You might also like

- World Bank Procurement Framework & Business OpportunitiesDocument25 pagesWorld Bank Procurement Framework & Business OpportunitiesM Faisal HanifNo ratings yet

- Arcus-Air-Brochure - 1 1 PDFDocument4 pagesArcus-Air-Brochure - 1 1 PDFSangeetha Krishnamurthy100% (2)

- Healthcare Data - Tracxn Business Model Report - 22 Sep 2020Document162 pagesHealthcare Data - Tracxn Business Model Report - 22 Sep 2020Gautam NatrajanNo ratings yet

- Document PDFDocument52 pagesDocument PDFMiguel Rivas20% (10)

- The 2022 ERP Report - Panorama Consulting GroupDocument43 pagesThe 2022 ERP Report - Panorama Consulting GroupMerouane AmraouiNo ratings yet

- Nutanix TN 2072 ESXi AHV Migration Version 2.2Document23 pagesNutanix TN 2072 ESXi AHV Migration Version 2.2Alejandro DariczNo ratings yet

- Hospital Information System FortisDocument76 pagesHospital Information System FortisAditya Varshneya100% (6)

- 2019 Global Shared Services Survey ResultsDocument24 pages2019 Global Shared Services Survey ResultskritikaNo ratings yet

- Rahul Raj MantooDocument15 pagesRahul Raj Mantooshakti4itNo ratings yet

- Paper Presentation Cloud Computing PDFDocument14 pagesPaper Presentation Cloud Computing PDFamphoen2528100% (3)

- Nidhi ResumeDocument3 pagesNidhi ResumeAnonymous laTL5eYR7mNo ratings yet

- EdgeReport WIPRO CaseStudy 28 12 2022 444Document35 pagesEdgeReport WIPRO CaseStudy 28 12 2022 444gann wolfNo ratings yet

- EdgeReport WIPRO CaseStudy 27 12 2021 1037Document35 pagesEdgeReport WIPRO CaseStudy 27 12 2021 1037Im CandlestickNo ratings yet

- Tata ElxsiDocument34 pagesTata Elxsijameelk786No ratings yet

- Persistent Sys Case StudyDocument34 pagesPersistent Sys Case StudyGrim ReaperNo ratings yet

- EdgeReport PAGEIND CaseStudy 20 09 2022 1048Document35 pagesEdgeReport PAGEIND CaseStudy 20 09 2022 1048aadil suhailNo ratings yet

- EdgeReport AFFLE CaseStudy 23 12 2022 883Document36 pagesEdgeReport AFFLE CaseStudy 23 12 2022 883amsukdNo ratings yet

- Dabur Case StudyDocument35 pagesDabur Case StudyUdaya Vijay AnandNo ratings yet

- Larsen & Toubro Limited: Case StudyDocument36 pagesLarsen & Toubro Limited: Case Studyarvind2431No ratings yet

- EdgeReport BALKRISIND CaseStudy 22-11-2022 240Document34 pagesEdgeReport BALKRISIND CaseStudy 22-11-2022 240malayalamedits100No ratings yet

- Outsourcing Review April 2020Document23 pagesOutsourcing Review April 2020Francisco Jose Fernandez MaldonadoNo ratings yet

- EdgeReport TATAELXSI CaseStudy 10 04 2023 417Document34 pagesEdgeReport TATAELXSI CaseStudy 10 04 2023 417Department of power MIS CellNo ratings yet

- EdgeReport BALKRISIND CaseStudy 17 03 2022 682Document35 pagesEdgeReport BALKRISIND CaseStudy 17 03 2022 682Im CandlestickNo ratings yet

- EdgeReport AFFLE CaseStudyDocument36 pagesEdgeReport AFFLE CaseStudySandyNo ratings yet

- Indiamart Case StudyDocument35 pagesIndiamart Case StudyGrim ReaperNo ratings yet

- Annual Report Imexhs 2022 1Document95 pagesAnnual Report Imexhs 2022 1Eduardo RodriguezNo ratings yet

- Capgemini - 2022-02-14 - FY21 Results Analyst PresentationDocument41 pagesCapgemini - 2022-02-14 - FY21 Results Analyst Presentationgsameera676No ratings yet

- MultiplesDocument49 pagesMultiplesDekov72No ratings yet

- Redington Final MSDocument15 pagesRedington Final MSkarthik sNo ratings yet

- Intergrated Annual ReportDocument15 pagesIntergrated Annual ReportAbdelhkim KechNo ratings yet

- FMS Delhi - Summer Placement Report 2022Document9 pagesFMS Delhi - Summer Placement Report 2022Ishant GuptaNo ratings yet

- PGP MAJVCG 2019-20 S3 Unrelated Diversification PDFDocument22 pagesPGP MAJVCG 2019-20 S3 Unrelated Diversification PDFBschool caseNo ratings yet

