You might also like

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanFrom EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNo ratings yet

- 3 DR KBL MathurDocument31 pages3 DR KBL MathurAkhilesh MishraNo ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

- The Budget Process by Group 3Document15 pagesThe Budget Process by Group 3Anne MalongoNo ratings yet

- Term Paper AmidaDocument10 pagesTerm Paper AmidaPhelixNo ratings yet

- Budget FormulationDocument54 pagesBudget FormulationShravani PalandeNo ratings yet

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document13 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033Angelito Mamersonal100% (1)

- Preparation and Enactment of Budget in IndianDocument9 pagesPreparation and Enactment of Budget in Indianmrityunjaybayanguist45No ratings yet

- Makerere University: Business SchoolDocument4 pagesMakerere University: Business SchoolHSFXHFHXNo ratings yet

- SEC Assignment Final Semester IIIDocument5 pagesSEC Assignment Final Semester IIITushi TalwarNo ratings yet

- 40ekl 15099 BSG Dr. Peter MangiDocument16 pages40ekl 15099 BSG Dr. Peter MangiAllan JoelNo ratings yet

- The Two Sides of The BudgetDocument8 pagesThe Two Sides of The BudgetritusahrawatNo ratings yet

- The Budget ProcessDocument31 pagesThe Budget ProcessrizzaNo ratings yet

- MPA 261 The Budget PhasesDocument42 pagesMPA 261 The Budget PhasesRea LahoylahoyNo ratings yet

- Week 12 Reading MaterialDocument18 pagesWeek 12 Reading MaterialAfrasiyab ., BS Commerce Hons Student, UoPNo ratings yet

- Bugets-Basics & Terminologies-Ankur SachanDocument8 pagesBugets-Basics & Terminologies-Ankur Sachanamarsinha1987No ratings yet

- Budget Formulation ProcessDocument15 pagesBudget Formulation ProcessAnkit SharmaNo ratings yet

- The Key Elements of Union Budget Document and Its Formation ProcessesDocument9 pagesThe Key Elements of Union Budget Document and Its Formation Processesposhita8singlaNo ratings yet

- The Various Objectives of Government Budget Are: 1. Reallocation of ResourcesDocument23 pagesThe Various Objectives of Government Budget Are: 1. Reallocation of ResourcesSantosh ChhetriNo ratings yet

- CH 08 Budget System and Cost Benefit Anlysis (Autosaved)Document36 pagesCH 08 Budget System and Cost Benefit Anlysis (Autosaved)Hossain UzzalNo ratings yet

- Constitutional MandateDocument5 pagesConstitutional MandateZaira PangesfanNo ratings yet

- Module 1Document10 pagesModule 1Cassandra VenecarioNo ratings yet

- Basic Concepts of Government AccountingDocument10 pagesBasic Concepts of Government AccountingLyra EscosioNo ratings yet

- Aripin BPA 122 Sir VirayDocument3 pagesAripin BPA 122 Sir VirayAripin SangcopanNo ratings yet

- Public FinanceDocument29 pagesPublic FinanceKhanNo ratings yet

- Annual Union Budget - India's Earning & Expenses - Expressions by KT - Tarun's BlogDocument6 pagesAnnual Union Budget - India's Earning & Expenses - Expressions by KT - Tarun's BlogjeevitharkgNo ratings yet

- Budget Making ProcessDocument8 pagesBudget Making ProcessHarsh AgarwalNo ratings yet

- Guide To The Budget 2019Document8 pagesGuide To The Budget 2019amahlemndiyata0615No ratings yet

- Rafsan BPA 122 Sir VirayDocument3 pagesRafsan BPA 122 Sir VirayAripin SangcopanNo ratings yet

- The Budget Making ProcessDocument4 pagesThe Budget Making Processdevilananya2828No ratings yet

- Budgetary and Fiscal Policy Tools PDFDocument5 pagesBudgetary and Fiscal Policy Tools PDFAshagre MekuriaNo ratings yet

- Public Ad (Lecture 19) Budgeting and Financial AdministrationDocument23 pagesPublic Ad (Lecture 19) Budgeting and Financial AdministrationHafiz Farrukh Ishaq IshaqNo ratings yet

- Lesson 3 Activity 4 Main Task Synthesis PaperDocument3 pagesLesson 3 Activity 4 Main Task Synthesis PaperJoseph Ace Tianero LangamNo ratings yet

- Lecture Notes On Philippines BudgetingDocument9 pagesLecture Notes On Philippines Budgetingzkkoech92% (12)

- Mombasa County CBROP 2019 - 2020Document48 pagesMombasa County CBROP 2019 - 2020Mombasa CountyNo ratings yet

