You might also like

- Eric C. Blue Criminal Record New Orleans 2Document1 pageEric C. Blue Criminal Record New Orleans 2Eric GreenNo ratings yet

- Ilm - 2d Maw Loa Final SignedDocument6 pagesIlm - 2d Maw Loa Final SignedMichael JamesNo ratings yet

- American Rescue Plan Six Month ReportDocument8 pagesAmerican Rescue Plan Six Month ReportJoecippNo ratings yet

- Hanergy Report PDFDocument42 pagesHanergy Report PDFViviana Newman100% (2)

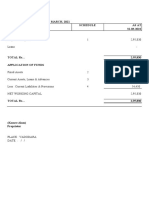

- Lichello A.I.M. ImprovementsDocument8 pagesLichello A.I.M. Improvementsd1234dNo ratings yet

- July 7th Negotiation PresentationDocument100 pagesJuly 7th Negotiation PresentationDan Trotter BN9No ratings yet

- 101 Eric C. Blue Creditor MatrixDocument4 pages101 Eric C. Blue Creditor MatrixEric GreenNo ratings yet

- California Department of Health Care Services Stipulation Regarding Arlington Recovery Community and Sobering CenterDocument8 pagesCalifornia Department of Health Care Services Stipulation Regarding Arlington Recovery Community and Sobering CenterThe Press-Enterprise / pressenterprise.comNo ratings yet

- 2016 UCPB Annual Report UpdatedDocument236 pages2016 UCPB Annual Report UpdatedPat Dela CruzNo ratings yet

- 294 Riya RanaDocument4 pages294 Riya RanaRiya RanaNo ratings yet

- FERC 10.19.22 LTR With FWS Comments From 10.4.22Document19 pagesFERC 10.19.22 LTR With FWS Comments From 10.4.22jonsokolowNo ratings yet

- 3 Symbiosis Law School, Hyderabad, National Moot Court Competition-2018Document32 pages3 Symbiosis Law School, Hyderabad, National Moot Court Competition-2018Amiya Bhushan SharmaNo ratings yet

- Coalition On Homlessness V City and County of San Francisco 2008 Opposition To TRODocument5 pagesCoalition On Homlessness V City and County of San Francisco 2008 Opposition To TROauweia1100% (1)

- 13-09-2022 - AC Quote - Oftog Bussiness Solutions (OP-1)Document8 pages13-09-2022 - AC Quote - Oftog Bussiness Solutions (OP-1)Dausori SatishNo ratings yet

- Gfresort0119@yahoo - Co,: ABC Shopping Complex, Rizal Street, Old Albay District, Legazpi City, Albay 4500Document862 pagesGfresort0119@yahoo - Co,: ABC Shopping Complex, Rizal Street, Old Albay District, Legazpi City, Albay 4500Aces SalvadorNo ratings yet

- Duke Realty RezoningDocument79 pagesDuke Realty RezoningZachary HansenNo ratings yet

- Ohio ACLU & LWV Congressional Map LawsuitDocument45 pagesOhio ACLU & LWV Congressional Map LawsuitWKYC.comNo ratings yet

- Court - Ruling DOF Case $25MMDocument8 pagesCourt - Ruling DOF Case $25MMKaitlynSchallhornNo ratings yet

- Disclosure No. 761 2022 Audited Financial Statements As of December 31 2021Document160 pagesDisclosure No. 761 2022 Audited Financial Statements As of December 31 2021Apriljohn OlingayNo ratings yet

- Eric C. Blue Criminal Record New Orleans 1Document1 pageEric C. Blue Criminal Record New Orleans 1Eric GreenNo ratings yet

- Savage Rail Tooele STB FilingDocument14 pagesSavage Rail Tooele STB FilingThe Salt Lake TribuneNo ratings yet

- Kentucky Court of Appeals: 2022-CA-780-OADocument20 pagesKentucky Court of Appeals: 2022-CA-780-OAChrisNo ratings yet

- DevelopmentVol II19 202 PDFDocument619 pagesDevelopmentVol II19 202 PDFTIPUNo ratings yet

- NVDA F1Q23 Investor Presentation FINALDocument49 pagesNVDA F1Q23 Investor Presentation FINALTanjim RahmanNo ratings yet

- Kirk Fulford - AASB PresentationDocument33 pagesKirk Fulford - AASB PresentationTrisha Powell CrainNo ratings yet

- Supplemental Type Certificate: Department of Transportation Federal Aviation AdministrationDocument3 pagesSupplemental Type Certificate: Department of Transportation Federal Aviation AdministrationFlorian SteixnerNo ratings yet

- CM-760434-draft Complaint 12.14.19Document2 pagesCM-760434-draft Complaint 12.14.19Jon FriedNo ratings yet

- Adobe Scan Aug 11, 2022Document6 pagesAdobe Scan Aug 11, 2022Tausif HussainNo ratings yet

- PEER On MDOCDocument93 pagesPEER On MDOCRuss LatinoNo ratings yet

- Automatic License Plate Readers Quote For City of Marco Island - 2020Document2 pagesAutomatic License Plate Readers Quote For City of Marco Island - 2020Omar Rodriguez OrtizNo ratings yet

