You might also like

- 80G RC 02jul21Document3 pages80G RC 02jul21Priya Vijay kumaarNo ratings yet

- MFnew 80 G AAETM3161 EF20214Document2 pagesMFnew 80 G AAETM3161 EF20214Nisha PanchalNo ratings yet

- 80G OrderDocument2 pages80G OrderTHE R V 0007No ratings yet

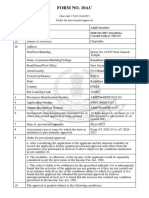

- Form No. 10ac: (See Rule 17A/11AA/2C) Order For Provisional Approval PAN ADSPE8580C ElayarajaDocument3 pagesForm No. 10ac: (See Rule 17A/11AA/2C) Order For Provisional Approval PAN ADSPE8580C ElayarajaPriya Vijay kumaarNo ratings yet

- 12a Aabtm0174ge20046 SignedDocument3 pages12a Aabtm0174ge20046 SignedPrashant MujumdarNo ratings yet

- Aacau4985hf20231 SignedDocument2 pagesAacau4985hf20231 SignedDebendra DasNo ratings yet

- Form No. 10acDocument3 pagesForm No. 10acAnkit DineshNo ratings yet

- Form No. 10acDocument2 pagesForm No. 10acAditya NayakNo ratings yet

- 12 AA Copy (BEST)Document2 pages12 AA Copy (BEST)vadivelmurugan rNo ratings yet

- 80g CertificateDocument2 pages80g CertificateROHIT SHARMANo ratings yet

- AARTS9794AF20241 SignedDocument2 pagesAARTS9794AF20241 SignedRameshwar sableNo ratings yet

- Form No. 10acDocument2 pagesForm No. 10acAditya NayakNo ratings yet

- AARTS9794AE20231 SignedDocument2 pagesAARTS9794AE20231 SignedRameshwar sableNo ratings yet

- 80G ExempDocument2 pages80G ExempATM-Ops MangaloreNo ratings yet

- Name and Address of The ApplicantDocument2 pagesName and Address of The ApplicantAbbas AliNo ratings yet

- Name and Address of The ApplicantDocument3 pagesName and Address of The ApplicantOrangetree ArtNo ratings yet

- AAETA0890J - Order Us 80G - 1019180029Document2 pagesAAETA0890J - Order Us 80G - 1019180029Donor CrewNo ratings yet

- Satirtha 12ADocument2 pagesSatirtha 12ADebasish Monimugdha BhuyanNo ratings yet

- In Re Senco Gold LTD GST AAR West BangalDocument4 pagesIn Re Senco Gold LTD GST AAR West Bangalkinnar2013No ratings yet

- 2023721217646921CircularNo 1of2023-2024Document4 pages2023721217646921CircularNo 1of2023-2024krebs38No ratings yet

- Form 3CD - Meenakshi SoniDocument15 pagesForm 3CD - Meenakshi SoniAditya AroraNo ratings yet

- EnglishPrintNotice (1) 230414 143818Document438 pagesEnglishPrintNotice (1) 230414 143818rekha kumariNo ratings yet

- Doc-20231022-Wa0005 231022 090138Document9 pagesDoc-20231022-Wa0005 231022 090138kumarhealthcare2000No ratings yet

- Cir 188 20 2022 CGSTDocument4 pagesCir 188 20 2022 CGSTAtanu Kumar SenNo ratings yet

- Chapter - Registration 1. Application For Registration: Form GST Reg-01Document10 pagesChapter - Registration 1. Application For Registration: Form GST Reg-01Abhishek MehtaNo ratings yet

- Section 74 Reply Narachi IndustriesDocument9 pagesSection 74 Reply Narachi Industriesbirpal singhNo ratings yet

- Reportable: Siddharth ChaturvediDocument44 pagesReportable: Siddharth ChaturvediKarthikaNo ratings yet

- ARI AB MSBs Pawnshops and DNFBPsDocument2 pagesARI AB MSBs Pawnshops and DNFBPsRemy Rose AlegreNo ratings yet

- 15CADocument2 pages15CAavinash14 neereNo ratings yet

- Form 15CADocument4 pagesForm 15CAManoj MahimkarNo ratings yet

- Before The High Court of Karnataka at Bengaluru WRIT PETITION NO. 58209/2018 (L-PF) BetweenDocument8 pagesBefore The High Court of Karnataka at Bengaluru WRIT PETITION NO. 58209/2018 (L-PF) BetweenkirumcaNo ratings yet

