You might also like

- Lone Pine Café: Transaction Sheet For 1st Nov 05Document6 pagesLone Pine Café: Transaction Sheet For 1st Nov 05Dhanu ArunNo ratings yet

- Year-End Financial Statements for 2014Document2 pagesYear-End Financial Statements for 2014MutiaraNo ratings yet

- Prac PaDocument20 pagesPrac PaTrương Mỹ HạnhNo ratings yet

- ACC101Document9 pagesACC101Tran Vo Van Anh (K17 HCM)No ratings yet

- Assets Liabilities Date Cash + Accounts Receivable + Equipment Accounts PayableDocument11 pagesAssets Liabilities Date Cash + Accounts Receivable + Equipment Accounts PayableAadit AggarwalNo ratings yet

- Date Cash Supplies Equipment A/C Payble Notes Payable Capital Remarks Accounts ReceivableDocument15 pagesDate Cash Supplies Equipment A/C Payble Notes Payable Capital Remarks Accounts ReceivablesnigdhaNo ratings yet

- 2015 Balance Sheet for CompanyDocument41 pages2015 Balance Sheet for CompanyWendelyn ShieNo ratings yet

- ProblemsDocument30 pagesProblemssrijiet agarwalNo ratings yet

- Abhijit Company (PG No 483) : Cash Flow From Operating ActivitiesDocument4 pagesAbhijit Company (PG No 483) : Cash Flow From Operating ActivitiesMaryNo ratings yet

- Simbol Cont Denumire Cont Solduri Initiale Rulaje Total Sume Solduri Finale Debit Credit Debit Credit Debit Credit Debit Credit 1012Document2 pagesSimbol Cont Denumire Cont Solduri Initiale Rulaje Total Sume Solduri Finale Debit Credit Debit Credit Debit Credit Debit Credit 1012nador2302@yahoo.comNo ratings yet

- Accounts List SummaryDocument1 pageAccounts List SummaryCahya AgungNo ratings yet

- An Sa CT IonDocument2 pagesAn Sa CT IonCharisa BenjaminNo ratings yet

- Balancesheet As On 31st May 2012 Liabilities Rs Assets RsDocument3 pagesBalancesheet As On 31st May 2012 Liabilities Rs Assets Rsrahul.iamNo ratings yet

- Cash Loan Supply Expense Tools Salary Expense Down Payment Bills Paypable Tool Expense Services Telephone Ex Office Supplies Petrol Ex Recieable RentDocument4 pagesCash Loan Supply Expense Tools Salary Expense Down Payment Bills Paypable Tool Expense Services Telephone Ex Office Supplies Petrol Ex Recieable RenttanimaNo ratings yet

- Finance - Chap2Document24 pagesFinance - Chap2Nguyễn Thị Thu PhươngNo ratings yet

- Kapoor Software LTDDocument5 pagesKapoor Software LTDluniapNo ratings yet

- Jone's Mower Repairs Income Statement and Balance SheetDocument23 pagesJone's Mower Repairs Income Statement and Balance SheetNguyễn Thị Thu PhươngNo ratings yet

- Item Unit Qty Rams Hinunangan ManilaDocument6 pagesItem Unit Qty Rams Hinunangan Manilamarven estinozoNo ratings yet

- Assets Liabilities Income ExpenditureDocument16 pagesAssets Liabilities Income ExpenditurevidyaNo ratings yet

- Profit or Loss1 PDFDocument7 pagesProfit or Loss1 PDFdanishahmed2126No ratings yet

- Accounts: Trial Balance Adjustments Adjusted T.BDocument2 pagesAccounts: Trial Balance Adjustments Adjusted T.BJaqueline Sarkis IssaNo ratings yet

- Trial Balance AssignmentDocument2 pagesTrial Balance AssignmentRavi BodhNo ratings yet

- Tubing Correlation Match Parameters AnalysisDocument50 pagesTubing Correlation Match Parameters AnalysisMarcelo Ayllón RiberaNo ratings yet

- A1Document1 pageA1Anushka PereraNo ratings yet

- B&B Repair Services Income StatementDocument22 pagesB&B Repair Services Income Statementrhyayuli0% (1)

- PT Ramawijaya Sport Memorial Journal Adjustment December 2017Document29 pagesPT Ramawijaya Sport Memorial Journal Adjustment December 2017DarDer DorNo ratings yet

- Shubham Blooms Feb 2021 Maintenance CollectionDocument8 pagesShubham Blooms Feb 2021 Maintenance CollectionVedha UmakanthNo ratings yet

- Akuntansi NadhipDocument9 pagesAkuntansi NadhipGeordhan AlexanderNo ratings yet

