You might also like

- Hind Oil Case Study SolutionDocument11 pagesHind Oil Case Study SolutionVineel Kumar80% (5)

- Income Tax Return Sat-Ita22: Official StampDocument6 pagesIncome Tax Return Sat-Ita22: Official Stamptsere butsere50% (2)

- Fundamentals of Internal Auditing PDFDocument113 pagesFundamentals of Internal Auditing PDFCarla Jean Cuyos100% (1)

- Swot Analysis Korean RestaurantDocument4 pagesSwot Analysis Korean RestaurantIzzatul KamilaNo ratings yet

- A Consultative Approach To AuditingDocument24 pagesA Consultative Approach To AuditingWafaa Safaei TolamiNo ratings yet

- Case AlvisDocument1 pageCase AlvisRicha MathewsNo ratings yet

- Loan AgreementDocument5 pagesLoan AgreementAnthony MalungaNo ratings yet

- Factsheet - Internal Audit ConsultingDocument2 pagesFactsheet - Internal Audit ConsultingDejan PericNo ratings yet

- CH 15 PDFDocument7 pagesCH 15 PDFYohanaNo ratings yet

- Chapter 2Document17 pagesChapter 2Cristina RamirezNo ratings yet

- Managing The IAFDocument34 pagesManaging The IAFhziqhshahNo ratings yet

- POA - Unit 2 - v2Document10 pagesPOA - Unit 2 - v2Ari SyahputraNo ratings yet

- Internal Audit As A Trusted Advisor 1669192593Document2 pagesInternal Audit As A Trusted Advisor 1669192593mohamedNo ratings yet

- 28.5 Expanded Internal Audit Services To ManagementDocument1 page28.5 Expanded Internal Audit Services To ManagementMuhammad TenriNo ratings yet

- Week 10 11 12 - Project Management FundamentalsDocument54 pagesWeek 10 11 12 - Project Management Fundamentals7 daysNo ratings yet

- Benefits and Best Practices of Management Consulting by Laith TseganoffDocument57 pagesBenefits and Best Practices of Management Consulting by Laith Tseganoffsaikumar selaNo ratings yet

- Foundation S of Internal AuditDocument4 pagesFoundation S of Internal AuditS4M1Y4No ratings yet

- Lean Auditing PDFDocument2 pagesLean Auditing PDFasdasfNo ratings yet

- Us Advisory Agile Internal Audit Part1 Introduction To Elevating PerformanceDocument10 pagesUs Advisory Agile Internal Audit Part1 Introduction To Elevating PerformancecvacaNo ratings yet

- Topic 1Document65 pagesTopic 1Carl Dhaniel Garcia SalenNo ratings yet

- Chapter 1 - Introduction To Internal AuditingDocument21 pagesChapter 1 - Introduction To Internal AuditingIndah arum sariNo ratings yet

- 2019-IAWebinar Course5 Agile FINAL 111919Document37 pages2019-IAWebinar Course5 Agile FINAL 111919Jennie LimNo ratings yet

- CIA Part 1, Unit 1-1Document35 pagesCIA Part 1, Unit 1-1Ahmed AzaziNo ratings yet

- Red Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaDocument78 pagesRed Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaАндрей МиксоновNo ratings yet

- CIA Part 1 AUD1201 IAE 1Document5 pagesCIA Part 1 AUD1201 IAE 1gerezkarla13No ratings yet

- Deloitte ES GRC Agile Internal AuditDocument12 pagesDeloitte ES GRC Agile Internal AuditPatricio Cuadra LizamaNo ratings yet

- Problem & Solutions - ProgressDocument23 pagesProblem & Solutions - ProgressAkbar Yoga PrastyaNo ratings yet

- Harnessing The Full Potential of Internal Audit: To Protect and EnhanceDocument12 pagesHarnessing The Full Potential of Internal Audit: To Protect and EnhanceAlya Khaira NazhifaNo ratings yet

- Internal Audit in The Dynamic WorldDocument165 pagesInternal Audit in The Dynamic Worldkhuzaimaaziz18No ratings yet

- WBS Management Advancement Programme 2023Document24 pagesWBS Management Advancement Programme 2023MKmahlako mahlakoNo ratings yet

- MK 324 Power Point Management Consulting CompleteDocument397 pagesMK 324 Power Point Management Consulting CompleteWILBROAD THEOBARDNo ratings yet

- Stracosman - Chapter 7Document2 pagesStracosman - Chapter 7Rae WorksNo ratings yet

- Case Study Managed ServicesDocument2 pagesCase Study Managed ServicesAshtangram jhaNo ratings yet