- Mirae Asset Hang Seng Technology ETF FundDocument8 pagesMirae Asset Hang Seng Technology ETF FundArmstrong CapitalNo ratings yet

- Fiche Technique FortinetDocument12 pagesFiche Technique FortinetHafide ZnNo ratings yet

- C&M ProjectDocument9 pagesC&M Projectaslam khanNo ratings yet

- Case Study Cera SanitDocument34 pagesCase Study Cera SanitGrim ReaperNo ratings yet

- HDFC AMC Case StudyDocument34 pagesHDFC AMC Case StudyGrim ReaperNo ratings yet

- EdgeReport RELAXO CaseStudy 14 01 2022 450Document34 pagesEdgeReport RELAXO CaseStudy 14 01 2022 450Im CandlestickNo ratings yet

- Corporate Presentation PDFDocument28 pagesCorporate Presentation PDFAnonymous WOiz9n8No ratings yet

- EdgeReport BRITANNIA CaseStudy 07 09 2022 994Document34 pagesEdgeReport BRITANNIA CaseStudy 07 09 2022 994aadil suhailNo ratings yet

- 2022 - CARE HEALTH INSURANCE - All Rights Reserved. - CONFIDENTIALDocument24 pages2022 - CARE HEALTH INSURANCE - All Rights Reserved. - CONFIDENTIALRohit ShekhawatNo ratings yet

- EdgeReport NILKAMAL CaseStudy 13 01 2022 348Document34 pagesEdgeReport NILKAMAL CaseStudy 13 01 2022 348Im CandlestickNo ratings yet

- Procurement Framework and Bidding Opportunities PresentationDocument25 pagesProcurement Framework and Bidding Opportunities PresentationvigneshatcubeNo ratings yet

- CFA Research Challenge PresentationDocument17 pagesCFA Research Challenge PresentationSebastian MorenoNo ratings yet

- Management Tools and TrendsDocument124 pagesManagement Tools and TrendsigangNo ratings yet

- D-Link (India) LTD: Retail ResearchDocument14 pagesD-Link (India) LTD: Retail ResearchDinesh ChoudharyNo ratings yet

- EdgeReport ULTRACEMCO CaseStudy 28 01 2022 160Document35 pagesEdgeReport ULTRACEMCO CaseStudy 28 01 2022 160Im CandlestickNo ratings yet

- Annual Report 2020 Full Version PDF 1Document161 pagesAnnual Report 2020 Full Version PDF 1pukis pukisNo ratings yet

- Merus LabsDocument20 pagesMerus LabsJenny QuachNo ratings yet

- State of AI in Africa ReportDocument19 pagesState of AI in Africa ReportDaniel BruintjiesNo ratings yet

- The SoDA Report On The Global Agency Landscape 2022Document41 pagesThe SoDA Report On The Global Agency Landscape 2022Alejandro DiMannoNo ratings yet

- 200case StudyDocument11 pages200case StudyRituraj ShekharNo ratings yet

- CXO Increments Survey 2023 ReportDocument12 pagesCXO Increments Survey 2023 Reportmarvel mNo ratings yet

- 2021 Procurement Key Issues: ALL Spend, ALL Suppliers, NO CompromisesDocument19 pages2021 Procurement Key Issues: ALL Spend, ALL Suppliers, NO CompromisesMarcos TobarNo ratings yet

- Deloitte Proposal - JSL - ESG Risk Assesment - De-Carbonization - 24feb2022Document80 pagesDeloitte Proposal - JSL - ESG Risk Assesment - De-Carbonization - 24feb2022mhemanthkumar2167No ratings yet

- Performance: Numerai's Relative Performance (Net of Costs and Fees)Document5 pagesPerformance: Numerai's Relative Performance (Net of Costs and Fees)Jagdeep MaviNo ratings yet

- April 2022Document43 pagesApril 2022Indraneel MahantiNo ratings yet

- IPoint Study Sustainability and Compliance Trends 2022Document26 pagesIPoint Study Sustainability and Compliance Trends 2022qmbkxy7k9cNo ratings yet

- Investment Research: Fundamental Coverage - 3M India LimitedDocument8 pagesInvestment Research: Fundamental Coverage - 3M India Limitedrchawdhry123No ratings yet

- Exide LTD Market Impact Q1FY19Document2 pagesExide LTD Market Impact Q1FY19Shihab MonNo ratings yet

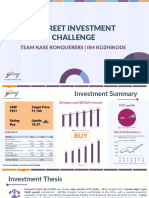

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- 2020 REPORT: Leveraging Technology To Optimize Your BusinessDocument39 pages2020 REPORT: Leveraging Technology To Optimize Your Business9980139892No ratings yet

