2 of PO YTL - BACKUPDocument1 pageCopy2 of PO YTL - BACKUPNur Azlina NazriNo ratings yet

- Refund Rebate Hydrb Feb 22Document1 pageRefund Rebate Hydrb Feb 22Yakshit JainNo ratings yet

- Form 26asDocument6 pagesForm 26asSubramanyam JonnaNo ratings yet

- Site QuantitiesDocument211 pagesSite Quantitiesvaibhav sawantNo ratings yet

- GeM Bidding 4553416Document6 pagesGeM Bidding 4553416Rising Trans Infra SolutionsNo ratings yet

- For The Worthy Regional Tax Office Islamabad: Chief Commissioner - IrDocument13 pagesFor The Worthy Regional Tax Office Islamabad: Chief Commissioner - IrUsman Shaukat KhanNo ratings yet

- Statement of Account - 21 - 38 - 42Document3 pagesStatement of Account - 21 - 38 - 42Srinadh JettiNo ratings yet

- Circular 14062023-Vivad Se Vishwas-1Document4 pagesCircular 14062023-Vivad Se Vishwas-1Priya SinghNo ratings yet

- E-Way Bill: Government of IndiaDocument1 pageE-Way Bill: Government of IndiaVIVEK N KHAKHARANo ratings yet

- Bid Mega 1Document55 pagesBid Mega 1Sumit GuptaNo ratings yet

- Form Unblock Customer 01 - PT. RJS - SignedDocument1 pageForm Unblock Customer 01 - PT. RJS - SignedArman amirNo ratings yet

- GeM Bidding 3387647Document5 pagesGeM Bidding 3387647Sonu KushwahaNo ratings yet

- GeM Bidding 3485930Document23 pagesGeM Bidding 3485930MDL COMMNo ratings yet

- Account Statement From 21 Jul 2022 To 31 Aug 2022Document3 pagesAccount Statement From 21 Jul 2022 To 31 Aug 2022chinmoy patraNo ratings yet

- Abbreviations: IFB . Invitation For BidsDocument2 pagesAbbreviations: IFB . Invitation For BidsRam NepaliNo ratings yet

- Purchase OrderDocument2 pagesPurchase OrderAnand VermaNo ratings yet

- Annexure Viii Neon Cable - 26!04!2021Document12 pagesAnnexure Viii Neon Cable - 26!04!2021group3 cgstauditNo ratings yet

- Loa JP EpcDocument2 pagesLoa JP EpcIES-GATEWizNo ratings yet

- DRM/W/JHS Acting For and On Behalf of The President of India Invites E-Tenders Against Tender No JHS-ENGG-HQ-2022-17 ClosingDocument8 pagesDRM/W/JHS Acting For and On Behalf of The President of India Invites E-Tenders Against Tender No JHS-ENGG-HQ-2022-17 ClosingM D SrivastavaNo ratings yet

- Ckepk7343g 2023Document4 pagesCkepk7343g 2023Shashwat SumanNo ratings yet

- Name Joko Warsuyo Department 3124kjiuaf No Date Activity No. Project NoteDocument2 pagesName Joko Warsuyo Department 3124kjiuaf No Date Activity No. Project NotewretchNo ratings yet

- Document 1Document2 pagesDocument 1gstceraslmNo ratings yet

- BCI20200813161126 - C2 TMD Trip UnitDocument4 pagesBCI20200813161126 - C2 TMD Trip Unitranj kNo ratings yet

- IDFCFIRSTBankstatement 10027354401 154032854Document6 pagesIDFCFIRSTBankstatement 10027354401 154032854SAGAR YADAVNo ratings yet

- Hyder 181122Document1 pageHyder 181122Yakshit JainNo ratings yet

- 290 (80-Stn Smiley Ball)Document2 pages290 (80-Stn Smiley Ball)Sudhir GuptaNo ratings yet

- Hyderabad 22122022Document1 pageHyderabad 22122022Yakshit JainNo ratings yet

- Lana Technologies Private Limited: Particulars Credit DebitDocument1 pageLana Technologies Private Limited: Particulars Credit DebitVsa VasuNo ratings yet

- GeM Bidding 5691429Document7 pagesGeM Bidding 5691429DHEERAJ JAINNo ratings yet

- Hamara Punmp Q4 Fy 2021-2022Document3 pagesHamara Punmp Q4 Fy 2021-2022Advocate SkitaxNo ratings yet

- It I Ro Ahd 16052022Document114 pagesIt I Ro Ahd 16052022harshNo ratings yet

- Aino Communique 108th EditionDocument12 pagesAino Communique 108th EditionSwathi JainNo ratings yet