- Government Accounting & Financial ReportingDocument37 pagesGovernment Accounting & Financial ReportingSony AxleNo ratings yet

- Process No.5: Preparation of Forward Estimates/Ceilings'Document4 pagesProcess No.5: Preparation of Forward Estimates/Ceilings'Arshad Khan AfridiNo ratings yet

- Budget Preparation Stages at Federal LevelDocument5 pagesBudget Preparation Stages at Federal Levelemebet mulatuNo ratings yet

- LGU Budget ProcessDocument7 pagesLGU Budget ProcessKaren Santos100% (1)

- Tin 160201063310Document73 pagesTin 160201063310martin ngipolNo ratings yet

- 2ND321 - Foundation of EducationDocument26 pages2ND321 - Foundation of EducationMary Rose GonzalesNo ratings yet

- Activity 2 - Temario, Ray CrisDocument5 pagesActivity 2 - Temario, Ray CrisRay Cris TemarioNo ratings yet

- Assignment One ANUDocument18 pagesAssignment One ANUyeshiwas temesgenNo ratings yet

- The Philippine Budget CycleDocument5 pagesThe Philippine Budget CycleMaria Jessamae Caylaluad SaronhiloNo ratings yet

- Budget Process Yojana March 2013 PDFDocument2 pagesBudget Process Yojana March 2013 PDFvipul0457No ratings yet

- 11 Financial ManagementDocument23 pages11 Financial ManagementAmartya MishraNo ratings yet

- Budget 2021 and 2022: A Critical Analysis (Summary)Document5 pagesBudget 2021 and 2022: A Critical Analysis (Summary)Ayushman SinghNo ratings yet

- Budgetary Cycle in IndiaDocument4 pagesBudgetary Cycle in Indiasarayupedada1210No ratings yet

- Econ101 Group AssignmentDocument10 pagesEcon101 Group Assignmentbhallashray101No ratings yet

- What Is The General Accounting Plan of Government Agencies/units?Document2 pagesWhat Is The General Accounting Plan of Government Agencies/units?Che CoronadoNo ratings yet

- Government Accounting Chapter 2Document5 pagesGovernment Accounting Chapter 2Jeca RomeroNo ratings yet

- Topic 4 - Budgeting Daf II-1Document14 pagesTopic 4 - Budgeting Daf II-1kitderoger_391648570No ratings yet

- Psa Class Notes Daf 2020-21Document22 pagesPsa Class Notes Daf 2020-21kitderoger_391648570No ratings yet

- BudgetDocument5 pagesBudgetanthonyNo ratings yet

- Note 1 - MEC 34Document7 pagesNote 1 - MEC 34S GracsNo ratings yet

- Process of Union Budget MakingDocument12 pagesProcess of Union Budget MakingAnkush JadaunNo ratings yet

- Accounting Systems of Local GovernmentDocument5 pagesAccounting Systems of Local GovernmentWasLiana JafarNo ratings yet

- Reaction Paper Public AdDocument4 pagesReaction Paper Public AdAshley Ann Carable100% (1)

- ACCOUNTING 303 Chap 2 TTHS 12.30 1.30Document11 pagesACCOUNTING 303 Chap 2 TTHS 12.30 1.30Fred Michael L. Go100% (1)

- Kisoro District Local Government Report of The Auditor General2017Document21 pagesKisoro District Local Government Report of The Auditor General2017Alex NkurunzizaNo ratings yet

- Strategic Management Assignment 02Document8 pagesStrategic Management Assignment 02Avishka IndulaNo ratings yet

- Public Management Assignment 2Document4 pagesPublic Management Assignment 2Avishka IndulaNo ratings yet

- Econ AssignmentDocument7 pagesEcon AssignmentAvishka IndulaNo ratings yet

- Policy Assignment 2 FinalDocument15 pagesPolicy Assignment 2 FinalAvishka IndulaNo ratings yet

- Other Auto Companies & HR - PuneDocument65 pagesOther Auto Companies & HR - Punerutuja chaudhary100% (1)

- Barómetro Omt Del TurismoDocument18 pagesBarómetro Omt Del TurismoMara Villasanti PortilloNo ratings yet

- Final Question Bank With Answers - Treasury Management-Final ExamDocument7 pagesFinal Question Bank With Answers - Treasury Management-Final ExamHarsh MaheshwariNo ratings yet

- cl-12 Economics Lesson Plan 2023-24Document30 pagescl-12 Economics Lesson Plan 2023-24kuldeepbhatt0786No ratings yet

- Objectives of Financial StatementsDocument3 pagesObjectives of Financial StatementsNelly GomezNo ratings yet