- Annual Transfers ATM Dte - 2022Document52 pagesAnnual Transfers ATM Dte - 2022Pavan GopalapuramNo ratings yet

- Olympus Pools Florida AG FillingDocument9 pagesOlympus Pools Florida AG FillingABC Action NewsNo ratings yet

- Lumber Duty DepositsDocument10 pagesLumber Duty DepositsForexliveNo ratings yet

- Public Infrastructure Construction Jobs in The Central ValleyDocument2 pagesPublic Infrastructure Construction Jobs in The Central ValleyMelissa MontalvoNo ratings yet

- Penawaran Grabtaxi-BillboardDocument18 pagesPenawaran Grabtaxi-BillboardheryNo ratings yet

- Spreadsheet TutorialDocument106 pagesSpreadsheet Tutorialankitp219No ratings yet

- Annual Credit Report Request Form: Social Security Number: Date of BirthDocument1 pageAnnual Credit Report Request Form: Social Security Number: Date of BirthPendi AgarwalNo ratings yet

- Green Bay Professional Police Ass'n v. City of Green BayDocument2 pagesGreen Bay Professional Police Ass'n v. City of Green BayFOX 11 NewsNo ratings yet

- Big Sky Network v. Sichuan Provincial, 533 F.3d 1183, 10th Cir. (2008)Document21 pagesBig Sky Network v. Sichuan Provincial, 533 F.3d 1183, 10th Cir. (2008)Scribd Government DocsNo ratings yet

- United States Court of Appeals, First CircuitDocument5 pagesUnited States Court of Appeals, First CircuitScribd Government DocsNo ratings yet

- DayanandhDocument2 pagesDayanandhMK gamingNo ratings yet

- Tri Colored BatDocument3 pagesTri Colored BatjonsokolowNo ratings yet

- Analysis of Key Factors Affecting The Variation of Labour Productivity in Construction ProjectsDocument9 pagesAnalysis of Key Factors Affecting The Variation of Labour Productivity in Construction ProjectsJohn AjishNo ratings yet

- Tejas Motel, L.L.C. v. City of Mesquite, No. 22-10321 (5th Cir. Mar. 22, 2023)Document18 pagesTejas Motel, L.L.C. v. City of Mesquite, No. 22-10321 (5th Cir. Mar. 22, 2023)RHTNo ratings yet

- Danny Rolling - Brief of Appellant by Supreme Court of Florida, January 22, 1996Document263 pagesDanny Rolling - Brief of Appellant by Supreme Court of Florida, January 22, 1996Erin Banks100% (1)

- FRC DRAFT Meeting Minutes 3-14-2023Document3 pagesFRC DRAFT Meeting Minutes 3-14-2023Pat PowersNo ratings yet

- Final BookDocument196 pagesFinal BookRuhiNo ratings yet

- Scott Spivey's Estate Files Wrongful Death LawsuitDocument12 pagesScott Spivey's Estate Files Wrongful Death LawsuitKristin100% (1)

- Question 686785 1Document11 pagesQuestion 686785 1rishu53840% (1)

- Full BusinessDocument96 pagesFull Businessh.zaidi569No ratings yet

- 45-1 Ex. A COMPLAINTDocument100 pages45-1 Ex. A COMPLAINTlarry-612445No ratings yet

- Billing Statement: Payoff Progress Current Payment Breakdown PaynearmeDocument4 pagesBilling Statement: Payoff Progress Current Payment Breakdown PaynearmeGabriel B Mendonca100% (1)

- Georgia Power Company v. Charles F. Baker, 830 F.2d 163, 11th Cir. (1987)Document9 pagesGeorgia Power Company v. Charles F. Baker, 830 F.2d 163, 11th Cir. (1987)Scribd Government DocsNo ratings yet

- Kelley ComplaintDocument10 pagesKelley ComplaintThe Salt Lake TribuneNo ratings yet

- Dekkers RedactedDocument4 pagesDekkers RedactedGazetteonlineNo ratings yet

- Caso de Casey David Crowther. FloridaDocument9 pagesCaso de Casey David Crowther. FloridaDiario Las AméricasNo ratings yet

- Capital Budgeting Challenger SeriesDocument17 pagesCapital Budgeting Challenger SeriesDeepsikha maitiNo ratings yet

- SFM Answer 2Document13 pagesSFM Answer 2riyaNo ratings yet

- Ii Semester Endterm Examination March 2016Document2 pagesIi Semester Endterm Examination March 2016Nithyananda PatelNo ratings yet

- 8 RTP Nov 21 1Document27 pages8 RTP Nov 21 1Bharath Krishna MVNo ratings yet

- Bangalore University Previous Year Question Paper AFM 2020Document3 pagesBangalore University Previous Year Question Paper AFM 2020Ramakrishna NagarajaNo ratings yet

- Kamre Aalam Balance Sheet - March-2022Document4 pagesKamre Aalam Balance Sheet - March-2022Parth KachhiyaNo ratings yet