- CNDS Ceb IpesDocument4 pagesCNDS Ceb IpesNey Milk RomãoNo ratings yet

- SEBI Circular Dated 03112021 ClarificationDocument13 pagesSEBI Circular Dated 03112021 ClarificationKrunalNo ratings yet

- Ranjana Singh Vs Commissioner of State Tax Allahabad High CourtDocument12 pagesRanjana Singh Vs Commissioner of State Tax Allahabad High Courtkumarhealthcare2000No ratings yet

- DSCN Aa TradersDocument13 pagesDSCN Aa TradersIAS MeenaNo ratings yet

- JudgementbyjdateDocument27 pagesJudgementbyjdateBasanta Kumar SahooNo ratings yet

- circular-CBDT Clarifies Provisions RelatingDocument6 pagescircular-CBDT Clarifies Provisions RelatingYogesh KanojiyaNo ratings yet

- S. A. Bobde, Cji, B. R. Gavai and Surya Kant, Jj.Document7 pagesS. A. Bobde, Cji, B. R. Gavai and Surya Kant, Jj.yvonnewebster626No ratings yet

- SEBI CiruclarsDocument41 pagesSEBI Ciruclars25Oct 20No ratings yet

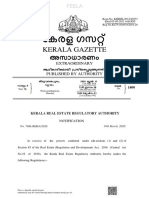

- RERA Regulations 2020 Dt.11.06.2020 - FDocument44 pagesRERA Regulations 2020 Dt.11.06.2020 - FSajith KumarNo ratings yet

- Extra Extra Extra Extra Extraordinar Ordinar Ordinar Ordinar Ordinary Y Y Y YDocument28 pagesExtra Extra Extra Extra Extraordinar Ordinar Ordinar Ordinar Ordinary Y Y Y YAll India Brahmin MorchaNo ratings yet

- (Anil Choudhary) Member (Judicial) : (Order Dictated in The Open Court)Document2 pages(Anil Choudhary) Member (Judicial) : (Order Dictated in The Open Court)Akash chandoraNo ratings yet

- Application For RegistrationDocument9 pagesApplication For RegistrationSarinNo ratings yet

- G.R. No. 154126Document3 pagesG.R. No. 154126GraceNo ratings yet

- KMC (Amendment) Act, 2021Document9 pagesKMC (Amendment) Act, 2021Kushwanth KumarNo ratings yet

- Payment of Bonus Act Case LawDocument3 pagesPayment of Bonus Act Case LawShivaNo ratings yet

- Maruti Suzuki India LTD 0Document97 pagesMaruti Suzuki India LTD 0AMAN KUMAR 20213009No ratings yet

- Nomination Sebi Circular On NominationDocument20 pagesNomination Sebi Circular On NominationGunvant ThakkarNo ratings yet

- Kerala State Electricity Connections - .. . . ( ) ., ,, ,, , .Document11 pagesKerala State Electricity Connections - .. . . ( ) ., ,, ,, , .James AdhikaramNo ratings yet

- Form ISR-1Document4 pagesForm ISR-1deepisd3 veganpurNo ratings yet

- Tax Project ADocument8 pagesTax Project APreeti BafnaNo ratings yet

- DAO No. 10-08Document12 pagesDAO No. 10-08dannielamorinNo ratings yet

- No Itc Reversal Demand W o Investigating Supplier DB Calhc 1690968957Document10 pagesNo Itc Reversal Demand W o Investigating Supplier DB Calhc 1690968957Dhanashree Prasanna Phadke ValanjooNo ratings yet

- Volga D 604 AgreementDocument5 pagesVolga D 604 AgreementSaddam YusufNo ratings yet

- REC Infra Bond Application FormDocument2 pagesREC Infra Bond Application FormPrajna CapitalNo ratings yet

- SFT CompliancesDocument51 pagesSFT CompliancesDevPantNo ratings yet

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintFrom EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintRating: 4 out of 5 stars4/5 (1)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- NzersrightsDocument5 pagesNzersrightsC&R Media50% (2)

- Nirma University: Institute of Law (Semester I, BALLB)Document15 pagesNirma University: Institute of Law (Semester I, BALLB)moshadab khanNo ratings yet

