You might also like

- Persistent Sys Case StudyDocument34 pagesPersistent Sys Case StudyGrim ReaperNo ratings yet

- Tata ElxsiDocument34 pagesTata Elxsijameelk786No ratings yet

- EdgeReport TATAELXSI CaseStudy 10 04 2023 417Document34 pagesEdgeReport TATAELXSI CaseStudy 10 04 2023 417Department of power MIS CellNo ratings yet

- Britannia Case StudyDocument34 pagesBritannia Case StudyGrim ReaperNo ratings yet

- EdgeReport BRITANNIA CaseStudy 07 09 2022 994Document34 pagesEdgeReport BRITANNIA CaseStudy 07 09 2022 994aadil suhailNo ratings yet

- EdgeReport NILKAMAL CaseStudy 13 01 2022 348Document34 pagesEdgeReport NILKAMAL CaseStudy 13 01 2022 348Im CandlestickNo ratings yet

- EdgeReport RELAXO CaseStudy 14 01 2022 450Document34 pagesEdgeReport RELAXO CaseStudy 14 01 2022 450Im CandlestickNo ratings yet

- EdgeReport AFFLE CaseStudy 23 12 2022 883Document36 pagesEdgeReport AFFLE CaseStudy 23 12 2022 883amsukdNo ratings yet

- Case Study Cera SanitDocument34 pagesCase Study Cera SanitGrim ReaperNo ratings yet

- HDFC AMC Case StudyDocument34 pagesHDFC AMC Case StudyGrim ReaperNo ratings yet

- EdgeReport PAGEIND CaseStudy 20 09 2022 1048Document35 pagesEdgeReport PAGEIND CaseStudy 20 09 2022 1048aadil suhailNo ratings yet

- EdgeReport BALKRISIND CaseStudy 17 03 2022 682Document35 pagesEdgeReport BALKRISIND CaseStudy 17 03 2022 682Im CandlestickNo ratings yet

- Col Pal Case StudyDocument34 pagesCol Pal Case StudyGrim ReaperNo ratings yet

- Dabur Case StudyDocument35 pagesDabur Case StudyUdaya Vijay AnandNo ratings yet

- Balrampur Chini Mills Limited: Case StudyDocument33 pagesBalrampur Chini Mills Limited: Case StudyAmitabh VatsyaNo ratings yet

- Indian Hotels Company Case StudyDocument34 pagesIndian Hotels Company Case StudyEquity NestNo ratings yet

- Jubilant Food Stock Report PDFDocument33 pagesJubilant Food Stock Report PDFPranav WarneNo ratings yet

- EdgeReport AFFLE CaseStudyDocument36 pagesEdgeReport AFFLE CaseStudySandyNo ratings yet

- EdgeReport JUBLFOOD CaseStudy 27 12 2023 348Document36 pagesEdgeReport JUBLFOOD CaseStudy 27 12 2023 348vijaygawdeNo ratings yet

- Cost & Management Accounting: Cia-IiiDocument9 pagesCost & Management Accounting: Cia-IiiARYAN GARG 19212016No ratings yet

- EdgeReport BALKRISIND CaseStudy 22-11-2022 240Document34 pagesEdgeReport BALKRISIND CaseStudy 22-11-2022 240malayalamedits100No ratings yet

- PB Fintech Icici SecuritiesDocument33 pagesPB Fintech Icici SecuritieshamsNo ratings yet

- Indag Rubber Note Jan20 2016Document5 pagesIndag Rubber Note Jan20 2016doodledeeNo ratings yet

- Exide LTD Market Impact Q1FY19Document2 pagesExide LTD Market Impact Q1FY19Shihab MonNo ratings yet

- Buisness RareDocument22 pagesBuisness RareALINA ZohqNo ratings yet

- Middle East Working Capital Study 2023Document21 pagesMiddle East Working Capital Study 2023alhadipress3No ratings yet

- BalrampurChinni CaseStudy StockEdge 2010628Document34 pagesBalrampurChinni CaseStudy StockEdge 2010628Sureshbabu LakshminarayananNo ratings yet

- Divis RRDocument10 pagesDivis RRRicha P SinghalNo ratings yet

- Analytical Annexures Q2FY23Document24 pagesAnalytical Annexures Q2FY23Kdp03No ratings yet

- Technology: IndiaDocument9 pagesTechnology: IndiabradburywillsNo ratings yet

- Vaibhav Global Research ReportDocument4 pagesVaibhav Global Research ReportVikrant SadanaNo ratings yet

- Syngene International: Discovery Services Driving Growth Outlook UpbeatDocument11 pagesSyngene International: Discovery Services Driving Growth Outlook Upbeatsanketsabale26No ratings yet

- April 2022Document43 pagesApril 2022Indraneel MahantiNo ratings yet

- Amfr Writeup FinalDocument9 pagesAmfr Writeup FinalTanya AgarwalNo ratings yet

- 4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedDocument5 pages4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedbradburywillsNo ratings yet