- PT.LP3i ADJUSTMENT JOURNALDocument9 pagesPT.LP3i ADJUSTMENT JOURNALRendyyyNo ratings yet

- Trial Balance Lks 18Document2 pagesTrial Balance Lks 18M. SofyanNo ratings yet

- WS PT SUBURDocument2 pagesWS PT SUBURrendipakpahan21No ratings yet

- P4 1Document1 pageP4 1Arnalistan Eka100% (1)

- P4 1Document1 pageP4 1Arnalistan EkaNo ratings yet

- BudgetDocument10 pagesBudgetEranda SDNo ratings yet

- Free CashflowDocument4 pagesFree CashflowMainali GautamNo ratings yet

- BEA1007 Tutorial 2 SolutionsDocument12 pagesBEA1007 Tutorial 2 SolutionsBecca CrossNo ratings yet

- General Ledger SummaryDocument1 pageGeneral Ledger Summaryaj1622ajengNo ratings yet

- Bank account transaction summaryDocument4 pagesBank account transaction summaryMikaella LamadoraNo ratings yet

- Accounting: AssignmentDocument4 pagesAccounting: Assignmentiza khanNo ratings yet

- GPLANDocument1 pageGPLANMuhammad Auwal TahirNo ratings yet

- Profit and Loss Template Under 77k Turnover 1Document2 pagesProfit and Loss Template Under 77k Turnover 1Edem Kofi BoniNo ratings yet

- Grand Tota ### ### ### ### ### ### ### ### ###Document2 pagesGrand Tota ### ### ### ### ### ### ### ### ###Asif MasihNo ratings yet

- Fee Structure 2022 23Document1 pageFee Structure 2022 23Uday Raj (Raghav)No ratings yet

- Worksheets 2022 FarDocument7 pagesWorksheets 2022 FarMariñas, Romalyn D.No ratings yet

- Terakhir P4-1Document1 pageTerakhir P4-1Arnalistan EkaNo ratings yet

- Work Sheet 4A2Document1 pageWork Sheet 4A2SohailAKramNo ratings yet

- Nokia Price ListDocument1 pageNokia Price ListRahul RajanNo ratings yet

- General Ledger SummaryDocument2 pagesGeneral Ledger SummaryiniakuntugasasligaboongdahNo ratings yet

- Trial Balance AdjustmentsDocument7 pagesTrial Balance AdjustmentsArnab HazraNo ratings yet

- NirmalaDocument3 pagesNirmalaswamilpatniNo ratings yet

- OTDR Advanced Cable Report: Location A Location BDocument12 pagesOTDR Advanced Cable Report: Location A Location BEdher ChavezNo ratings yet

- PC DepotDocument26 pagesPC Depotvishakha AGRAWALNo ratings yet

- Compact track loader dimensions and specificationsDocument2 pagesCompact track loader dimensions and specificationsnam nguyenNo ratings yet

- SOFN enDocument1 pageSOFN enAlexandre GiliiNo ratings yet

- Tugas Akuntan PRDocument4 pagesTugas Akuntan PRShelamita lestariNo ratings yet

- Problem 2.12 - SolutionDocument8 pagesProblem 2.12 - SolutiontanimaNo ratings yet

- Seminar Ratio Analysis 2Document2 pagesSeminar Ratio Analysis 2Muhammad Sajid SaeedNo ratings yet

- Juarez Inc Job Order Cost Sheets (1) March 1 Job 621 Job 622Document3 pagesJuarez Inc Job Order Cost Sheets (1) March 1 Job 621 Job 622ramaNo ratings yet

- Studi Kasus Menyusun Laporan Perusahaan Dagang PerpetualDocument16 pagesStudi Kasus Menyusun Laporan Perusahaan Dagang PerpetualAulia AmandaNo ratings yet

- Database Management Systems: Understanding and Applying Database TechnologyFrom EverandDatabase Management Systems: Understanding and Applying Database TechnologyRating: 4 out of 5 stars4/5 (8)

- GenderDocument6 pagesGenderSatyamNo ratings yet

- Importance of Ratios to Different User GroupsDocument2 pagesImportance of Ratios to Different User GroupsShruti ShivhareNo ratings yet

- 450e Candidate ApplicationDocument2 pages450e Candidate ApplicationShruti ShivhareNo ratings yet

- Cash Flow Statement AnalysisDocument7 pagesCash Flow Statement AnalysisShruti ShivhareNo ratings yet

- Afya 2021Document80 pagesAfya 2021Ayushika SinghNo ratings yet

- Cross-Asset Class Momentum: Bill ZieffDocument23 pagesCross-Asset Class Momentum: Bill Zieffpietro silvestriNo ratings yet