- Nokia GRI Content Index 2019uuDocument16 pagesNokia GRI Content Index 2019uuLucas SloniakNo ratings yet

- Saratoga Investor Relation Presentation 9M19 Final - PublicDocument15 pagesSaratoga Investor Relation Presentation 9M19 Final - Publicsigitsutoko8765No ratings yet

- 2018 ERP ReportDocument40 pages2018 ERP ReportkhalideNo ratings yet

- Estimating the Job Creation Impact of Development AssistanceFrom EverandEstimating the Job Creation Impact of Development AssistanceNo ratings yet

- Private Sector Operations in 2019: Report on Development EffectivenessFrom EverandPrivate Sector Operations in 2019: Report on Development EffectivenessNo ratings yet

- The Internet of Things and Industry 4.0: Adam Drobot Opentechworks, Inc. Wayne, Pa UsaDocument46 pagesThe Internet of Things and Industry 4.0: Adam Drobot Opentechworks, Inc. Wayne, Pa Usaimah pinterNo ratings yet

- Cloud Telephony EbookDocument33 pagesCloud Telephony EbookSangram SabatNo ratings yet

- AAI Automation 360Document51 pagesAAI Automation 360Martiniano MallavibarrenaNo ratings yet

- Zscaler Q3-23 Corporate PresentationDocument40 pagesZscaler Q3-23 Corporate Presentationjoshka musicNo ratings yet

- OpenStack 101 Modular Deck 1Document20 pagesOpenStack 101 Modular Deck 1zero oneNo ratings yet

- The Ultimate Guide To Data IntegrationDocument48 pagesThe Ultimate Guide To Data Integrationvr.sf99No ratings yet

- Hemanth Kumar S - DSUDocument1 pageHemanth Kumar S - DSUHemanth Kumar S ENG19CS0120No ratings yet

- Microsoft BizTalk Server 2020 - Licensing DatasheetDocument2 pagesMicrosoft BizTalk Server 2020 - Licensing DatasheetAlexandru CojocaruNo ratings yet

- Authors BookDocument180 pagesAuthors BookMaria DialNo ratings yet

- Journal of Business Research: Joel Mero, Miira Leinonen, Hannu Makkonen, Heikki KarjaluotoDocument12 pagesJournal of Business Research: Joel Mero, Miira Leinonen, Hannu Makkonen, Heikki KarjaluotoMuhammad AqsaNo ratings yet

- Smart Water Monitoring and Distribution System Based On IOTDocument5 pagesSmart Water Monitoring and Distribution System Based On IOTSudeep UpadhyeNo ratings yet

- Sign Language Recognition Using Smart GloveDocument4 pagesSign Language Recognition Using Smart Gloveiot forumNo ratings yet

- AWS Certified Solutions Architect Associate Training IpsrDocument8 pagesAWS Certified Solutions Architect Associate Training Ipsrriya vargheseNo ratings yet

- Best Practices Secure Cloud Migration WP - 537230 - 617126Document12 pagesBest Practices Secure Cloud Migration WP - 537230 - 617126Mircea MurguNo ratings yet

- Use Local VNC Viewer To Access Guest VM Console (Honglin Su - Building Open Cloud Infrastructure)Document5 pagesUse Local VNC Viewer To Access Guest VM Console (Honglin Su - Building Open Cloud Infrastructure)Tolulope AbiodunNo ratings yet

- MPJ Express: An Implementation of MPI in Java: Linux/UNIX/Mac User GuideDocument23 pagesMPJ Express: An Implementation of MPI in Java: Linux/UNIX/Mac User GuideSwapnil ShindeNo ratings yet

- Big Data For Managers: Assignment 1Document8 pagesBig Data For Managers: Assignment 1Aman SandalNo ratings yet

- Full Download Book CCSP Certified Cloud Security Professional All in One Exam Guide 2 PDFDocument33 pagesFull Download Book CCSP Certified Cloud Security Professional All in One Exam Guide 2 PDFerik.clements895100% (16)

- Telestream Vantage Integration With Aspera FASPDocument2 pagesTelestream Vantage Integration With Aspera FASPrberrospiNo ratings yet

- Cloud Computing Unit-3Document34 pagesCloud Computing Unit-3Akshath Kumar100% (1)

- Enhanced Secure Data Sharing Over Cloud Using ABE AlgorithmDocument4 pagesEnhanced Secure Data Sharing Over Cloud Using ABE Algorithmcyan whiteNo ratings yet

- Privacy Protection Based Access Control Scheme in Cloud-Based Services - 1crore ProjectsDocument5 pagesPrivacy Protection Based Access Control Scheme in Cloud-Based Services - 1crore ProjectsLalitha PonnamNo ratings yet

- ISACA CISA v2022-10-07 q117Document29 pagesISACA CISA v2022-10-07 q117Godfrey MakurumureNo ratings yet