- 2021 KBCM SaaS SurveyDocument71 pages2021 KBCM SaaS SurveyAdriaan StormeNo ratings yet

- BEML - Annual Report - FY 2020-2021Document278 pagesBEML - Annual Report - FY 2020-2021NILESH SHETENo ratings yet

- Avenue Supermarts: CMP: INR5,360 TP: INR4,900 (-9%) Continuing To Deliver On GrowthDocument10 pagesAvenue Supermarts: CMP: INR5,360 TP: INR4,900 (-9%) Continuing To Deliver On GrowthLucifer GamerzNo ratings yet

- Golden Midcap Portfolio: June 1, 2021Document7 pagesGolden Midcap Portfolio: June 1, 2021Ram KumarNo ratings yet

- CXO Increments Survey 2023 ReportDocument12 pagesCXO Increments Survey 2023 Reportmarvel mNo ratings yet

- 4Q20 Shareholder LetterDocument28 pages4Q20 Shareholder LettermfajsemNo ratings yet

- BIDU - Q1 2019 Earnings Release 2Document12 pagesBIDU - Q1 2019 Earnings Release 2Dragon RopaNo ratings yet

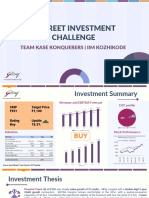

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- RaymondDocument11 pagesRaymondAbhinav VarmaNo ratings yet

- Chairman's Message PDFDocument2 pagesChairman's Message PDFharshit abrolNo ratings yet

- B2B SaaS Metrics Benchmark 2023 REPORTDocument51 pagesB2B SaaS Metrics Benchmark 2023 REPORTstartupcommunity.top100% (1)

- Ap A2.1Document10 pagesAp A2.1Dat HoangNo ratings yet

- Letter To ShareholdersDocument3 pagesLetter To ShareholdersMku MkuNo ratings yet

- Spark Pidilite Industries - Update - Mar2021Document28 pagesSpark Pidilite Industries - Update - Mar2021Akshaya SrihariNo ratings yet

- Fsa PresDocument5 pagesFsa PresHayab SafdarNo ratings yet

- SFE Investor Presentation May 2020 PDFDocument28 pagesSFE Investor Presentation May 2020 PDFEngr Qaisar NazeerNo ratings yet

- Vodafone Idea Limited - Annual Report - 2017-18 PDFDocument228 pagesVodafone Idea Limited - Annual Report - 2017-18 PDFAniruddh KanodiaNo ratings yet

- FSN E-Commerce Ventures Ltd. (Nykaa) : All You Need To Know AboutDocument7 pagesFSN E-Commerce Ventures Ltd. (Nykaa) : All You Need To Know AboutFact checkoutNo ratings yet

- DuPont Ratio AnalysisDocument3 pagesDuPont Ratio AnalysisNayan ChudasamaNo ratings yet

- Happiest Minds LTD IPO: Reason For Subscribing To The IPODocument3 pagesHappiest Minds LTD IPO: Reason For Subscribing To The IPODebjit AdakNo ratings yet

- Angel One: IndiaDocument9 pagesAngel One: IndiaRam JaneNo ratings yet

- Kriti Industries 2019 PDFDocument132 pagesKriti Industries 2019 PDFPuneet367No ratings yet

- Zomato Limited ReportDocument7 pagesZomato Limited Reportshivkumar singh100% (1)

- Fsa Analysis Final For Printout GgsDocument52 pagesFsa Analysis Final For Printout GgsKshitij GuptaNo ratings yet

- Case Study-Apollo HospDocument36 pagesCase Study-Apollo HospGrim ReaperNo ratings yet

- India Equity Strategy HSBC 260122Document10 pagesIndia Equity Strategy HSBC 260122Grim ReaperNo ratings yet

- Valiant Organic BP Wealth 280122Document19 pagesValiant Organic BP Wealth 280122Grim ReaperNo ratings yet

- RBI Introduces Scale-Based Regulations For NBFCsDocument5 pagesRBI Introduces Scale-Based Regulations For NBFCsGrim ReaperNo ratings yet

- SRE Diwali Picks 2021Document7 pagesSRE Diwali Picks 2021vikasNo ratings yet

- Supreme Industries LTD: ESG Disclosure ScoreDocument7 pagesSupreme Industries LTD: ESG Disclosure ScoreGrim ReaperNo ratings yet

- Col Pal Case StudyDocument34 pagesCol Pal Case StudyGrim ReaperNo ratings yet

- HDFC AMC Case StudyDocument34 pagesHDFC AMC Case StudyGrim ReaperNo ratings yet

- Commodity Technical Report July 26Document7 pagesCommodity Technical Report July 26Grim ReaperNo ratings yet

- Case Study Cera SanitDocument34 pagesCase Study Cera SanitGrim ReaperNo ratings yet

