You might also like

- Nike Media PlanDocument21 pagesNike Media Planapi-562312644100% (1)

- Marketing Plan of PEPSIDocument24 pagesMarketing Plan of PEPSIm_bilal_2577% (31)

- 100 Copywriting TipsDocument58 pages100 Copywriting TipsHelen Harrison100% (7)

- Leading in Innovation: A CAPSIM Simulation ReportDocument10 pagesLeading in Innovation: A CAPSIM Simulation ReportPubgGamingNo ratings yet

- Sun Pharma Initiating Coverage Report - AMSECDocument38 pagesSun Pharma Initiating Coverage Report - AMSECkbn errNo ratings yet

- OTT Industry AnalysisDocument32 pagesOTT Industry AnalysisRohit Raj100% (1)

- Reviving Levi's Brand ImageDocument6 pagesReviving Levi's Brand ImageFlori May CasakitNo ratings yet

- Case Study-Apollo HospDocument36 pagesCase Study-Apollo HospGrim ReaperNo ratings yet

- Consumer Behavior Assesment of A Local Company (MR Bean)Document54 pagesConsumer Behavior Assesment of A Local Company (MR Bean)Damian100% (3)

- Gati LimitedDocument30 pagesGati Limitedthundercoder9288No ratings yet

- EdgeReport BALKRISIND CaseStudy 17 03 2022 682Document35 pagesEdgeReport BALKRISIND CaseStudy 17 03 2022 682Im CandlestickNo ratings yet

- Jubilant Food Stock Report PDFDocument33 pagesJubilant Food Stock Report PDFPranav WarneNo ratings yet

- EdgeReport RELAXO CaseStudy 14 01 2022 450Document34 pagesEdgeReport RELAXO CaseStudy 14 01 2022 450Im CandlestickNo ratings yet

- Persistent Sys Case StudyDocument34 pagesPersistent Sys Case StudyGrim ReaperNo ratings yet

- Britannia Case StudyDocument34 pagesBritannia Case StudyGrim ReaperNo ratings yet

- EdgeReport PAGEIND CaseStudy 20 09 2022 1048Document35 pagesEdgeReport PAGEIND CaseStudy 20 09 2022 1048aadil suhailNo ratings yet

- EdgeReport BRITANNIA CaseStudy 07 09 2022 994Document34 pagesEdgeReport BRITANNIA CaseStudy 07 09 2022 994aadil suhailNo ratings yet

- Indiamart Case StudyDocument35 pagesIndiamart Case StudyGrim ReaperNo ratings yet

- HDFC AMC Case Study AnalysisDocument34 pagesHDFC AMC Case Study AnalysisGrim ReaperNo ratings yet

- EdgeReport BALKRISIND CaseStudy 22-11-2022 240Document34 pagesEdgeReport BALKRISIND CaseStudy 22-11-2022 240malayalamedits100No ratings yet

- Col Pal Case StudyDocument34 pagesCol Pal Case StudyGrim ReaperNo ratings yet

- Case Study Cera SanitDocument34 pagesCase Study Cera SanitGrim ReaperNo ratings yet

- EdgeReport NILKAMAL CaseStudy 13 01 2022 348Document34 pagesEdgeReport NILKAMAL CaseStudy 13 01 2022 348Im CandlestickNo ratings yet

- Balrampur Chini Mills Limited: Case StudyDocument33 pagesBalrampur Chini Mills Limited: Case StudyAmitabh VatsyaNo ratings yet

- EdgeReport WIPRO CaseStudy 12 07 2022 1058Document35 pagesEdgeReport WIPRO CaseStudy 12 07 2022 1058skumar412898No ratings yet

- BalrampurChinni CaseStudy StockEdge 2010628Document34 pagesBalrampurChinni CaseStudy StockEdge 2010628Sureshbabu LakshminarayananNo ratings yet

- EdgeReport AFFLE CaseStudy 23 12 2022 883Document36 pagesEdgeReport AFFLE CaseStudy 23 12 2022 883amsukdNo ratings yet

- EdgeReport WIPRO CaseStudy 28 12 2022 444Document35 pagesEdgeReport WIPRO CaseStudy 28 12 2022 444gann wolfNo ratings yet

- ABBOTT INDIA LTD Centrum 0620 QTR Update 020920 Growing Amid LockdownDocument12 pagesABBOTT INDIA LTD Centrum 0620 QTR Update 020920 Growing Amid LockdownShanti RanganNo ratings yet

- Geogit BNP Paribus PDFDocument5 pagesGeogit BNP Paribus PDFBook MonkNo ratings yet

- EdgeReport AFFLE CaseStudyDocument36 pagesEdgeReport AFFLE CaseStudySandyNo ratings yet

- Glenmark Pharmaceuticals Limited_Investor Presentation_Q3 FY24Document19 pagesGlenmark Pharmaceuticals Limited_Investor Presentation_Q3 FY24SHREYA NAIRNo ratings yet