- Kamre Aalam ITR-V - March-2022Document1 pageKamre Aalam ITR-V - March-2022Parth KachhiyaNo ratings yet

- Sbec Part B FinalDocument64 pagesSbec Part B FinalParth KachhiyaNo ratings yet

- Revised ITR-VDocument1 pageRevised ITR-VParth KachhiyaNo ratings yet

- JIGL Chapter 1 Analysis Sheet Dec'2022Document1 pageJIGL Chapter 1 Analysis Sheet Dec'2022Parth KachhiyaNo ratings yet

- Executive Reg LetterDocument8 pagesExecutive Reg LetterParth KachhiyaNo ratings yet

- Solution Manual For Financial Institutions Managementa Risk Management Approach Saunders Cornett 8th EditionDocument17 pagesSolution Manual For Financial Institutions Managementa Risk Management Approach Saunders Cornett 8th EditionAmandaMartinxdwj100% (41)

- DOS Circular No. 01: Provision Against Investment in Listed and Non-Listed Share, Bond/debenture and Mutual FundDocument4 pagesDOS Circular No. 01: Provision Against Investment in Listed and Non-Listed Share, Bond/debenture and Mutual Fundsoyiga8199No ratings yet

- Role of Institutional Investors in Corporate GovernanceDocument17 pagesRole of Institutional Investors in Corporate GovernanceRaj KumarNo ratings yet

- Multiple Bank Accounts Registration FormDocument2 pagesMultiple Bank Accounts Registration FormgoutamNo ratings yet

- DSP BR Common Application FormDocument42 pagesDSP BR Common Application Formrkdgr87880No ratings yet

- Smart Investment (E-Copy) Vol 15 Issue No. 48 (8th January 2023)Document82 pagesSmart Investment (E-Copy) Vol 15 Issue No. 48 (8th January 2023)Keshav KhetanNo ratings yet

- RHP ClarisDocument423 pagesRHP ClarisSharmila RaniNo ratings yet

- Project Report ON "Customer Satisfaction Regarding HDFC Bank"Document63 pagesProject Report ON "Customer Satisfaction Regarding HDFC Bank"BHARATNo ratings yet

- Sarthak Tikam Imf Tybaf Full ProjectDocument63 pagesSarthak Tikam Imf Tybaf Full ProjectShivansh AgrahariNo ratings yet

- AMC Sector - HDFC Sec-201901111558114702001 PDFDocument99 pagesAMC Sector - HDFC Sec-201901111558114702001 PDFmonikkapadiaNo ratings yet

- ICICI Securities Limited Annual Report FY2020 21Document255 pagesICICI Securities Limited Annual Report FY2020 21Avengers HeroesNo ratings yet

- A Study On Mutual Funds in IndiaDocument32 pagesA Study On Mutual Funds in IndiaAbhranil DasNo ratings yet

- XXXXX MFDocument24 pagesXXXXX MFpratik0909No ratings yet

- Investment Decision Making Pattern of Investors...Document123 pagesInvestment Decision Making Pattern of Investors...Rijabul Talukdar63% (8)

- BCFM ModuleDocument253 pagesBCFM ModuledbankwalaNo ratings yet

- Varun Beverages Q1CY22 Result UpdateDocument5 pagesVarun Beverages Q1CY22 Result UpdateBaria VirenNo ratings yet

- A Study On Various Investment Options in IndiaDocument169 pagesA Study On Various Investment Options in IndiaLeena NaikNo ratings yet

- FRM Learning Objectives 2023Document58 pagesFRM Learning Objectives 2023Tejas JoshiNo ratings yet

- Reforms in Capital MarketDocument22 pagesReforms in Capital MarketJitendra KalwaniNo ratings yet

- Manikanta Doki 1486 - IRDocument50 pagesManikanta Doki 1486 - IRNawazish KhanNo ratings yet

- BUS 505.assignmentDocument16 pagesBUS 505.assignmentRashìd RanaNo ratings yet

- Nivetha.V 531900782 ProjectDocument73 pagesNivetha.V 531900782 ProjectDeepuNo ratings yet

- FRI AssignmentDocument18 pagesFRI AssignmentHaider SaleemNo ratings yet

- Project On MFDocument5 pagesProject On MFSahil MakkarNo ratings yet

- Safekeeping of Valuables and Certification of Value: Rose - Chapter 01 #1Document20 pagesSafekeeping of Valuables and Certification of Value: Rose - Chapter 01 #1Lê Chấn PhongNo ratings yet

- The Unit Trust of IndiaDocument2 pagesThe Unit Trust of Indiakhageswarsingh865No ratings yet

- Interview Questions and AnswersDocument7 pagesInterview Questions and AnswersAsif JavaidNo ratings yet

- Ishika Jain 2021346 PDFDocument59 pagesIshika Jain 2021346 PDFsanu duttaNo ratings yet

- Mera Funds Newsletter October 2022Document11 pagesMera Funds Newsletter October 2022Prasanna ShenoyNo ratings yet