- 1 1 Investment Management Interview QuestionsDocument3 pages1 1 Investment Management Interview Questionsdeepu9989No ratings yet

- ICRA Press Release - NBFC - July 20th 2023Document3 pagesICRA Press Release - NBFC - July 20th 2023RajNo ratings yet

- Ifm - 5Document17 pagesIfm - 5Tường LinhNo ratings yet

- Research Paper - Evaluating Institutional Factors Contributing To Default in Loan Repayment Within Microfinance Institutions in JamaicaDocument68 pagesResearch Paper - Evaluating Institutional Factors Contributing To Default in Loan Repayment Within Microfinance Institutions in JamaicaCecile S CameronNo ratings yet

- 2011 07 A Short Note On The Tobin Tax The Costs and Benefts of A Tax On Financial Transactions EDHECDocument72 pages2011 07 A Short Note On The Tobin Tax The Costs and Benefts of A Tax On Financial Transactions EDHECVincent_Delaru_4396No ratings yet

- Finance for Managers: Financial Markets GuideDocument5 pagesFinance for Managers: Financial Markets GuidehonathapyarNo ratings yet

- 9th Comparative AnalysisDocument98 pages9th Comparative AnalysisJeanMarieFourquinNo ratings yet

- Binary Options Made SimpleDocument49 pagesBinary Options Made SimpleMr Binary Option100% (5)

- Notice of 15th AGM On 16 09 2021Document13 pagesNotice of 15th AGM On 16 09 2021Edward DevisNo ratings yet

- Lesson 2 The EMA BounceDocument32 pagesLesson 2 The EMA BounceVagueNo ratings yet

- Tensor Charts ScalpingDocument10 pagesTensor Charts Scalpingpotfictio100% (1)

- Capital budgeting M&A appraisalDocument5 pagesCapital budgeting M&A appraisalMuhammad QaiserNo ratings yet

- Assessing E-Banking in Nam Dinh, Viet NamDocument180 pagesAssessing E-Banking in Nam Dinh, Viet NamDo NganNo ratings yet

- Santos ECO Fin HW03Document5 pagesSantos ECO Fin HW03cohenbry1125No ratings yet

- Option Strategy Cheat Sheet: Condition Volatility Skew Time NotesDocument1 pageOption Strategy Cheat Sheet: Condition Volatility Skew Time Notesraj33% (3)

- Arbitrage - Free Pricing ModelsDocument43 pagesArbitrage - Free Pricing ModelsororoNo ratings yet

- Risk and ReturnDocument9 pagesRisk and ReturnNgọc LinggNo ratings yet

- 3PPP Certification Guide AcknowledgementsDocument9 pages3PPP Certification Guide AcknowledgementsTomasz CzNo ratings yet

- Price Change: Cash Flow or Discount Rate?: Asset Pricing Zheng ZhenlongDocument39 pagesPrice Change: Cash Flow or Discount Rate?: Asset Pricing Zheng ZhenlongAryen RajNo ratings yet

- Maximize Shareholder Value with Optimal Capital BudgetingDocument72 pagesMaximize Shareholder Value with Optimal Capital BudgetingZijian ZHUNo ratings yet

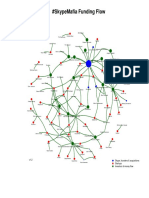

- SkypeMafia Funding Flow ChartDocument1 pageSkypeMafia Funding Flow ChartMarius Cristian IspasNo ratings yet

- ImpairmentsDocument3 pagesImpairmentsjingyuu kimNo ratings yet

- MGMT3000 2020 S2 Final ExamDocument4 pagesMGMT3000 2020 S2 Final ExamhaohtsNo ratings yet

- WTI Commodity Price Analysis: WTI Oil As of June 2020Document4 pagesWTI Commodity Price Analysis: WTI Oil As of June 2020JHON EFRAIN POMA ROSALESNo ratings yet

- Benjamin Graham Articles Magazine of Wall Street 1917-1922Document142 pagesBenjamin Graham Articles Magazine of Wall Street 1917-1922Anonymous CP6MdC7S4TNo ratings yet

- Symbol List I Glob Le Index 20120123Document26 pagesSymbol List I Glob Le Index 20120123Peter ZhangNo ratings yet

- Caselet Master TV India Answers 2020Document2 pagesCaselet Master TV India Answers 2020shirley zhangNo ratings yet

- Chistruga Vladislav 2) Analysis of observance of the net working capital requiremenеntDocument2 pagesChistruga Vladislav 2) Analysis of observance of the net working capital requiremenеntVladuț KistrugaNo ratings yet