- GeM Bidding 3458186Document4 pagesGeM Bidding 3458186MANISH KAPADIYANo ratings yet

- E20 CVL Work OrderDocument151 pagesE20 CVL Work OrderEr. TK SahuNo ratings yet

- Notice of Twenty Ninth Annual General MeetingDocument8 pagesNotice of Twenty Ninth Annual General MeetingAakash SinglaNo ratings yet

- 08 Poonam ItineraryDocument2 pages08 Poonam ItineraryAakash SinglaNo ratings yet

- Dec'22 Electricity BillDocument1 pageDec'22 Electricity BillAakash SinglaNo ratings yet

- Agm NoticeDocument4 pagesAgm NoticeAakash SinglaNo ratings yet

- Statement DEC2022 265757521Document6 pagesStatement DEC2022 265757521Ranjit LengureNo ratings yet

- User Id 012439461813 - DSL Telephonenumber 01244823150Document6 pagesUser Id 012439461813 - DSL Telephonenumber 01244823150NAVEEN SLNo ratings yet

- Benefits of Income TaxDocument2 pagesBenefits of Income TaxHemant PaulNo ratings yet

- DeductionsDocument10 pagesDeductionsceline marasiganNo ratings yet

- Online Banking DownloadDocument4 pagesOnline Banking DownloadANDREW STRUGNELLNo ratings yet

- Encasa BrochureDocument12 pagesEncasa Brochuremanoj_dalalNo ratings yet

- Interim Statement 10-Mar-2023 12-25-49Document2 pagesInterim Statement 10-Mar-2023 12-25-49zani arslanNo ratings yet

- HelloMoney FAQsDocument3 pagesHelloMoney FAQsGrendelle BasaNo ratings yet

- Module2 AE26 ITDocument7 pagesModule2 AE26 ITJemalyn PiliNo ratings yet

- QQQQQQQQQQQQQQQQQQDocument2 pagesQQQQQQQQQQQQQQQQQQZakir Brama LombokNo ratings yet

- No Name T1 2022Document42 pagesNo Name T1 2022Indo -CanadianNo ratings yet

- Member ApplyDocument2 pagesMember ApplyIvo SapplasNo ratings yet

- Prelim TaxDocument5 pagesPrelim TaxDonna Zandueta-TumalaNo ratings yet

- Make-Up & Beauty Salon: Guruji EnterprisesDocument1 pageMake-Up & Beauty Salon: Guruji EnterprisesAMITNo ratings yet

- Possible Q&ADocument22 pagesPossible Q&AmarkespinoNo ratings yet

- 01.04.2022 To 20.02.2023Document22 pages01.04.2022 To 20.02.2023PrashantNo ratings yet

- SSHC PaystubDocument1 pageSSHC Paystubnsampson739No ratings yet

- Your BillDocument4 pagesYour BillPruthviraj JuniNo ratings yet

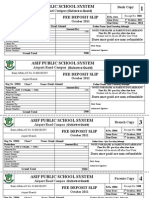

- Asif Public School System: Fee Deposit SlipDocument1 pageAsif Public School System: Fee Deposit SlipIrfan YousafNo ratings yet

- Notification 11 2021Document2 pagesNotification 11 2021sudhagar palaniNo ratings yet

- Foreign Currency Accounts RFCD, ERQ, NFCD, NITA, FCDocument4 pagesForeign Currency Accounts RFCD, ERQ, NFCD, NITA, FCOrko Abir100% (1)

- Lecture Notes Corporate Income TaxDocument25 pagesLecture Notes Corporate Income TaxAU SLNo ratings yet

- Account Statement 280322 270622Document43 pagesAccount Statement 280322 270622Maha RajaNo ratings yet

- EBTax UAT Test Script ARDocument2 pagesEBTax UAT Test Script ARchirag0% (1)

- Screen Noir 48M Boa 13.12.2021Document1 pageScreen Noir 48M Boa 13.12.2021EllerNo ratings yet

- PAYSLIPDocument11 pagesPAYSLIPSaran ManiNo ratings yet

- User Manual: Intellect Core Banking System (CBS)Document50 pagesUser Manual: Intellect Core Banking System (CBS)tempo100% (5)

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Document6 pagesBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)شمس الدين إسماعيلNo ratings yet

- Buy Verified Stripe AccountDocument12 pagesBuy Verified Stripe Accountrohanpur3899No ratings yet

- F 5452Document4 pagesF 5452IRSNo ratings yet