- Dabur: Weak Performance, Share Gain Continues ReduceDocument13 pagesDabur: Weak Performance, Share Gain Continues ReduceBook MonkNo ratings yet

- Arfy2021 22Document208 pagesArfy2021 22MAHI LADNo ratings yet

- Ajanta Annual Report FY22Document208 pagesAjanta Annual Report FY22MAHI LADNo ratings yet

- 1182311122021672glenmark Pharma Q2FY22Document5 pages1182311122021672glenmark Pharma Q2FY22Prajwal JainNo ratings yet

- PI Industries LTD - Q1FY23 Result Update - 10082022 - 10!08!2022 - 13Document8 pagesPI Industries LTD - Q1FY23 Result Update - 10082022 - 10!08!2022 - 13SandeepNo ratings yet

- EdgeReport TATAELXSI CaseStudy 10 04 2023 417Document34 pagesEdgeReport TATAELXSI CaseStudy 10 04 2023 417Department of power MIS CellNo ratings yet

- Nirmal Bang PDFDocument11 pagesNirmal Bang PDFBook MonkNo ratings yet

- Dabur India LTD: CMP: Rs 492 Rating: HOLD Target Price: Rs 515Document4 pagesDabur India LTD: CMP: Rs 492 Rating: HOLD Target Price: Rs 515Book MonkNo ratings yet

- EdgeReport WIPRO CaseStudy 27 12 2021 1037Document35 pagesEdgeReport WIPRO CaseStudy 27 12 2021 1037Im CandlestickNo ratings yet

- EdgeReport JUBLFOOD CaseStudy 03 11 2022 775Document36 pagesEdgeReport JUBLFOOD CaseStudy 03 11 2022 775aadil suhailNo ratings yet

- P5Document43 pagesP5Abhishek PandeyNo ratings yet

- Maquarie Mankind Pharma Initiation by Dr. Kunal DhameshaDocument35 pagesMaquarie Mankind Pharma Initiation by Dr. Kunal Dhameshalong-shortNo ratings yet

- Exide LTD Market Impact Q1FY19Document2 pagesExide LTD Market Impact Q1FY19Shihab MonNo ratings yet

- Hartalega Financial Performance AnalysisDocument18 pagesHartalega Financial Performance AnalysisfalinaNo ratings yet

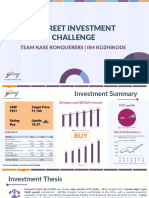

- R-STREET INVESTMENT CHALLENGE - BUY GODREJ CONSUMER PRODUCTSDocument12 pagesR-STREET INVESTMENT CHALLENGE - BUY GODREJ CONSUMER PRODUCTSApoorva JainNo ratings yet

- DairyDocument12 pagesDairyHimanshu SoniNo ratings yet

- Dabur India LTD PDFDocument8 pagesDabur India LTD PDFBook MonkNo ratings yet

- SPIL-IR-Presentation-Jan-2024-INR-1Document60 pagesSPIL-IR-Presentation-Jan-2024-INR-1SHREYA NAIRNo ratings yet

- United Spirits: Inflationary Pressures Darken Near-Term Outlook Retaining A HoldDocument6 pagesUnited Spirits: Inflationary Pressures Darken Near-Term Outlook Retaining A HoldSatya JagadishNo ratings yet

- Annual Report2017 MARICODocument318 pagesAnnual Report2017 MARICOmiaujNo ratings yet

- SPIL-IR-Presentation-March-2024-INRDocument60 pagesSPIL-IR-Presentation-March-2024-INRSHREYA NAIRNo ratings yet

- Indag Rubber Note Jan20 2016Document5 pagesIndag Rubber Note Jan20 2016doodledeeNo ratings yet

- Term Paper: HartalegaDocument18 pagesTerm Paper: HartalegafalinaNo ratings yet

- Glaxosmithkline Pharmaceuticals LTD: Revenue De-GrowthDocument7 pagesGlaxosmithkline Pharmaceuticals LTD: Revenue De-GrowthGuarachandar ChandNo ratings yet

- Middle East Working Capital Study 2023Document21 pagesMiddle East Working Capital Study 2023alhadipress3No ratings yet

- ICICI Securities Amul FY21 Annual Report UpdateDocument13 pagesICICI Securities Amul FY21 Annual Report UpdateMohitNo ratings yet

- Deepak Nitrate Research NotesDocument11 pagesDeepak Nitrate Research NotesJagan MohanNo ratings yet

- HSIE Results Daily - 04 August 21-202108040822126132901Document9 pagesHSIE Results Daily - 04 August 21-202108040822126132901Michelle CastelinoNo ratings yet

- Pija Doc 1581907800Document8 pagesPija Doc 1581907800lamp vicNo ratings yet

- Rali 23 7 20 PL PDFDocument8 pagesRali 23 7 20 PL PDFwhitenagarNo ratings yet

- ICICI - Piramal PharmaDocument4 pagesICICI - Piramal PharmasehgalgauravNo ratings yet