- Sprinting Ahead With Agile AuditingDocument24 pagesSprinting Ahead With Agile AuditingarfianNo ratings yet

- What Are The Benefits of Performance Measurement?Document12 pagesWhat Are The Benefits of Performance Measurement?LuisNo ratings yet

- Life As An Internal AuditorDocument44 pagesLife As An Internal AuditormmatiasNo ratings yet

- Scorecard WorkshopDocument61 pagesScorecard WorkshopKeemeNo ratings yet

- 2017-1170 QAL-Insights To Quality Q4-FINALDocument2 pages2017-1170 QAL-Insights To Quality Q4-FINALMerta WiramaNo ratings yet

- Tone at The Top June 2021Document4 pagesTone at The Top June 2021Well Durano CasasNo ratings yet

- Group 2 - Pyq - Managing IaDocument15 pagesGroup 2 - Pyq - Managing Iajaizah saimNo ratings yet

- Transformation in The Internal Audit Function: Neil WhiteDocument12 pagesTransformation in The Internal Audit Function: Neil WhiteAlexchandar Anbalagan100% (1)

- Peran Internal Auditor SBG Konsultan & Katalis V (1) .2Document25 pagesPeran Internal Auditor SBG Konsultan & Katalis V (1) .2Retno Triwahyuni ManullangNo ratings yet

- It Iia AustraliaDocument4 pagesIt Iia AustraliaAzaria KylaNo ratings yet

- Mod 4 P 1Document8 pagesMod 4 P 1Jison FrancisNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource Wasjaydee magalangNo ratings yet

- Internal Control, Internal Auditor & Risk ManagementDocument58 pagesInternal Control, Internal Auditor & Risk ManagementWagimin SendjajaNo ratings yet

- Engaging The Audit CommitteeDocument2 pagesEngaging The Audit Committeeabdul syukurNo ratings yet

- Chapter9ppt4thedition 240415081801 d7c7638cDocument43 pagesChapter9ppt4thedition 240415081801 d7c7638cPei LingNo ratings yet

- CIA Challenge Exam (Part 1)Document116 pagesCIA Challenge Exam (Part 1)JohnNo ratings yet

- Risk Management and Internal AuditorDocument58 pagesRisk Management and Internal AuditorAnanda rizky syifa nabilahNo ratings yet

- Z 09300000120164006 PP T 06Document36 pagesZ 09300000120164006 PP T 06TFI Student CommunityNo ratings yet

- ISQC1 Element 1-3 (Final)Document50 pagesISQC1 Element 1-3 (Final)Lee SuarezNo ratings yet

- Managing The Quality of Consulting EngagementsDocument32 pagesManaging The Quality of Consulting EngagementsCedric Legaspi TagalaNo ratings yet

- Factsheet: Internal Audit Benefits: Connect Support AdvanceDocument2 pagesFactsheet: Internal Audit Benefits: Connect Support AdvanceAsfa AsfiaNo ratings yet

- Internal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiaDocument86 pagesInternal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiacuixiNo ratings yet

- Case Study 3 Abridged v.3Document13 pagesCase Study 3 Abridged v.3رهف العاليNo ratings yet

- Management Consultancy - 9Document2 pagesManagement Consultancy - 9ardagrbwNo ratings yet

- Internal Audit StrategyDocument5 pagesInternal Audit StrategyRoberto Vega100% (1)

- Intro To Internal Auditing Ch. 1, 2, and 3 Flashcards - QuizletDocument5 pagesIntro To Internal Auditing Ch. 1, 2, and 3 Flashcards - QuizletIman NessaNo ratings yet

- CH02-Illustrative Solutions-V.4 - Pre-QuizDocument11 pagesCH02-Illustrative Solutions-V.4 - Pre-QuizBrandonNo ratings yet

- AI-X-S2-G5-Arief Budi NugrohoDocument3 pagesAI-X-S2-G5-Arief Budi Nugrohoariefmatani73No ratings yet

- Ula Chapter 1-23-28Document6 pagesUla Chapter 1-23-28queen awesomeNo ratings yet

- Internal Audit Report Types 1707298159Document3 pagesInternal Audit Report Types 1707298159khanjahan1955No ratings yet

- Agile Auditing - LanjutanDocument59 pagesAgile Auditing - LanjutanmuchtarNo ratings yet

- The Enterprise Business Analyst: Developing Creative Solutions to Complex Business ProblemsFrom EverandThe Enterprise Business Analyst: Developing Creative Solutions to Complex Business ProblemsNo ratings yet