- Case Study-Apollo HospDocument36 pagesCase Study-Apollo HospGrim ReaperNo ratings yet

- Bain Report India Private Equity Report 2020Document60 pagesBain Report India Private Equity Report 2020Grim ReaperNo ratings yet

- Autos: Two Wheelers: Sector ThematicDocument37 pagesAutos: Two Wheelers: Sector ThematicGrim ReaperNo ratings yet

- Abbott India-AAA-210906-Edited (2) - 22-09-2021 - 11Document18 pagesAbbott India-AAA-210906-Edited (2) - 22-09-2021 - 11Grim ReaperNo ratings yet

- Atul LTD: ESG Disclosure ScoreDocument7 pagesAtul LTD: ESG Disclosure ScoreGrim ReaperNo ratings yet

- Adani Case StudyDocument35 pagesAdani Case StudyGrim ReaperNo ratings yet

- 9.0 Responsibility Accounting 2018Document14 pages9.0 Responsibility Accounting 2018Emily SongNo ratings yet

- Bundl Technologies Private Limited: Detailed ReportDocument14 pagesBundl Technologies Private Limited: Detailed Reportb0gm3n0tNo ratings yet

- Accounting TheoryDocument6 pagesAccounting TheoryAPRIL ROSE YOSORESNo ratings yet

- CIMA F2 NotesDocument154 pagesCIMA F2 Notesakirevski001100% (1)

- Fa S23 Introduction To Consolidated Financial StatementsDocument9 pagesFa S23 Introduction To Consolidated Financial StatementsCharisma CharlesNo ratings yet

- Finance - Cost of Capital TheoryDocument30 pagesFinance - Cost of Capital TheoryShafkat RezaNo ratings yet

- The Accounting Equation (Financial Accounting)Document5 pagesThe Accounting Equation (Financial Accounting)RidwanAbirNo ratings yet

- Persamaan Akuntansi2Document11 pagesPersamaan Akuntansi2anon_121015384No ratings yet

- Vietnam Financial Structure: The Overview of Direct and Indirect Finance in Viet Nam 1Document5 pagesVietnam Financial Structure: The Overview of Direct and Indirect Finance in Viet Nam 1Hiền NguyễnNo ratings yet

- AccountingDocument5 pagesAccountingMoira C. VilogNo ratings yet

- La Trobe Cash QuestionDocument2 pagesLa Trobe Cash QuestionKimberly MarkNo ratings yet

- Pershing Square Q2 LetterDocument11 pagesPershing Square Q2 Lettermarketfolly.com100% (1)

- Rehman 2012Document8 pagesRehman 2012AisyahNo ratings yet

- 3 - A Form of Financial IntermediariesDocument7 pages3 - A Form of Financial IntermediariesTaha Wael QandeelNo ratings yet

- CFS Cbse Question BankDocument8 pagesCFS Cbse Question BankAgastya KarnwalNo ratings yet

- (Template) Prelim Fabm1Document3 pages(Template) Prelim Fabm1Christine Yarso TabloNo ratings yet

- Company Law LecturesDocument48 pagesCompany Law Lecturesimdad1986No ratings yet

- RatioDocument20 pagesRatioAkashdeep MarwahaNo ratings yet

- Yasin Acconting AssignmentDocument10 pagesYasin Acconting Assignmentkedir SeidNo ratings yet

- 1-Introduction To Financial StatementsDocument95 pages1-Introduction To Financial Statementstibip12345100% (3)

- APLN - Report Audit 2019Document142 pagesAPLN - Report Audit 2019Jefri Formen PangaribuanNo ratings yet

- Barth Etal The Relevance of The Value Relevance AnotherviewDocument28 pagesBarth Etal The Relevance of The Value Relevance AnotherviewMaz ShuliztNo ratings yet

- A Comparison of IFRS, US GAAP and Belgian GAAPDocument100 pagesA Comparison of IFRS, US GAAP and Belgian GAAPVoicu Dragomir67% (3)

- Introduction To Business FinanceDocument14 pagesIntroduction To Business Financesohail janNo ratings yet

- Merger and Acquisition in India: A Dissertation Report OnDocument43 pagesMerger and Acquisition in India: A Dissertation Report OnShehbaz ShaikhNo ratings yet

- Faq FlaDocument8 pagesFaq Flaumang24No ratings yet

- Level 1 - Financial StatementDocument11 pagesLevel 1 - Financial StatementVimmi BanuNo ratings yet

- Lesson 2 - The Accounting Information Systems Chapter 03Document74 pagesLesson 2 - The Accounting Information Systems Chapter 03Ismadth2918388No ratings yet

- Winter Issue of The Dirt 2022-23Document33 pagesWinter Issue of The Dirt 2022-23Vermont Nursery & Landscape AssociationNo ratings yet

- Balabac Executive Summary 2022Document5 pagesBalabac Executive Summary 2022Gray XoxoNo ratings yet