- Dabur India Outperforms on Rural Growth and Power BrandsDocument14 pagesDabur India Outperforms on Rural Growth and Power BrandsVishakha RathodNo ratings yet

- Equity Research Report Varun Beverages LTD 1700908867Document16 pagesEquity Research Report Varun Beverages LTD 1700908867Bazaar AajNo ratings yet

- Buy - ICICI Prudential Life Insurance - MOSL - 20.4.2021Document12 pagesBuy - ICICI Prudential Life Insurance - MOSL - 20.4.2021Roopa RoopavathyNo ratings yet

- Private Sector Operations in 2019: Report on Development EffectivenessFrom EverandPrivate Sector Operations in 2019: Report on Development EffectivenessNo ratings yet

- IP Q4FY21 FinalDocument54 pagesIP Q4FY21 FinalUdaya Vijay AnandNo ratings yet

- Hatsun Agro FoodsDocument134 pagesHatsun Agro FoodsUdaya Vijay AnandNo ratings yet

- BM Ia SL Sample OutlineDocument1 pageBM Ia SL Sample OutlineUdaya Vijay AnandNo ratings yet

- BM Ia Sample - Volkswagen PDFDocument16 pagesBM Ia Sample - Volkswagen PDFDiaffal David Halim NgNo ratings yet

- Anette VeidungDocument99 pagesAnette VeidungPrabhu PareekNo ratings yet

- PB BrochureDocument7 pagesPB BrochurePrabal Pratap SinghNo ratings yet

- Nielsen Beyond Clicks and ImpressionsDocument6 pagesNielsen Beyond Clicks and ImpressionsSy An NguyenNo ratings yet

- Evaluation Criteria For The Case Study Presentations: GROUP I - Cyworld: Creating and Capturing Value in A Social NetworkDocument3 pagesEvaluation Criteria For The Case Study Presentations: GROUP I - Cyworld: Creating and Capturing Value in A Social NetworkAshish KumarNo ratings yet

- Interpretations of Survey Results From Exhibit 1Document7 pagesInterpretations of Survey Results From Exhibit 1Tanya YadavNo ratings yet

- Gitanjali Amit MandalDocument2 pagesGitanjali Amit MandalAmit KumarNo ratings yet

- Era Gene: Gameintrogenie Group LTDDocument23 pagesEra Gene: Gameintrogenie Group LTDAna SilvaNo ratings yet

- Share 'Marketing Mix - Docx'Document8 pagesShare 'Marketing Mix - Docx'Albert ValezaNo ratings yet

- Zen App Pitch Deck Ver. 14 (Full Deck)Document34 pagesZen App Pitch Deck Ver. 14 (Full Deck)minh.scarletNo ratings yet

- 6 - Building A Brand SaturnDocument49 pages6 - Building A Brand SaturnFarhan AkhterNo ratings yet

- Halal Certi Cation Mark, Brand Quality, and Awareness Do They Influence Buying Decisions of Nigerian ConsumersDocument14 pagesHalal Certi Cation Mark, Brand Quality, and Awareness Do They Influence Buying Decisions of Nigerian ConsumersShinta Tri NurazizahNo ratings yet

- A Study On Effect of Welfare Measures On Employee MoraleDocument9 pagesA Study On Effect of Welfare Measures On Employee MoraleKeleti SanthoshNo ratings yet

- Marketing Presentation SlideDocument24 pagesMarketing Presentation SlideC harisseNo ratings yet

- Niche Marketing Club application insightsDocument3 pagesNiche Marketing Club application insightsMayuresh GaikarNo ratings yet

- Brand Building and Market Share Goals for Nike IndiaDocument3 pagesBrand Building and Market Share Goals for Nike IndiaDeepakdmimsNo ratings yet

- Spanish Dissertation TopicsDocument8 pagesSpanish Dissertation TopicsWritingPaperServicesToledo100% (1)

- Aimia Social Media White Paper 6 Types of Social Media UsersDocument22 pagesAimia Social Media White Paper 6 Types of Social Media UsersEuskaldunak100% (1)

- Assignement 4 Buyer Decision Process by Jeet ThakkarDocument5 pagesAssignement 4 Buyer Decision Process by Jeet ThakkarJeetNo ratings yet

- Promotion Stratergy of CadburyDocument81 pagesPromotion Stratergy of CadburyChaitanya SawantNo ratings yet

- UGC NET MOCK TEST PAPERDocument64 pagesUGC NET MOCK TEST PAPERBalaji_SAP100% (1)

- You Exec - Competitive Strategies CompleteDocument35 pagesYou Exec - Competitive Strategies CompletekylewfeeneyNo ratings yet

- Marketing AssignmentDocument19 pagesMarketing AssignmentHarshit PansariNo ratings yet

- A Study On The Marketing Strategies Adopted by E-Commerce Organizations To Induce Consumer Buying BehaviourDocument9 pagesA Study On The Marketing Strategies Adopted by E-Commerce Organizations To Induce Consumer Buying BehaviourarcherselevatorsNo ratings yet