- Proactive Fraud Audit, Whistleblowing and Cultural Implementation of Tri Hita Karana For Fraud PreventionDocument14 pagesProactive Fraud Audit, Whistleblowing and Cultural Implementation of Tri Hita Karana For Fraud PreventionIzzatul KamilaNo ratings yet

- Makalah Bhs Inggris BaruDocument10 pagesMakalah Bhs Inggris BaruIzzatul KamilaNo ratings yet

- Swot Analysis SlimeDocument8 pagesSwot Analysis SlimeIzzatul KamilaNo ratings yet

- SPNY - AR - 2009 (Bursa) Final PDFDocument147 pagesSPNY - AR - 2009 (Bursa) Final PDFEric Tan Chee KheongNo ratings yet

- Quiz Chap 1 - Modern Project ManagementDocument4 pagesQuiz Chap 1 - Modern Project ManagementNGÂN PHẠM NGỌC THẢONo ratings yet

- Ride Details Bill Details: Mohd Sabir AliDocument3 pagesRide Details Bill Details: Mohd Sabir AlidbtechkubeNo ratings yet

- CH 14Document4 pagesCH 14pablozhang1226No ratings yet

- CV RanjitDocument3 pagesCV RanjitIto LawputraNo ratings yet

- Chronic Care in IndiaDocument28 pagesChronic Care in IndiaVijaykumar Bojja100% (1)

- 9001 Audit Checklist-Production SupportDocument7 pages9001 Audit Checklist-Production SupportAmer RahmahNo ratings yet

- Tema 12 - Inglés para Los Negocios IDocument12 pagesTema 12 - Inglés para Los Negocios IKimberly Mendoza SalasNo ratings yet

- SchemesTap Old - January 2023 Lyst8174Document75 pagesSchemesTap Old - January 2023 Lyst8174Bhanu RaghavNo ratings yet

- DownloadDocument3 pagesDownloadChristina SalliNo ratings yet

- Add Power of Attorney: 1. Account Holder InformationDocument3 pagesAdd Power of Attorney: 1. Account Holder InformationDavid BuchananNo ratings yet

- IXP - Conclusions - Swazilnd - Document vr1Document6 pagesIXP - Conclusions - Swazilnd - Document vr1Linda DlaminiNo ratings yet

- CRM Short QuizDocument1 pageCRM Short QuizDaria Par-HughesNo ratings yet

- BIAPPS 7964 Config GuideDocument640 pagesBIAPPS 7964 Config GuidesathishNo ratings yet

- Soal Usbn B. Inggris 2020Document13 pagesSoal Usbn B. Inggris 2020atikah suhendar0% (1)

- Solution Manual For Microeconomics and Behavior 9th Edition Frank 0078021693 9780078021695Document36 pagesSolution Manual For Microeconomics and Behavior 9th Edition Frank 0078021693 9780078021695brianrobertsonogknfzetxw100% (23)

- Types of AdvertisingDocument22 pagesTypes of Advertisinganjali mohandasNo ratings yet

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- Bus 102 Study GuideDocument35 pagesBus 102 Study Guidewang FarrahNo ratings yet

- NSE - National Stock Exchange of India LTDDocument1 pageNSE - National Stock Exchange of India LTDBharathi RajuNo ratings yet

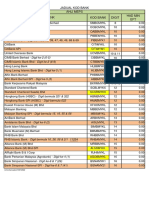

- JADUAL KOD BANK TERKINI (Kemaskini 10012022)Document1 pageJADUAL KOD BANK TERKINI (Kemaskini 10012022)DygKuNormarzuraNo ratings yet

- Answers To Workshop 1: Introducing EconomicsDocument4 pagesAnswers To Workshop 1: Introducing EconomicsAsmaNo ratings yet

- Pharma Outlook 2030: From Evolution To Revolution: A Shift in FocusDocument20 pagesPharma Outlook 2030: From Evolution To Revolution: A Shift in FocusraviNo ratings yet

- GEC 8 The Contemporary WorldDocument68 pagesGEC 8 The Contemporary WorldMay MedranoNo ratings yet

- BUSI1633-Strategy For Managers MODULE-HANDBOOK-2022-23 FinalDocument16 pagesBUSI1633-Strategy For Managers MODULE-HANDBOOK-2022-23 FinalTrần ThaoNo ratings yet

- Third Year T.D.C. Arts International Economics: Paper - IIDocument2 pagesThird Year T.D.C. Arts International Economics: Paper - IIHari RegarNo ratings yet