- Southern Rhodesia War 1860-67 PDFDocument24 pagesSouthern Rhodesia War 1860-67 PDFMaria Paula MenesesNo ratings yet

- Dave Waite - Bankruptcy Proceedings in BarbadosDocument4 pagesDave Waite - Bankruptcy Proceedings in BarbadosClaudine BaileyNo ratings yet

- Russia S GravediggersDocument38 pagesRussia S Gravediggersadavielchiù75% (4)

- CATCH 22 Complete TextDocument157 pagesCATCH 22 Complete Textmicksoul100% (1)

- 220921File-Stamped - Complaint - Worldwide NFT v. CalasseDocument71 pages220921File-Stamped - Complaint - Worldwide NFT v. CalasseGeorge SharpNo ratings yet

- The German Army (1939-45)Document50 pagesThe German Army (1939-45)gottesvieh100% (11)

- Howard Winant InterviewDocument3 pagesHoward Winant InterviewNorton SociologyNo ratings yet

- What Is Women Empowerment?: HistoryDocument1 pageWhat Is Women Empowerment?: HistoryMaryam QureshiNo ratings yet

- Unit 3 - Ottoman Empire Case Study (Documents)Document8 pagesUnit 3 - Ottoman Empire Case Study (Documents)Travy PattyNo ratings yet

- Bangladesh Why It HappenedDocument9 pagesBangladesh Why It HappenedAzad Master100% (1)

- 6.LearnEnglish Speaking B1 Responding To NewsDocument4 pages6.LearnEnglish Speaking B1 Responding To NewsLidiaNo ratings yet

- The Ultimate Guide To ECP-742 Ericsson Certified Professional - Radio Network DesignDocument2 pagesThe Ultimate Guide To ECP-742 Ericsson Certified Professional - Radio Network DesignStefanNo ratings yet

- Case 4:19-cv-00681-SDJDocument6 pagesCase 4:19-cv-00681-SDJJun YiNo ratings yet

- Baptism of The Holy Ghost - FoleyDocument32 pagesBaptism of The Holy Ghost - FoleyManuel DelgadoNo ratings yet

- Gec 102 Activity 6 The Cry of Pugad LawinDocument5 pagesGec 102 Activity 6 The Cry of Pugad LawinDaylan Lindo MontefalcoNo ratings yet

- Module 3 Lesson 4 The Concept of Filipino and Filipino NationalismDocument8 pagesModule 3 Lesson 4 The Concept of Filipino and Filipino Nationalismcarlo francisco100% (1)

- FQDocument3 pagesFQCristinaNo ratings yet

- Oral Comm PTDocument2 pagesOral Comm PTmyoui minaNo ratings yet

- Strub - 'The Theory of Panoptical Control'Document20 pagesStrub - 'The Theory of Panoptical Control'Kam Ho M. WongNo ratings yet

- Back Drop SkullportDocument10 pagesBack Drop SkullportBrent G Landry100% (1)

- Twilight 2013 - Player Characters - Americans (93GS1501)Document17 pagesTwilight 2013 - Player Characters - Americans (93GS1501)Fro Sem40% (5)

- Seal or Stamp. - The Penalty of Prision MayorDocument20 pagesSeal or Stamp. - The Penalty of Prision MayorMohammad Haitham M. SaripNo ratings yet

- 2020 LS Seatwork 3 Book IIIDocument6 pages2020 LS Seatwork 3 Book IIIJustin Dominic ManaogNo ratings yet

- Positive AffirmationsDocument3 pagesPositive AffirmationsraashieeNo ratings yet

- The Truth About AurangzebDocument21 pagesThe Truth About AurangzebAcfor NadiNo ratings yet

- (American Encounters - Global Interactions) Kirsten Weld - Paper Cadavers - The Archives of Dictatorship in Guatemala-Duke University Press Books (2014)Document352 pages(American Encounters - Global Interactions) Kirsten Weld - Paper Cadavers - The Archives of Dictatorship in Guatemala-Duke University Press Books (2014)Marinella Cruz100% (1)

- Letter to J. Hogan, K.C., M.L.a.Document4 pagesLetter to J. Hogan, K.C., M.L.a.andrewldwatermanNo ratings yet

- United States Court of Appeals Fourth CircuitDocument7 pagesUnited States Court of Appeals Fourth CircuitScribd Government DocsNo ratings yet