- Evolution of Capitalism 1Document9 pagesEvolution of Capitalism 1jannatin.tajreen.raiyanNo ratings yet

- Five Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearDocument36 pagesFive Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearAsta LavistaNo ratings yet

- Contemporary World - Bretton WoodsDocument18 pagesContemporary World - Bretton WoodsFaith DomingoNo ratings yet

- As We All Are AwareDocument17 pagesAs We All Are AwaremgrfanNo ratings yet

- Lucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaDocument24 pagesLucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaAdisha's100% (1)

- Inland Revenue Board of Malaysia: Eng MalDocument6 pagesInland Revenue Board of Malaysia: Eng Malathirah jamaludinNo ratings yet

- Marketing in Nepalese Microfinance InstitutionsDocument16 pagesMarketing in Nepalese Microfinance InstitutionschiranrgNo ratings yet

- Activity 1 - PAYROLL SYSTEMDocument2 pagesActivity 1 - PAYROLL SYSTEMEmilyn olidNo ratings yet

- 9 - 29 - M&aDocument2 pages9 - 29 - M&aPham Ngoc VanNo ratings yet

- Birth PDFDocument8 pagesBirth PDFspcbanking100% (3)

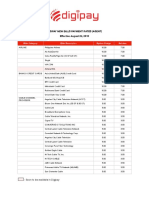

- DIGIPAY New Rates Agent PDFDocument41 pagesDIGIPAY New Rates Agent PDFMye-Khel Lagunay AwayanNo ratings yet

- AbstractDocument45 pagesAbstractMelvin BrionesNo ratings yet

- Senior' ProjectDocument265 pagesSenior' ProjectAayushi ChandwaniNo ratings yet

- MSB ATM GuidanceDocument3 pagesMSB ATM GuidanceJay CaplanNo ratings yet

- Scholarship Form 2023-24Document2 pagesScholarship Form 2023-24Kiran ToplaniNo ratings yet

- Maybank Annual Report 2020 - Financial Statements (English)Document269 pagesMaybank Annual Report 2020 - Financial Statements (English)YikHau NgNo ratings yet

- Call For Calm by Western Leaders After Saudi Execution of Shia ClericDocument40 pagesCall For Calm by Western Leaders After Saudi Execution of Shia ClericstefanoNo ratings yet

- CBIC Civil List As On 01.01.2016Document433 pagesCBIC Civil List As On 01.01.2016रुद्र प्रताप सिंह ८२No ratings yet

- 7 - 1-Market Risk PDFDocument15 pages7 - 1-Market Risk PDFVivek KheparNo ratings yet

- 1 Session - Overfiew of FSADocument45 pages1 Session - Overfiew of FSAAbhishek SwarnkarNo ratings yet

- CHARPY V NOTCH Impact Values (J) (I)Document1 pageCHARPY V NOTCH Impact Values (J) (I)trivendra kumarNo ratings yet

- Portfolio Restructuring DilemmaDocument7 pagesPortfolio Restructuring DilemmaVarun AgrawalNo ratings yet

- Internship Report F (Aaron Lopes)Document66 pagesInternship Report F (Aaron Lopes)Aarxn LopesNo ratings yet

- Utility Analysis - (Unit-3)Document18 pagesUtility Analysis - (Unit-3)pro.firewall00No ratings yet

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- Amazon Interview Secrets: A Complete Guide to Help You to Learn the Secrets to Ace the Amazon Interview Questions and Land Your Dream JobFrom EverandAmazon Interview Secrets: A Complete Guide to Help You to Learn the Secrets to Ace the Amazon Interview Questions and Land Your Dream JobRating: 4.5 out of 5 stars4.5/5 (3)

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- Internal Controls: Guidance for Private, Government, and Nonprofit EntitiesFrom EverandInternal Controls: Guidance for Private, Government, and Nonprofit EntitiesNo ratings yet

- Internal Audit Quality: Developing a Quality Assurance and Improvement ProgramFrom EverandInternal Audit Quality: Developing a Quality Assurance and Improvement ProgramNo ratings yet

- Financial Shenanigans, Fourth Edition: How to Detect Accounting Gimmicks & Fraud in Financial ReportsFrom EverandFinancial Shenanigans, Fourth Edition: How to Detect Accounting Gimmicks & Fraud in Financial ReportsRating: 4 out of 5 stars4/5 (26)

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- Building a World-Class Compliance Program: Best Practices and Strategies for SuccessFrom EverandBuilding a World-Class Compliance Program: Best Practices and Strategies for SuccessNo ratings yet

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowFrom EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNo ratings yet

- Electronic Health Records: An Audit and Internal Control GuideFrom EverandElectronic Health Records: An Audit and Internal Control GuideNo ratings yet

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet